- The Kiwi labour market is as tight as it has ever been. Jobs are plentiful, unemployment is at a new record low, and wages are rising. There is no denying the strength of this report.

- New Zealand’s unemployment rate dropped to a record low 3.2%, in line with our forecast. Wage growth picked up to 2.8%.

- Most of the jobs gains came from younger workers, in a sign the labour market is tightening further.

- We expect the RBNZ to lift the cash rate at every meeting this year, reaching 2.5% by November.

Labour market continues to shine.

The labour market looks to have breezed through delta disruptions unscathed. Businesses have maintained a healthy appetite for workers, helped by solid underlying demand and Government financial support over the period. Combined with the closed border and we have a recipe for the HLFS to pump out new record numbers. The unemployment rate dropped once again to 3.2%, a rate never seen in the HLFS’s 35-year history. Employment growth posted a weaker than expected 0.1% in the quarter. But over 2021 as a whole employment growth was 3.7% - just a touch lower than the 4.2% seen in Q3. In addition, the number of filled jobs reported in the Quarterly Employment Survey (QES) posted a second consecutive 1.4% quarterly gain. Plentiful jobs and rising wages should entice more people back to the jobs market. However, a closed border and the potential impact from omicron will limit increases in labour supply in the next few quarters at least. The labour market is set to tighten even further.

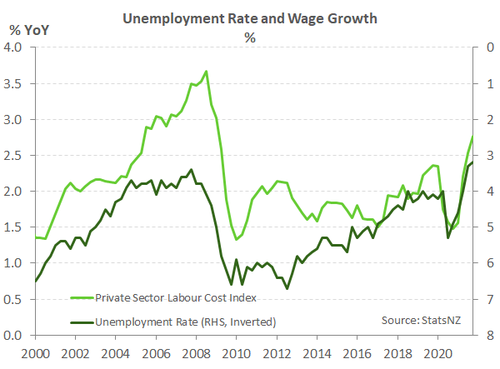

The blatant tightness in the labour market in the current environment drove wage growth higher. Firms are paying up to secure the labour needed. The private sector labour cost index (a measure of pure wage inflation) lifted 0.7% in the quarter reaching a 12-year high of 2.8% over 2021. Similarly, the average ordinary-time hourly earnings recorded rising wage growth, growing 3.8 % last year. With CPI inflation well in advance of wage growth, and a solid labour market expected to persist for some time, wage growth has further to rise, and we see the LCI hitting 3.6% by the end of the year.

As we mentioned in this week’s First View report, we have brought forward our view on the timing of OCR hikes in 2022. In the current environment of worryingly high inflation, and a labour market that has moved beyond full employment there is no time for the RBNZ to take a breather. We now see the RBNZ hiking the cash rate at every meeting in 2022, taking the cash rate to 2.50% by November. A full six months earlier than previously thought.

Wages shrink in real terms

The unbelievably tight labour market and increasing living costs are a recipe for rising wage growth. The private sector Labour Cost Index (LCI) grew 0.8% in the quarter, generating a 12-year high annual increase of 2.8%. However, with CPI inflation running at over twice that rate in 2021, real wages – or wage earners’ purchasing power - shrank. The labour market is a lagging indicator of the economy. Wage growth will continue to rise over much of this year. We see wage growth reaching 3.6% by the end of 2022. In part, as firms entice people back to the labour market, or poach them from competitors with the promise of higher pay rates. In addition, workers will expect compensation for the erosion in their real incomes – or jump ship. And here in lies a major risk for the RBNZ. As wages chase inflation higher, firms are pushed into rising prices further, a nasty wage-price spiral can take hold.

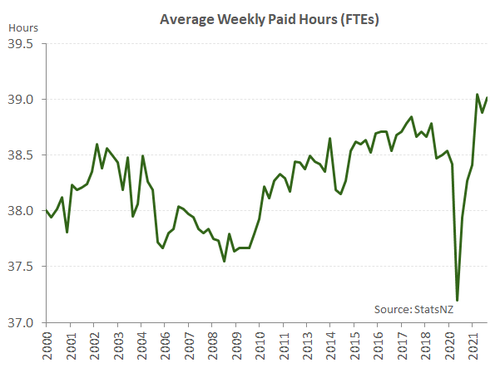

For now, it appears households are mitigating some of the impact of the rapidly rising cost of living by working longer. Firms will be lifting staff hours to counter the acute shortages of labour. In the QES average weekly paid hours for FTEs hit 39 hours. The second highest level recorded after the June 2021 quarter. And well above the pre-covid level of 38.5hrs. The longer working week is another indication of the tightness of the labour market, and one that’s not likely to be sustained.

For now, it appears households are mitigating some of the impact of the rapidly rising cost of living by working longer. Firms will be lifting staff hours to counter the acute shortages of labour. In the QES average weekly paid hours for FTEs hit 39 hours. The second highest level recorded after the June 2021 quarter. And well above the pre-covid level of 38.5hrs. The longer working week is another indication of the tightness of the labour market, and one that’s not likely to be sustained.

Higher and higher

Throughout 2021, each piece of economic data reinforced the same narrative; one of an overstimulated, capacity-constrained Kiwi economy. The Delta lockdown made a far smaller dent to the economy than the 2020 lockdown, with economic growth activity contracting just 3.7%. Inflation has accelerated from 1.5% to 5.9%, with broadening price gains. And the labour market has tightened further, with the unemployment rate falling to new low of 3.2%. Clearly the data continues to overshoot the RBNZ’s employment and inflation targets. In the current environment of worryingly high inflation, and a labour market that has moved beyond full employment there is no time for the RBNZ to take a breather. We now see the RBNZ hiking the cash rate at every meeting in 2022, taking the cash rate to 2.5% by November.

The bigger question is what happens beyond 2022. By year-end, we’re expecting the global supply disruptions to have eased which should see inflation come off its 30-year high, albeit remain elevated. Lifting the border restrictions this year would also help to alleviate some of the cost pressure (PM Jacinda Ardern is scheduled to make an announcement on the border tomorrow). However, more importantly, we expect house price growth to slow significantly in the second half of this year. There’s a lot weighing on the market – rising mortgage rates, property tax changes, tighter LVR rules, tweaks to the CCCFA. And cracks are already starting to emerge. We see the housing market in a state of consolidation (modest house price falls), which should temper domestic demand.

By year-end, the RBNZ could be in a position to pause tightening, keeping the cash rate at 2.5%. Theoretically, a cash rate above neutral (2%) should continue to cool an overheated economy, until bring inflation and employment are back in check. Of course, the RBNZ could raise rates even further if the economy’s temperature refuses to come down, especially on the inflation front.

Naturally, financial markets will toy with the idea of a 50bp rate hike given the strength of the data. There’s definitely further upside risk to employment and inflation, but the risks are not all one-way. Omicron is now the dominant virus in NZ, and its impact on the economy is yet to play out. Restrictions enforced to slow the spread of the virus could dampen business and consumer confidence, which could stymie economic growth. Given the risks and the current state of high uncertainty, we expect the RBNZ to maintain its approach of moving in 25bps increments.