- August’s lockdown threw up some surprising results in the housing market. While sales were down 26.5% from last August, house price growth hit a new record of 31.1% across the country.

- However, the data was distorted by lockdown and will remain so while Auckland, our largest market, is in level 4.

- The outlook for housing remains unchanged. Rising mortgage rates, further lending restrictions, affordability constraints, and a boom in new housing supply should all work to cool the market over the year ahead.

A surprising result in August.

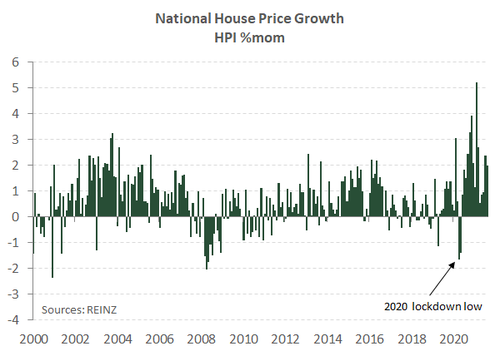

Two weeks of lockdown across the country threw up some surprising housing market results according to the latest REINZ report. Unsurprisingly, house sales in August fell sharply. Sales were 26.5% lower compared to last year and 19.3% down in the month seasonally adjusted. However, house prices, according to the REINZ House Price Index (HPI), still managed to climb a whole 2% in the month. On an annual basis, house price growth hit a new all-time high of 31.1% across Aotearoa. At present house prices appear impervious to anything thrown at them. Withstanding policy tightening so far this year, and now the start of a lockdown, house prices continue to defy gravity.

The rise in house prices contrasts to last year’s lockdown that generated a cautious contraction in prices (see chart below). The contrasting outcome seems to be explained by fewer days in lockdown over August, and the completely different climate in the market this time around. There was still significant interest in the housing market prior to lockdown. Also, the real estate industry and supporting services (conveyance, banking etc.) were better prepared to process transactions already in train during lockdown – socially distanced of course.

Nevertheless, like last year’s lockdown the data is distorted, and will be for a few months. Sales should bounce back in September. But with less vigour with Auckland, our largest housing market, still being in level 4 lockdown. The median number of days to sell in August, a measure of market tightness, was anchored at low levels. However, days to sell should spike in September as sales activity has been held back.

The outlook is unchanged

Looking through the current lockdown distortions, the housing market is still expected to cool. To start with, housing affordability is worsening, denying some would-be buyers from getting on the property ladder. Second, the current construction boom will generate a surge in desperately needed housing supply at a time new demand is curtailed by the closed border.

Finally, it’s undeniable that the RBNZ is currently feeling squeamish on housing. Financial stability risks are growing alongside mortgage-related debt. The RBNZ is responding. LVR lending restrictions for owner-occupiers are set to be tightened from 1 October. And despite the current covid disruption, there is enough in the inflation and labour market outlook to justify hiking the OCR next month. We expect the RBNZ will deliver three hikes by early next year, and lift the OCR to 1.50% in a year’s time. As a result, mortgage rates will be higher next year than they are now. The factors listed above should be plenty to cool the market. House price growth is still expected to reach low single digit rates next year. And there are risks of falling house prices ahead. If house prices do not respond, the RBNZ still has Debt-to-Income lending restrictions up its sleeve.

Regional details

Auckland fared better than any other region in August. Tāmaki Makaurau managed to avoid a double-digit fall in sales during the month (only -9.3%). And annual house price growth of 27.9% was the fastest pace of growth in almost six years. The median house price hit a fresh high of $1.2mn – up 26%yoy. Elsewhere, sales fell much faster, in the range of 15-30%. There were some eyewatering house price gains in places like Canterbury and the Hawke’s Bay.

Contrary to most regions, minor falls in house prices were recorded down south in Otago and Southland. And Taranaki stood out by posting a 2% fall in its HPI in the month. But again, the data will be thrown around for the next month or so.