The focus has shifted to LVRs

- The economy and financial system is in a much better place than we had expected back at the height of NZ’s covid crisis. Loan losses remain very low, but may rise in coming months.

- Both fiscal and monetary policy has proven to be potent, and powerful. With house prices on a tear, LVR restrictions are (effectively) back.

- The FLP will provide banks with cheaper funding, putting further downward pressure on deposit rates, and lending rates. There is still an opportunity in incentivise lending to SMEs.

Summary

“The financial system has been insulated from significant stress so far.” Although significant downside risks still remain, we are in a far better state than we had feared earlier in the year. Both fiscal and monetary policy have been effective in triaging the economy during the covid pandemic. Although the path to a full recovery remains long and arduous. The highly contentious burst in house prices, however, is causing concern, and public backlash. Highly propelled house prices prove the potency of monetary policy. And we’re at a point where both fiscal and monetary policy need to address both speculative demand, and chronic undersupply.

NZ’s financial system faces other risks too. The global economy continues to weather the covid storm. A storm that could wash up here both physically and financially. Cases of covid have risen sharply since October, and social restrictions have been tightened in several major economies across Europe and the US. Back here in NZ, the pandemic has thrown up all sorts of curveballs. Some elements of commercial property are strained such as retail and accommodation, which have faced the brunt of our closed borders. And not going away is climate change and its inevitable financial fallout.

Today’s bi-annual health check of NZ’s financial system was overshadowed by yesterday’s exchange of letters between the Finance Minister Grant Robertson and his pen pal RB Governor Adrian Orr. It appears house prices will be shoehorned into the RBNZ’s remit. The rampant rise in house prices have been fuelled by the various actions of the RBNZ. During a recession house prices typically fall as job losses mount. Cutting interest rates helps lift asset prices, including housing, increasing wealth and inflation – a key channel of monetary policy. But the current recession is atypical. The housing market took off even as NZ was in the depths of the sharpest recession of the last 100 years. There are deep-rooted structural issues at play. One being the ongoing lack of housing supply.

The LVRs are back in effect

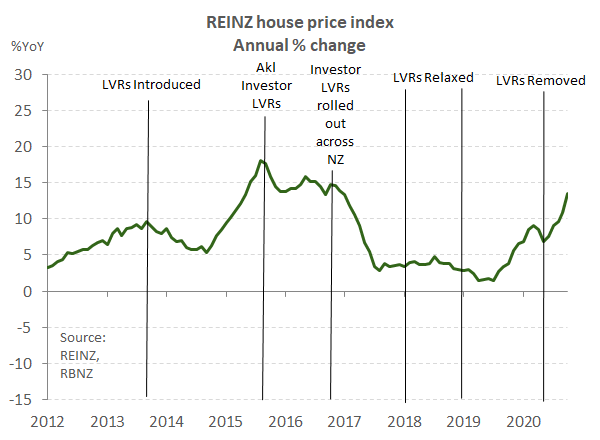

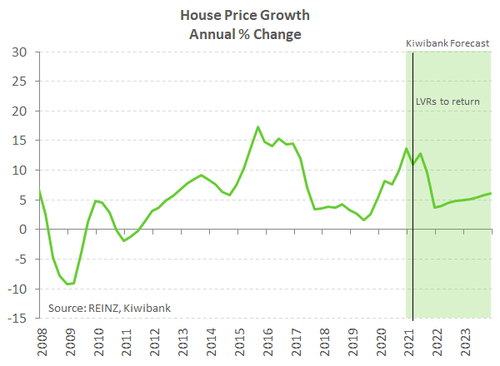

LVR restrictions will be reinstated in March 2021. The housing market has been on a tear in recent months, with record low mortgage rates, and looser lending standards fuelling the fire. Cuts to the cash rate, flanked by threats of a negative cash rate, the temporary removal of high LVR restrictions, large scale asset purchases (QE), and now the FLP, are all aimed at lowering borrowing costs. And our favourite asset to borrow into, is housing. We now find ourselves in a situation where the economy has gone through a sharp recession, but house prices have taken off. Reinstating LVR restrictions on investors should take some of the heat out of the market.

LVRs in the past have been effective in taking the heat out of the housing market. Introduced in 2013, there have been several adjustments made in response to changing financial conditions. In 2016 for instance, LVR restrictions were extended to investor related lending across NZ. Investor related lending shrank quickly and so did house price growth. The reinstatement of LVRs next year is one reason why we are forecasting slowing house price growth over the second half of next year.

If required, the RBNZ could lower LVR speed limits below where they were earlier in the year. Say a 40% deposit requirement for investors. Although for now the RBNZ “…intends to re-impose LVR restrictions at their previous settings from March 2021…”.

More stimulus is on the way

The Kiwi economy has proven incredibly resilient to the shock caused by covid. We’re outperforming the most pessimistic of projections. And it’s thanks to the duo of an ‘elimination strategy’ and significant policy support. But credit is also due to Kiwi businesses. The strength of economic activity following the May lockdown suggests that businesses have adapted to the new operating environment, embracing the shift to online and flexible working. Businesses and households have had to be quick on their feet, and are proving to be more than capable of living with alert levels. Lockdowns are turning out to be far less costly to the economy than we initially feared.

Because of the better than expected resilience of the economy, the near-term risks to financial stability remain well-contained, for now. “Banks have experienced relatively limited loan impairments to date”.

But the risks remain to the downside. The end of Covid is still the big unknown. We’re still one Covid outbreak away from another lockdown. And we’re still living in our pristine bubble. The 95% of the economy not reliant on travel and tourism is roaring. But the 5% are hurting and will continue to do it tough while our border restrictions remain. Policymakers need to keep up the good work.

Still to come, the FLP will further reduce term deposit rates, and lending rates on housing and business loans. Slashing interest rates is designed to disincentivise saving, and incentivise investment. Savers are forced (encouraged) out the risk spectrum, into higher risk assets, like investment property and equities. $1mil dollars in the bank, would have given retirees enough to live on a few years ago. Today, $1mil in the bank would give savers only a few thousand dollars, after tax, with term deposit rates as low as 0.6% ($6,000 per year before tax). Rental yields around the country range from 2.5% to 5-6% in parts. A $1mil rental property could bring in $30-50k before tax. It is no surprise then to see a lift in investors hunting yield.

Where is the money needed? Lending into businesses should be encouraged. As in Australia, the FLP could be incentivised to business lending. The RBA’s term lending facility offers a large sweetener: “For every extra dollar of loans by ADIs to small and medium-sized businesses (those with turnover below $50 million), ADIs have access to an additional five dollars of funding from the Reserve Bank. For every extra dollar lent to large businesses, ADIs have access to an additional dollar of funding.”

Of course, the appetite for loans comes from the business, not the bank. But ensuring the credit is available, at a cheaper rate, helps. As Kiwi SME’s grow in confidence, their investment intentions grow. And banks play a pivotal role in supporting SME expansion.

Interest rates are higher in financial markets

The predictability of the FSR has had little impact on financial markets. Much of the action took place yesterday afternoon. The Finance Minister’s proposal to tweak the RB’s mandate to explicitly include house prices was read by market traders as a potential tightening of monetary policy. Further cuts to the OCR were seemingly pushed to the edge of the table. OIS pricing now effectively sees ~8bps of cuts priced by late 2021. Kiwi rates and currencies rallied hard.

The Kiwi swap curve is higher and steeper. The pivotal 2-year swap rose ~8bps on the day, and the 5-year was up ~10pts. Both have pared back a little. But much of the hard work done by QE to flatten the curve has been unwound. And on currencies, the Kiwi propelled to a high of 69.8c from 69.3C following Robertson's letter. The Governor’s response that the MPC is in fact looking at house prices tamed the Kiwi somewhat, but it wasn’t enough. The Kiwi flyer had fuel left in the tank and continued its charge higher, shooting to 70c! - a level not seen since June 2018. The NZD/AUD cross too neared 95c. It’s hard to believe that the Kiwi was trading at 55USc only a few months ago.