- Inflation in the final quarter of 2020 at 0.5%qoq is much stronger than we had expected, leaving annual inflation unchanged at 1.4%.

- A rapid rebound in domestic demand at the same time supply constraints bite turned the screws on housing, accommodation and used car prices.

- The RBNZ’s dual mandates are far from being met. But the rampant advances in the housing market have surely taken a negative cash rate off the table.

- In order to take some of the heat out of the housing market, unequivocally fuelled by lower interest rates, the RBNZ could look to risk-weights on investors.

The fourth quarter CPI report was much stronger than we, and the market, had expected. The headline print of 0.5% (1.4%yoy) was well above our best guess of flat (0.9%yoy). Domestic accommodation was much stronger than anticipated. Heavy discounting during the winter months was unwound into summer – suggesting solid domestic tourist flows. Home construction costs rose as expected, with the rampant run in the housing market. Used cars were also more expensive, with a lack of supply. The supply constraints at the ports are showing up already in the numbers. But should ease over the year ahead.

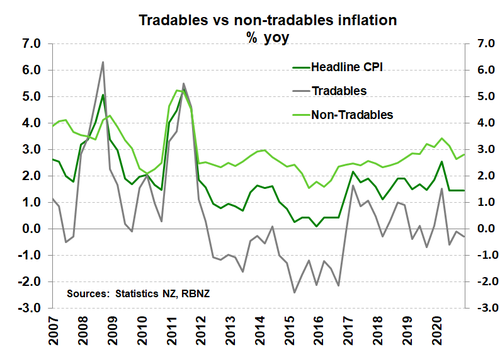

Non-tradables, the domestically generated inflation, was much stronger than expected at 2.8%yoy (up from 2.6%). And tradables, the imported inflation (or deflation), didn’t fall as much as we expected. Tradables inflation was down -0.3%yoy (we thought -0.9%). All measures, no matter how you slice and dice the data, were stronger, and justify a change in RBNZ call.

We’ve witnessed a remarkable journey over 2020. Inflation hit an 8-year high at the start of 2020 at 2.5%, finishing the year at just 1.4% - much higher than we thought.

The biggest “surprise” was accommodation. According to StatsNZ “We saw lower price levels for domestic accommodation in the June and September 2020 quarters, which coincided with a campaign to increase domestic tourism after COVID-19 lockdowns. The December 2020 quarter seasonal price rise, which took prices to near normal levels, therefore resulted in a larger than usual percentage change movement.”

More rate cuts unlikely, more macro-pru likely.

Although both RBNZ mandates are still moving away from them, and unlikely to return to target anytime soon, monetary conditions are easy enough. We have changed our call on the RBNZ. We now expect the OCR to be left unchanged, well into 2022. We had played the man, and we are now playing the ball. We had fiercely opposed negative rates, but thought the RBNZ would steer us down that mistaken path. As it turns out, the economy has proven more resilient, and there is mounting pressure to rein in the housing market. Thoughts of further RBNZ easing have turned to thoughts of RBNZ tightening, via macro-prudential policy.

The RBNZ has already tightened conditions, lifting LVR restrictions from March 1st. Given banks offer pre-approved loans up to 3 months, all major banks have implemented the changes already. The full impact of the LVR changes will be felt in coming months. And if the housing market doesn’t cool, more will come.

Housing, accommodation and cars are more expensive

With our borders closed Kiwi have redirected spending internally. Many of us are holidaying at home, doing up the house and upgrading the car. The added injection of domestic demand was a major driving force in Q4 figures. Moreover, this has occurred at a time when the supply side of the economy is facing constraints, which are also helping to turn the screws on prices. For instance, the supply of used cars over the December quarter was particularly tight. Non-tradables inflation jumped a decent 0.7% in the quarter. On an annual basis domestic inflation actually lifted 0.2%pts to 2.8%, rather than ease further as had been expected.

Housing-related inflation was again a major contributor to headline inflation. Record low mortgage rates, and a fear of missing out over the final months of 2020 fuelled a jump the demand of all things housing. For example, sales activity in the housing market hit multi-year highs. The jump in demand combined with an ongoing shortage of housing led the price of new housing up 1.3%qoq – the largest rise in around two years. Rents also lifted another 0.5% meaning they were almost 3% up on last year.

Housing-related inflation was again a major contributor to headline inflation. Record low mortgage rates, and a fear of missing out over the final months of 2020 fuelled a jump the demand of all things housing. For example, sales activity in the housing market hit multi-year highs. The jump in demand combined with an ongoing shortage of housing led the price of new housing up 1.3%qoq – the largest rise in around two years. Rents also lifted another 0.5% meaning they were almost 3% up on last year.

Local hotel, motel and Airbnb accommodation providers were able to raise rates over summer as we avoided another lockdown and Kiwi happily ventured around our beautiful part of the world. Domestic accommodation prices surged 20% in the quarter from the very low base of a covid hit winter. International travel also featured in the CPI. Travel between NZ and Australia returned in the CPI at a substantially higher price in the December quarter. And even though Stats lowered the weight of overseas travel in the basket it still managed to contribute almost 0.1%pts to headline inflation.

Core inflation is strong

Measures of core, or underlying, inflation pressure added to today’s strong report. Remember core inflation can indicate where inflation might land when large price changes work their way through. StatsNZ’s trimmed means CPI (a measure that removes volatile price changes) landed between 1.7-2.1%, universally above headline CPI of 1.4%. In addition, headline inflation less the usually volatile fuel and energy prices up to 2.1%yoy in Q4 from 1.7% in Q3.

Inflation to strengthen over the medium term

Inflation is expected to cool a little at the start of 2021 before gradually strengthening over the remainder of the year. The Government decided not to hike tobacco excise duties on 1 Jan by the accustomed double-digit rate. And NZ’s success in keeping covid at bay has helped strengthen the NZD. Ongoing disruptions at NZ’s major ports may offset some of the March quarter weakness. However, recently released business confidence surveys such as NZIER’s QSBO, suggest that businesses are wearing higher freight costs for now. Although today’s data indicates that firms might already be passing these costs on. But it’s widely believed that the longer these supply-chain issues continue, the more likely these costs will be passed onto consumers.

Inflation is expected to cool a little at the start of 2021 before gradually strengthening over the remainder of the year. The Government decided not to hike tobacco excise duties on 1 Jan by the accustomed double-digit rate. And NZ’s success in keeping covid at bay has helped strengthen the NZD. Ongoing disruptions at NZ’s major ports may offset some of the March quarter weakness. However, recently released business confidence surveys such as NZIER’s QSBO, suggest that businesses are wearing higher freight costs for now. Although today’s data indicates that firms might already be passing these costs on. But it’s widely believed that the longer these supply-chain issues continue, the more likely these costs will be passed onto consumers.

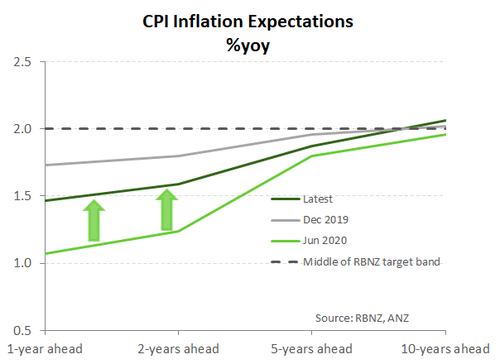

The medium-term outlook for inflation looks stronger compared to just a few months ago. A more resilient economy, with a sustained recovery, suggests there is less spare capacity than believed. In addition, inflation expectations also look to have turned a corner and are strengthening.

Market Reaction

The rates market was shunted higher, and pricing of further rate cuts has been effectively removed. Traders had placed bets on further rate cuts in 2021, following last year’s RBNZ discussion around implementing a negative cash rate. The rampant rise in house prices, and the far better than expected domestic economic data, has seen this risk evaporate.

On currencies, the Kiwi flyer had been riding high off the back of positive offshore – mainly US – developments. The risk-off mood saw the Kiwi (NZD/USD) outperform its peers, trading at 71.97c prior to the CPI release. But seconds after the embargo was lifted, the Kiwi shot up ~23pts to a high of 72.2c. Movement in the NZD/AUD cross also reflected the surprising strength in the report, rising ~25pts to just under the 93c mark. With the risks of deflation, and therefore further rate cuts receding, the Kiwi in effect has been unshackled. If the NZ economy can maintain its A+ recovery performance, then the Kiwi has room to fly higher.

Re-weighting the risk, properly

In our opinion, the next best step the RBNZ could take is a reassessment, and repricing, of the risk associated with home loans. The risk-weighting on home loans could be adjusted, to better reflect the higher risk associated with interest-only and investor loans. It’s been done in Australia. Applying a higher risk-weighting on investor mortgages, forces banks to hold more capital against those loans, and ultimately price them differently. Interest rates on investor mortgages will increase, and (potentially) enable lower interest rates on first home buyer and owner-occupier mortgages. More specific risk weightings will put a spread between lower risk owner-occupier loans, and higher risk investor loans. The same could be done on interest-only versus principal-and-interest (P+I) loans. Interest only is riskier.

So, an owner-occupier upgrading their house with a +30% deposit, on P+I, should receive a lower interest rate than a leveraged investor buying their 5th investment property on interest-only. In Australia, for example, the lowest mortgage rate available is on owner-occupier, principal-and-interest loans. According to RBA data, an owner-occupier interest-only loan is around 75bps higher than P+I (~3.25% versus ~2.5%). Whereas an investor P+I loan is around 30bps higher than an owner-occupier loan (2.85% versus 2.5%). Investors on interest-only pay ~3.1%. And Australian mortgagees can save 10bps off their mortgage rate for stumping up >30% deposit. Re-pricing the risk associated with (all) lending is all in the name of financial stability. And it doesn’t have to be on home loans alone. APRA is easing overall capital requirements, and lowering the risk-weights (and therefore interest costs) on SME lending to help stimulate the economy out of Covid. What a great idea.

Of course, any tweaks to mortgage rates won’t fix the housing problem, not even close. Attacking demand is not the answer. Fuelling supply is the answer. And fuelling supply is more a fiscal responsibility. The Government must step up, in support of the councils, to unlock land, build the infrastructure, and provide long-term plans to tackle our chronic housing shortage. A multi-pronged approach that provides certainty (beyond the election cycle) is needed to channel resources into housing development. We’ve heard the excuses. We know the solutions. We need to put our foot on the shovel al-ready.