Supply disruption may cause a cost squeeze

- Kiwi business optimism lifted in the final quarter of 2020 according to NZIER’s latest confidence survey. Barring another covid outbreak, NZ’s recovery is likely to continue.

- However, the recovery won’t be evenly experienced. For instance, builders are being run off their feet. However, a net 14% of service sector firms experienced weaker sales in Q4 as our border restrictions are hurting areas such as tourism.

- Local supply-chain disruption at our ports is a growing concern, adding to rising cost pressure and possibly inflation. But disruption is expected to be temporary.

The NZ economy, capsized by covid, righted itself over the second half of last year. Business confidence followed suit as NZ avoided any major outbreak of covid, and spending held up well over the period. According to NZIER’s latest business survey, a net 16% of firms expect worsening economic conditions ahead in Q4 – more than half of the net 38% measured in the previous quarter. Firms’ outlook for own trading activity lifted too with a net 9% of businesses surveyed expecting increased trading ahead. A sharp V-shaped bounce out of lockdown has seen firms’ expectations for profitability jump too. And where business activity and profitability go, intentions to hire and invest tend to follow. The NZ economy has proved much more resilient than expected, with barely a scratch on the hull.

Like last year’s covid hit to the economy, NZ’s recovery is far from shared evenly. NZIER’s December quarter survey suggested that our border restrictions are having an adverse impact on some. The services sector remains the most pessimistic industry with a net 14% experiencing weaker activity over the final quarter of the year. In contrast the building sector, spurred on by a rampant housing market, remains the most optimistic of industries.

But supply-chain issues, related to covid, is having a broader impact on the NZ economy. NZ’s ports are clogged and supply from offshore can be patchy at times. Recent media reports suggest that supply chain issues may get worse in the coming months too, impacting on March quarter growth and future inflation. Pricing intentions did rise, but not to the same extent as cost increases, suggesting a difficulty in passing on rising costs to customers for now.

The survey overall is encouraging for the current recovery. Supply disruptions are a growing concern for the economy, and like us the RBNZ will be closely following these developments. But supply-chain disruption is still expected to be temporary, and any inflation pressure created is likely to be looked through by the RBNZ. Low interest rates are here to stay.

Supply-chain disruption

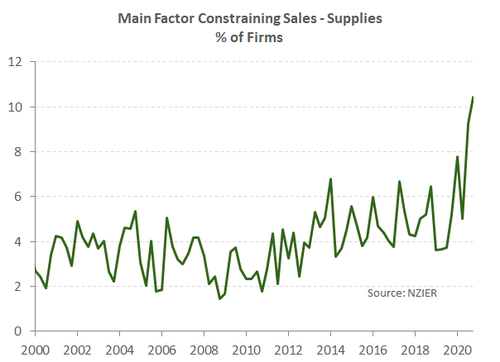

Supply-chain disruption caused by bottlenecks at our major ports was evident in the survey, adding to concerns of rising inflation. An increased share of firms noted access to new stock as enemy number one for turnover. A net 19% of retailers noted supplies as being their largest constraint to turnover in the December quarter, like the net 21% recorded in Q3. Even an increased share of service sector firms noted access to supplies a growing constraint to sales. Unfortunately, clogged ports look likely to be here for a while yet, in part due to the disruption to the usual transit of trade due of covid. China’s upcoming Lunar New Year holiday next month is anticipated to add further disruption with factories in China taking the usual break at this time.

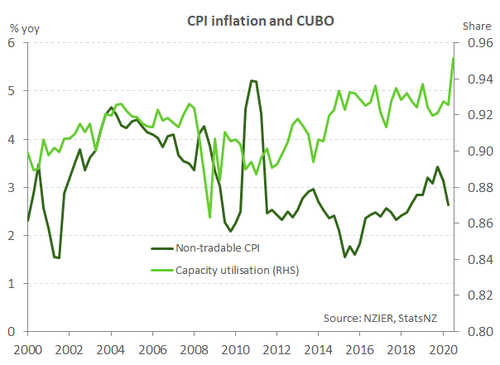

Delays in getting stock may also be contributing to rising costs. Jumps in international freight costs have been widely reported, given a lack of availability of shipping capacity. Pricing intentions did lift in Q4 and firms supplying to the domestic market are under the pump. For instance, capacity utilisation increased to 95%, the highest on record – mostly relating to the building sector. However, capacity utilisation lost its usefulness as an indicator of future inflation long ago (see chart below).

Strong domestic demand shines through

NZ’s stronger-than-expected rebound out of last year’s lockdown has been fuelled by a release of local pent-up demand. Pent-up demand that has been directed internally, while our border is closed, and Kiwi are unable to leave our shores. The building industry has reaped the rewards of more domestic spending and the continuing housing shortage. Consequently, builders are currently the most optimistic bunch. Order books are full, capacity utilisation is at the highest on record at 99.1%, and the pipeline of construction is incredibly full. Consents have hit record levels, and according to NZIER’s survey, architects also have their hands full. Unsurprisingly, hiring remains elevated in construction.

Retailers are also being cushioned by the increase in domestic spending. A net 14% of retailers noted an increase in NZ sales in the fourth quarter. In contrast, a net 5% noted a fall in overall sales. Unlike other industries, retail noted a deterioration in profitability last quarter. Average costs have shot up – supply chain disruptions related – but at the same time there looks to be a reluctance to pass on increased costs to customers.

Retailers are also being cushioned by the increase in domestic spending. A net 14% of retailers noted an increase in NZ sales in the fourth quarter. In contrast, a net 5% noted a fall in overall sales. Unlike other industries, retail noted a deterioration in profitability last quarter. Average costs have shot up – supply chain disruptions related – but at the same time there looks to be a reluctance to pass on increased costs to customers.

At the other end of the spectrum, the service sector is the most pessimistic industry. A result that was anticipated given the lack of foreign visitors for tourist operators. A net 14% of service sector firms experienced falling sales in Q4, only marginally better than the third quarter result. Headcount looks to have been reduced too over the period. Fortunately, the outlook among service firms is a bit rosier. Employment intentions held steady for the March quarter, with a net 12% anticipating an increase in hiring.