- Recent mortgage rate hikes are exacting a toll on the housing market. According to the latest REINZ numbers, sales (-39%yoy) hit their lowest reading for a December month since 1995.

- The REINZ House Price Index slipped further, and the median house price across Aotearoa fell below $800k.

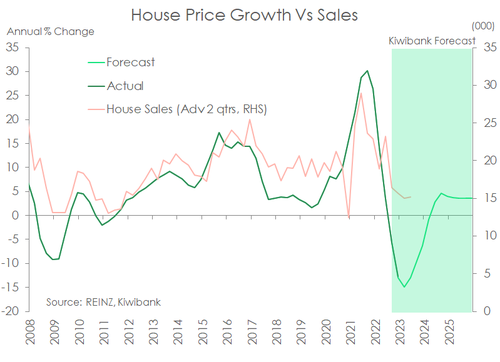

- Declining sales are leading to an increase in the supply of listed property. And properties are taking longer than average to sell. As a result, house prices have further to fall. We are picking annual house price falls to reach 15% in the current quarter. From peak to trough house prices are expected to fall a little over 20%.

Continued correction.

The market continued to go through the motions of a correction in December. TRising mortgage rates are exacting a toll. According to REINZ, unconditional sales hit their lowest level for a December month since 1995. And the 4,336 sales picked up by REINZ at the end of 2022 fell short of the figure recorded back in 2008 by one. Regardless of any future revisions to December sales data, current level of activity is indicative of a weak housing market. House prices posted further losses. The REINZ House Price Index (HPI), down 1.3% seasonally adjusted, recorded the 13th consecutive monthly fall. Over the December quarter as a whole, the HPI was 12.7% down on a year ago in line with our latest forecast (see chart Below). And the median house price across Aotearoa managed to fall back below $800k. However, to put current house price falls in context prices are back to levels seen in early 2021.

Adding to the downward pressure in prices is the growing supply of listed property, despite fewer new listings each month. Total listed property is trending higher according to realesate.co.nz. 26k+ listings were registered with the site in December, up 55% up on year earlier. In contrast, new listings fell further in December to a bit below 7,400 – down from the recent high 10.5k seen in late 2021. Potential vendors are under no pressure to sell at present. The jobs market is strong. And for those that transacted in the market at the peak 12-18 months ago, selling now would likely realise losses. Properties are taking much longer than average to change hands too. The median number of days to sell (seasonally adjusted) stood at 47 days for the third consecutive month compared to the survey average of 39 days.

Given the current backdrop of a slowing economy, and a large chunk of mortgages rolling onto higher fixed rates, house prices have further to fall. We still see house price falls trough in annual terms at -15% in the current quarter. And house prices will continue to fall beyond the current quarter, but just at a slower pace. Our forecast suggests a peak to trough fall in house prices of 21% in the current correction. A recovery in the market appears a long way off, perhaps a 2024 story. However, on the demand side net migration is turning around quickly and will see population growth pick up.

There are clear risks to our outlook for the housing market this year. We believe the RBNZ may deliver too much in the way of rate hikes and monetary tightening. That includes the likely 75bp hike in the cash rate next month to 5%. Although we would advocate a lesser move (25, not 75). And financial markets are moving in favour of reduced rate hikes. The economic pendulum is clearly swinging towards downside risks, rather than upside risks. We continue to forecast a peak in the RBNZ’s cash rate in coming months, and a likely cut to that cash rate by year-end.

A soft landing in some regions

All regions, except for Taranaki experienced price declines in December. Taranaki experienced an almost 2% rise in the HPI, offsetting a similar fall in November. On an annual basis house prices were down only 3.8%, and prices are only 4% below their January 2022 peak. Taranaki is one of a handful of regions (including, Northland and the South Island) that are experiencing a milder market downturn. These regions tended to experience a far less exaggerated boom during covid and have seen a smaller lift in listed property.

In contrast, the larger centres of the North Island are experiencing the largest market correction. Wellington is still the worst hit, with annual house price declines cracking the 20% mark in December.