Key Points

- Headline confidence falls further, with pessimists now outweighing optimists around the outlook for the general economy.

- The fall is at least in part attributed to a change in Government during the quarter, as businesses react to uncertainty around policy.

- In contrast, underlying indicators of activity still managed to hold up relatively well, with a net 18% of firms expecting a rise in activity in the coming quarter - indicating economic growth around trend.

- Investment intentions eased over the quarter and there is concern that the downbeat mood is feeding a lower expected profitability.

- Today’s survey has limited implications for monetary policy, with rising pricing intentions supportive of our view that the RBNZ will begin gradually hiking the OCR from the end of 2018.

Summary

Business confidence took a further hit in the final quarter of 2018 according to NZIER’s Quarterly Survey of Business Opinion (QSBO). A net 11% of firms are now pessimistic about the general economy over the coming six months, down from a net 5% of businesses being optimistic in Q3 and the lowest reading since the September quarter of 2015. The fall in confidence was broad-based across all industries surveyed by NZIER and was put down to a response by businesses to a change in government and policy uncertainty surrounding this change. This development has also been seen in other NZ surveys of business confidence, such as the ANZ Business Outlook survey. In addition, NZ business confidence readings from surveys such as the QSBO do exhibit historical biases toward National-led Governments.

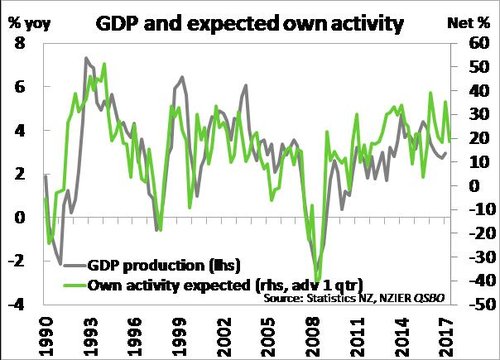

The fall in headline confidence looks to be largely sentiment driven, rather than being a reflection of actual activity experienced. When asked about their own activity over the December quarter a net 10% of firms noted an increase, down 3%pts from September and remains close to the survey average. In terms of future activity a net 18% of respondents are anticipating a rise, which suggests GDP growth will come in at around trend (3% yoy) in the coming quarters rather than being significantly above (see chart below). While we expect economic growth to start picking up from mid-2018, today’s QSBO does highlight a risk to growth if the current business pessimism flows through to actual business decisions. Nevertheless, we expect that confidence will recover through 2018 as actual activity holds up and puts the minds of businesses at ease.

Today’s QSBO is likely to have limited implications for monetary policy on its own. Given the data looks to have been distorted by the recent general election and mirrors other sentiment surveys. Indicators of inflation from the survey, such as pricing intentions and capacity pressures, do support a solid rise in non-tradables inflation over 2018. This is consistent with our view that the RBNZ will begin gradually hiking the OCR from the end of the year.

Some caution revealed in firms’ intentions

While the drop in confidence looks to be driven by perception rather than reality, there were signs among today’s QSBO results that suggest pessimism could be feeding through to firms’ decisions. For instance, measures of investment intentions recorded meaningful drops. A net 2% of businesses intend to invest in buildings in the coming quarter, down 16%pts, and a net 10% (-4%pts) expect to increase investment in plant and machinery. In addition, expected profitability fell sharply at the end of 2017, but is also likely to be attributed to an expected margin squeeze (see below for more detail). While a net 7% of firms experienced a fall in profits, a net 6% expect profits to be lower at the start of 2018. You have to go back to early 2011 for a worse reading. We are not inferring too much at this point as confidence is expected to recover, but there is a risk to economic activity if the current pessimism becomes self-fulfilling. On a more positive note, firms hiring intentions held up well, pulling back to the same level recorded last June.

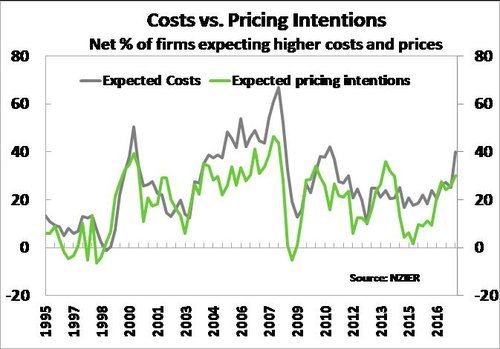

Firms look to hike prices as capacity pressures tighten

Looking behind the headline drop in confidence, firms look increasingly set to hike prices as capacity pressures remain elevated. While a net 18% of firms noted that they increased prices in the final quarter of 2017, a net 31% of businesses intend to lift selling prices at the start of 2018 – the highest reading since mid-2014. It’s easy to see why, with a net 38% of respondents expecting to experience a rise in costs, which is the highest share seen in almost seven years and is indicative of some pressure on margins (see chart below). Part of this rise may be in response to the Government’s decision to lift the minimum wage to $16.50/hr this year and steadily to $20/hr by April 2021. However, a hike in the minimum wage does not come into force until the second quarter of 2018. In addition, rising costs are also likely to be a symptom of elevated capacity constraints. Capacity utilisation lifted to 92.8% in the December quarter, and while builders continue to experience elevated capacity constraints, manufactures noted a jump in capacity utilisation in the quarter. Labour remains a key constraint for businesses, with the difficulty in finding skilled labour particularly acute at the end of last year. A net 49% and 30% of firms are finding it tough to source skilled and non-skilled labour respectively – levels not experienced in NZ since 2005. Labour constraints are expected to feed into rising wage inflation. Difficulty in finding staff may be exacerbated in future by the tightening of migration policy announced by the Government.