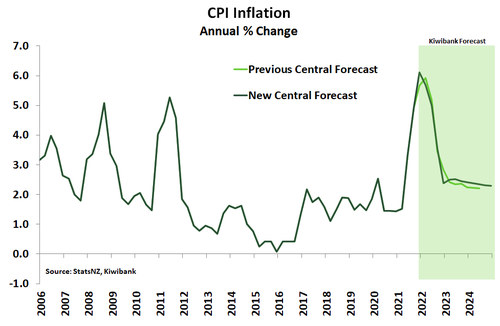

- Kiwi inflation spiked higher in the December quarter, and is up nearly 6% over the year. Inflation is running at the fastest pace in 30 years.

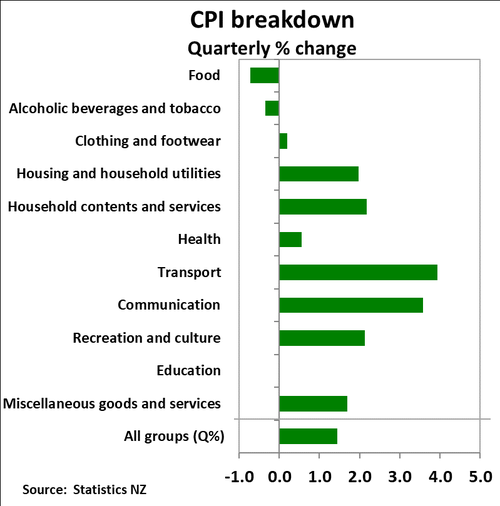

- The details of the report show a broad-based surge in consumer prices, with almost all groups posting decent gains. The growing strength in domestic inflation however is most worrying. Cost pressures will persist and may even be exacerbated by Omicron. The inflation rate is expected to remain elevated.

- Inflation is now knocking on the door of being over twice the top of the RBNZ’s target band. And we don’t think inflation has yet peaked. We expect the RBNZ to keep up the pace, lifting the cash rate at least another seven times to 2.5% by mid-2023. The next hike is due in February.

Today’s CPI report confirmed Inflation hit the highest rate in over 30 years at the end of 2021. An over-stimulated economy faced with supply-chain disruption both at home and abroad is rapidly pushing up the prices of ordinary goods and services. Prices in the CPI surged 1.4% in the December quarter. Annual inflation jumped to 5.9% in the final quarter of 2021 from 4.7%, that’s up from a mere 1.5% at the start of 2021. Inflation may have not been as lively as we had expected, but the details show that underlying inflation is broadening, and we don’t think inflation has yet peaked in the current covid hit surge.

Once again rising housing and transport related prices were the main contributors to the headline index. House construction costs rose 4.6%qoq with strong demand meeting significant supply disruption. Compared to a year ago, new housing is up 15.7%. Alongside housing, transport (+3.9%qoq) was again at the helm of the sharp lift in prices. Petrol prices are up 7% over the quarter and a whopping 30% higher than a year ago. The report also showed that inflation pressure continues to broaden, with prices for 10 out of the 11 groups increasing over the year. Underlying inflation pressure also broadened, with all key core measures of inflation rising in Q4. This suggests that current bout of inflation may not be as transitory as hoped

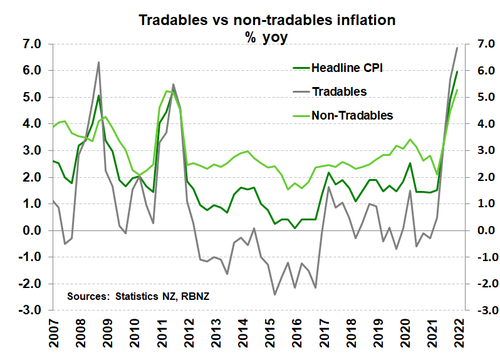

With strong commodity prices over 2021, tradables (imported) inflation rose 6.9%. But the gain in non-tradable (domestically generated inflation) was especially strong. Rising building costs contributed to a very solid 1.5% rise in non-tradables (or domestic) inflation in the quarter. On an annual basis domestic inflation hit 5.3%, which was the highest rate since StatsNZ began to record a domestic/imported split. Non-tradables inflation was comfortably above the RBNZ 5.1% forecast. Importantly, non-tradables inflation represents three fifths of all items in the CPI basket and it’s the chunk that the RBNZ has the most influence over.

We’ve yet to see the peak in inflation given the ongoing supply-side pressures. Global supply chain issues are yet to be resolved and energy prices – especially oil – continue to surge. And we now have omicron to contend with, in the near-term at least. Going by the experience seen overseas omicron will most likely exacerbate cost-push inflation here in NZ. Workers forced to isolate at home will add pressure to an already unbelievably tight labour market.

However, the growing strength of the domestic drivers of inflation is most concerning. Housing-related inflation is soaring and wages are expected to rise. Labour is scarce and Kiwi are justified in asking for higher wages given inflation is quickly sapping households’ purchasing power. Strong domestically generated inflation certainly threatens an extended period of high inflation. To persist, or not to persist: that is the question. And one that will be answered this year. We see inflation remaining stubbornly above 2% through to the end of 2023

Inflation is now knocking on the door of being over twice the top of the RBNZ’s target band. The RBNZ is expected to steady on and return monetary policy to more normal settings. The RBNZ has already hiked the cash rate twice in 2021, to 0.75%. We expect the RBNZ to keep up the pace, lifting the cash rate at least another seven times to 2.5% by mid-2023.

Housing costs heat up

Housing and transport were at the helm of the quarterly lift in prices. But almost all main groups (bar communications) posted price gains over the year as inflation continues to broaden

The 2% rise in housing-related inflation was the largest contributor to December quarter inflation. Demand for housing continues to show unwavering strength. Consents for new builds continue to hit new highs. However, builders are having difficulty in sourcing materials and workers to meet demand. These acute shortages continue to drive up home construction costs, up 4.6%qoq. And on an annual basis, the cost of new housing rose 16%!

The 2% rise in housing-related inflation was the largest contributor to December quarter inflation. Demand for housing continues to show unwavering strength. Consents for new builds continue to hit new highs. However, builders are having difficulty in sourcing materials and workers to meet demand. These acute shortages continue to drive up home construction costs, up 4.6%qoq. And on an annual basis, the cost of new housing rose 16%!

Transport prices were also responsible for a significant chunk of the quarterly rise in overall prices. Energy prices surged late in 2021, with petrol prices caught in the uptrend. Prices at the pump rose 7.7% over quarter, making for some expensive summer road trips. Compared to a year ago, petrol is up a whopping 30%. Beyond the December quarter, global oil prices have continued to charge ahead. Because geopolitical risks are threatening supply. Petrol prices have risen in lockstep and are nearing the $3/litre (regular 91) mark.

The December quarter report also showed the pass through of cost pressures firms are facing onto the retail level. With clogged global supply chains firms are finding it costlier to move goods (if they can get their hands on stock) to stores. But in an environment of strong consumer demand, firms have been able to relieve the cost burden by raising retail prices. The December quarter saw decent price gains for imported goods including recreational equipment and supplies (2.4%), household contents (2.2%) and miscellaneous goods and services (1.7%).

Price movements however weren’t all one-way. Breaking a 3-quarter streak of price gains, food prices posted a modest 0.7% decline due to a seasonal drop in prices for fruits and vegetables (-10%). However, on an annual basis, food prices have soared to 4.1%. The 0.6% December month gain showed renewed momentum in food prices, after back-to-back monthly falls; momentum that is likely to continue into the start of 2022.

Price movements however weren’t all one-way. Breaking a 3-quarter streak of price gains, food prices posted a modest 0.7% decline due to a seasonal drop in prices for fruits and vegetables (-10%). However, on an annual basis, food prices have soared to 4.1%. The 0.6% December month gain showed renewed momentum in food prices, after back-to-back monthly falls; momentum that is likely to continue into the start of 2022.

With strong commodity prices over 2021, tradable (imported) inflation rose 6.9%. But the annual gain in non-tradable (domestically generated inflation) was especially strong. The strength in housing costs led to a chunky 5.3% annual gain in domestic inflation, from 4.5%. The lift reflects strong underlying demand in a Kiwi economy that’s facing significant supply constraints.

To persist or not to persist

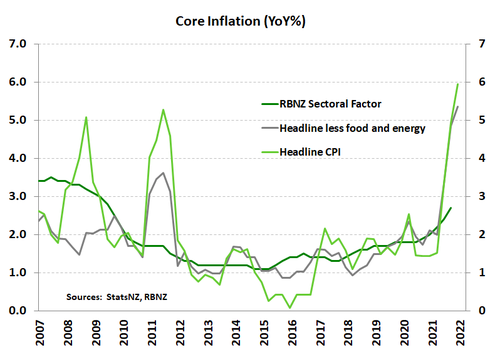

All key core measures of inflation rose in Q4, showing that underlying inflation pressure continues to broaden. Core inflation gives us an idea where inflation may land once volatile price movements settle. Stats NZ’s trimmed means measures followed the extraordinary jump in the headline CPI. Trimming all volatile price movements, core inflation measures ranged between 4.3% and 5.5%. In addition, headline inflation less the volatile food and energy price movements came in at 5.4%, up from 4.8%. Rising core inflation indicates that far from being transitory, the economy’s current bout of fast rising prices may become more sustained.

All key core measures of inflation rose in Q4, showing that underlying inflation pressure continues to broaden. Core inflation gives us an idea where inflation may land once volatile price movements settle. Stats NZ’s trimmed means measures followed the extraordinary jump in the headline CPI. Trimming all volatile price movements, core inflation measures ranged between 4.3% and 5.5%. In addition, headline inflation less the volatile food and energy price movements came in at 5.4%, up from 4.8%. Rising core inflation indicates that far from being transitory, the economy’s current bout of fast rising prices may become more sustained.

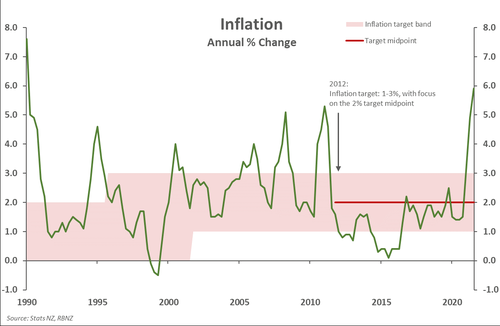

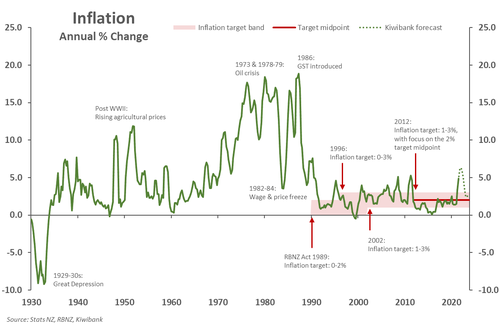

A 30-year high

In the 1970s and 1980s, inflation ran rampant and averaged around 11%. In a bid to stabilise prices, the RBNZ introduced a revolutionary approach to monetary policy known as inflation targeting – later adopted by most central banks. Soon after, inflation was successfully brought under control. But Covid has turned back the clock. Annual inflation shot well above the RBNZ’s 1-3% target band, almost breaching 6%.

In the 1970s and 1980s, inflation ran rampant and averaged around 11%. In a bid to stabilise prices, the RBNZ introduced a revolutionary approach to monetary policy known as inflation targeting – later adopted by most central banks. Soon after, inflation was successfully brought under control. But Covid has turned back the clock. Annual inflation shot well above the RBNZ’s 1-3% target band, almost breaching 6%.

The onslaught of cost pressures brought on by Covid disruptions has seen inflation rise to levels not seen in 30 years. And there’s real risk of prices running higher. Global supply chains issues are yet to be resolved and energy prices – especially oil – continue to surge. But in an environment of strong and resilient demand, firms are sharing the cost burden by increasing consumer prices. Firms’ pricing intentions remain elevated. We’ve yet to see the peak in prices.

Cost-push inflation however should prove temporary. Disruptions to global supply chains will eventually clear; the timing of which is simply uncertain. However, the domestic drivers of inflation continue to strengthen and threaten an extended period of high inflation. Domestically generated inflation has picked up the pace following the relentless rise in housing-related costs. Add to that a super tight labour market. Wage growth is expected to accelerate this year as firms try to attract and retain workers. We see inflation remaining stubbornly above 2% through to the end of 2023. Should persistently high inflation become embedded in price and wage setting behaviour, the RBNZ’s job of taming the beast becomes that much harder. Medium-term (5-year ahead) inflation expectations will be closely watched and have already risen to 2.1% from 2.03%.

Cost-push inflation however should prove temporary. Disruptions to global supply chains will eventually clear; the timing of which is simply uncertain. However, the domestic drivers of inflation continue to strengthen and threaten an extended period of high inflation. Domestically generated inflation has picked up the pace following the relentless rise in housing-related costs. Add to that a super tight labour market. Wage growth is expected to accelerate this year as firms try to attract and retain workers. We see inflation remaining stubbornly above 2% through to the end of 2023. Should persistently high inflation become embedded in price and wage setting behaviour, the RBNZ’s job of taming the beast becomes that much harder. Medium-term (5-year ahead) inflation expectations will be closely watched and have already risen to 2.1% from 2.03%.

With material risk of high inflation becoming entrenched, the RBNZ needs to steady on and return monetary policy to more normal settings. The RBNZ has already hiked the cash rate twice in consecutive moves. We expect the RBNZ to keep up the pace, lifting the cash rate at least another seven times to 2.5% by mid-2023. The unprecedented speed at which the Omicron variant is spreading threatens future economic growth. However, the uncertainty around the economic impact of the Omicron variant justifies the RBNZ’s preferred approach to move in the traditional 25bps increment.