Covid-19 to reshape economy

- Covid-19 has left no industry untouched. NZ has been fortunate enough to wind back social distancing measures, allowing for a faster recovery.

- Nevertheless, while borders remain closed, industries reliant on foreign visitors, such as tourism and education, will struggle.

- The current crisis will leave its mark on the economy. Evolving consumer trends, toward online retail, will accelerate. So too, the adoption of productivity enhancing technologies, such as AI and automation.

The Covid-19 crisis in NZ will generate the deepest recession in a generation and will leave no industry untouched. From this upheaval will likely come a change to the economic landscape as trends already in train are accelerated. In the meantime, we can celebrate NZ’s success at squashing the covid curve. We have seen a steady easing of social distancing measures and the resumption of a wide range of economic activity. We have seen early signs that the current recession, while still likely to be the deepest since the early 1990s, won’t be as severe as some worst-case economic scenarios had suggested. Kiwibank’s own electronic card transactions data (see our latest data insights) has shown a surprisingly quick rebound in spending post lockdown – some of which is pent-up demand. Globally, financial markets are more sanguine on improved expectations of future economic conditions. But despite the lift in optimism, the economy is far from out of the woods. The economic outcomes of many Kiwis are likely to get worse, not better, in the near-term at least. Job losses and business closures will continue to mount.

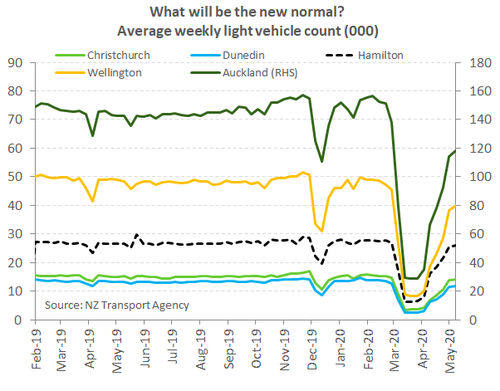

As NZ moves to alert-level 1, most economic activity can resume as normal. The Kiwi economy with run at about 95% capacity in level 1. And the economy will continue to be held below its potential for the foreseeable future. Borders remain shuttered to prevent a second wave of infection, hobbling industries reliant on foreign arrivals such as hospitality, retail and education.

The current Covid-19 crisis will likely leave an indelible mark on the economy. For instance, disruption to some industries has been accelerated by a forced change in consumer behaviour. But aside from the challenges, Covid-19 has also presented opportunities. The lockdown showed that many Kiwis can successfully work from home. A development, if embraced, that could help NZ meet climate change goals. Other industries may grab onto opportunities made available by disruptions to global supply chains. The inevitable reallocation of resources towards more productive firms and processes will have benefits. The faster adoption of productivity enhancing technologies such as AI and automation seem obvious. But the shift of resources may also lead to a concentration of market power, and/or job losses.

Covid’s fallout won’t be shared equally among industries.

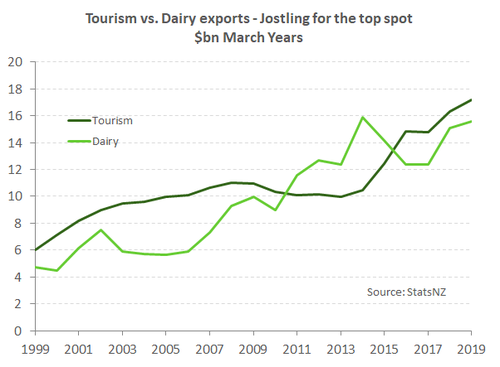

The fortunes across industries will vary markedly, and we know those industries reliant on foreign visitors will be among the worst hit. Tourism-related firms will suffer for many months to come as borders remain closed and the appetite for global travel takes time to recover. Tourism-related industries are broad and include firms in sectors such as retail, hospitality, accommodation, recreation and transport services. Unfortunately, domestic tourism, while doing its best, is unlikely to completely fill the void. International tourism was NZ’s largest foreign-currency earner in 2019, generating $17.1bn or 20% of all exports. Dairy exports came in a close second, generating $15.5bn. The evaporation of international tourism is a huge hole to fill. Domestic tourism was estimated to have contributed almost $24bn. Meanwhile, NZ’s imports of travel services (Kiwi’s spending on overseas holiday’s) was around $6.5bn. So even if Kiwi’s spend all of that travel domestically, taking domestic tourism to ~$30bn, we would still have a +$10bn shortfall.

Nevertheless, a pivot towards the domestic tourism market has already begun. And Kiwis are being encouraged to get out and see their country. We have seen in Kiwibank’s own electronic card transactions data a lift in spending post lockdown (see our latest data insights). Pent-up demand has been unleashed as social distancing restrictions have been wound back. However, local retail faces some challenging times ahead with trends toward online retail accelerating. A glimmer of light for the tourism sector is the plan to allow NZ to share a trans-Tasman bubble with Australia. Australia is easily our largest source of short-term visitor arrivals. Eventually tourism will recover. But a recovery is dependent on borders reopening, and the desire of people to explore the world again.

International education, also reliant on foreign visitor arrivals, has a brighter near-term outlook compared to tourism. Universities have embraced online lectures the best they can. And while servicing the foreign student market also requires the reopening of boarders, education could still operate with restrictive conditions of entry. For instance, if borders are reopened to foreign arrivals – but conditional on 14-day quarantine period – it would likely be easier to convince foreign students studying for a lengthy period to come down under. They could even start studying while in quarantine.

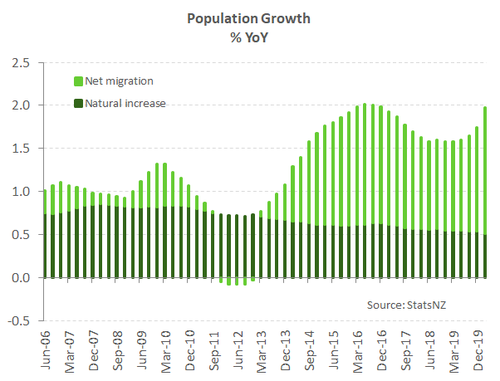

The construction sector’s medium-term outlook is mixed, at best. Residential building is likely to remain supported by the shortage of affordable housing for a while longer. However, net migration – a key driver of housing demand – will fall sharply while boarders remain closed. Yes, we witnessed a spike in Kiwi’s returning home and far fewer Kiwis leaving our shores in March. But once the recent volatility in people moving across the NZ border subsides, NZ’s population growth will fall back on natural means (net births). And the natural population growth of NZ, like most other developed countries, is weak. Fertility rates have fallen for decades. Natural growth contributed only a quarter of NZ’s 2% population growth in the year to March 2020 – a period in which NZ’s population hit 5 million. There is uncertainty whether we will see a rebound in migration flows once border restrictions are relaxed. As a result, the current shortage of housing will likely be met faster than previously expected.

The construction sector’s medium-term outlook is mixed, at best. Residential building is likely to remain supported by the shortage of affordable housing for a while longer. However, net migration – a key driver of housing demand – will fall sharply while boarders remain closed. Yes, we witnessed a spike in Kiwi’s returning home and far fewer Kiwis leaving our shores in March. But once the recent volatility in people moving across the NZ border subsides, NZ’s population growth will fall back on natural means (net births). And the natural population growth of NZ, like most other developed countries, is weak. Fertility rates have fallen for decades. Natural growth contributed only a quarter of NZ’s 2% population growth in the year to March 2020 – a period in which NZ’s population hit 5 million. There is uncertainty whether we will see a rebound in migration flows once border restrictions are relaxed. As a result, the current shortage of housing will likely be met faster than previously expected.

There are real concerns around commercial construction. Even before the covid-19 crisis, commercial construction was facing issues related to cost overruns. And covid-19 has seen the potential of an accelerated trend away from large office spaces. On the plus side, the Government has committed to a large boost in infrastructure spending, which should help offset some of the slack in commercial construction in the years ahead.

Manufacturing has already faced a sharp fall in activity due to both the fall in global demand and the nationwide lockdown. Looking ahead there will be opportunities for manufacturers that can take advantage of global trends, including the use of AI and automation. Such trends are likely to favour larger manufacturers that can marshal the capital need to make such investments, or innovative start-ups.

The ongoing need to feed the planet should continue to provide primary producers with some insulation from the worst of the Covid-19 crisis. A positive to hang onto. However, the hit to global demand from the Covid-19 crisis has already weighed on export commodity prices and farm incomes. Fonterra recently announced its dairy payout forecast for the upcoming season of anywhere between $5.40-$6.90/kgms. If realised, the payout would be a comedown from a $7+ payout for the current 2019/20 season. In addition, high-end luxury producers (seafood, merino wool, wagyu beef etc) may face a larger hit to demand from the global slowdown. Because some customers may be forced to substitute away from luxuries as incomes fall. Unlike many other industries, farming may face significant labour shortages. The usual foreign seasonal workers may be unable to help with peak producing months later this year. Anti-globalisation poses another risk to primary producers and exports, at a time when US-China tensions are rising once again.

Anti-globalisation thrives on economic disorder

The GFC is widely accepted as an accelerant of growing resentment toward globalisation. And the covid-19 crisis has reinforced anti-globalisation sentiment. Global trade will feel the effects of Covid-19 for years to come. Partly justified, with the crisis exposing vulnerability of an overly concentrated global supply-chain. But also, the uglier Trumpian variety of protectionism is growing. At the very minimum producers around the world will look to de-risk supply chains. Some importers for instance will want audits of their suppliers to know how diversified their supply really is. Consequently, there is likely to be a shift in some production from China to other low-wage economies. In addition, some manufacturers will look to repatriate production as an insurance policy. And these developments pose an opportunity for some local niche manufacturers.

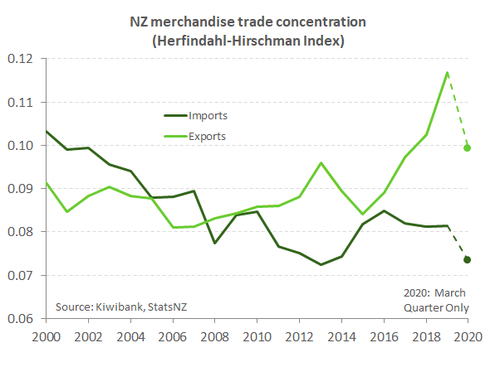

So how exposed is NZ to overly concentrated supply chains? Surprisingly, import concentration by source country – as measured using the Herfindahl-Hirschmann index (HHI) – has reduced over the last 20 years (see chart below). Over time the number of countries we source merchandise imports from has increased and the share spread more evenly as market access has been opened. However, despite increased import diversification NZ wasn’t immune from the global supply-chain disruption seen in the early stages of the Covid-19 crisis. What the HHI isn’t showing is the hidden degree of supply-chain concentration. Modern just-in-time supply chains are layered, complex and fragile. And while we may import electronics or cars from Europe, small but vital components within these goods may only be produced in a few countries outside the region. Most advanced computer chips for instance are manufactured in four countries: the US, South Korea, China and Taiwan.

A switch to domestic production might be costlier and make some goods more expensive compared to imports. Over the longer term though, onshoring would simplify supply chains for some, and provide protection against any future disruption. The coronavirus led to a major breakdown in trade flow, but it’s not the only example of global supply chain disruption. Over the last decade there have been examples of disruption in specific industries. For instance, China in recent years has threatened to limit exports of its exclusive supply of rare earth minerals. And China has threatened tourism flows also. Following the devastating 2011 earthquake and Tsunami in Japan, some automotive components were difficult to source. The growing stoush between the US and China is highlighting the potential for emerging supply chain disruption. The US recently announced a ban on tooling equipment for the production of silicon chips for the Chinese telecommunications giant Huawei. Huawei is a global leader of 5G telecommunications technology hardware. In a US presidential election year, we are likely to see the stakes raised between the US and China in coming months.

An acceleration of trends

Even before the Covid-19 crisis, there were trends well in train around how Kiwis consume, work, and travel. Trends that are expected to now accelerate. Online shopping was already a pastime for many Kiwi’s, from Trade Me to Amazon, and from the Warehouse to AliExpress. The lockdown forced many of us online for bargains. And this is how old habits are broken and new ones formed. We believe we have seen a faster (structural) shift in behaviour toward more online retail activity post Covid-19. Does a new trend spell the death of high-street retail? Probably not. But physical retail outlets may have a smaller footprint. Those that remain will need to trade on a point of difference, such as consumer experience or where it’s convenient for consumers to try before they buy. For retail more broadly there will be a greater need to have a slick online presence. None of this comes as a surprise, but it is happening much faster.

The current crisis has also produced some great opportunities. Take the fight against climate change. Alert levels 3 and 4 provided proof of concept that a decent chunk of NZ’s workforce could work successfully from home. Thereby reducing the need for the daily commute. A shallower peak in transport takes some pressure of clogged transport infrastructure and reduces carbon pollution. Another benefit of working from home includes the increase of effective catchment areas of our largest cities. If commuting to work is no longer a daily ritual, is there a need to live as close to centres of employment? The ability to work from home could alleviate some of the housing shortage in the heart of a sprawling city such as Auckland. And we may see more households moving to the regions.

Current IT infrastructure coped well with the extra pressure placed on it during lockdown. The rate of ultra-fast broadband penetration – at 79% of the population – has enabled working from home to, well, work. If a large share of the workforce continues to work from home, freeing up office space will help boost productivity. And businesses may find more resources to invest in the next opportunity. On the flipside however, the commercial property sector will likely face the challenge of reduced demand.

Current IT infrastructure coped well with the extra pressure placed on it during lockdown. The rate of ultra-fast broadband penetration – at 79% of the population – has enabled working from home to, well, work. If a large share of the workforce continues to work from home, freeing up office space will help boost productivity. And businesses may find more resources to invest in the next opportunity. On the flipside however, the commercial property sector will likely face the challenge of reduced demand.

Another opportunity for the NZ economy is the accelerated adoption of new technologies. New technologies of Artificial Intelligence (AI), automation, and data-driven technologies were increasingly being adopted globally over the last decade. The Covid-19 crisis, like any major economic downturn, will see the destruction of firms and jobs. But from this destruction comes creation as resources are channelled toward the most productive firms and new jobs are formed. A silver lining to the current upheaval would be increased adoption an investment of more of these technologies by NZ firms.

A consolidation of power

The economic upheaval generated by Covid-19 will likely create fertile ground for an increase in merger and acquisition behaviour. Previously viable firms, now struggling, may be picked up by rivals. The merging of business is an outcome that can be beneficial by saving jobs. Larger firms will likely have the wherewithal to acquire smaller competitors and increase market share. A concern though is the risk of too much market concentration and power from merger behaviour. Power which can be abused, working against innovation and offering consumers less choice at a higher price. Nevertheless, the recovery from Covid-19 will also be fertile ground for innovation – aiding the creation of new businesses and jobs. We’ve already seen many examples of customer facing businesses pivoting during Covid-19 to stay alive. The type of entrepreneurial spirit that will allow start-ups to break new ground as we emerge from the current recession.