Trifecta: Employment, higher. Inflation, higher. And Growth, higher. The doves must be caged.

Key Points

- Labour market pulls off a scorcher, completing a brilliant trifecta of good economic news. The risk of rate cuts has receded.

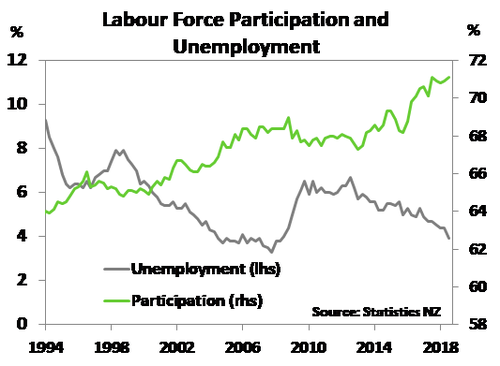

- The unemployment rate plunged 0.5%pts to 3.9%, the lowest rate since June 2008.

- The participation and employment rates hit record levels. People want to work and are finding work. Employment growth (1.1% qoq) exceeded growth in the working age population (0.4% qoq).

- The solid labour market will support spending by households. Consumer confidence has been drifting lower. It’s hard to imagine consumer confidence continuing to wane with such a solid jobs market.

- Wage growth remains modest, but we expect it to accelerate next year.

- The RBNZ have an awkward message to give tomorrow. They have been surprised, pleasantly, on growth, inflation and now employment.

The three-horse trifecta – employment, growth and inflation

Summary

The upside surprises keep rolling in. Today, the labour market report showed a shock drop in the unemployment rate to 3.9%. Unemployment is at the lowest rate since June 2008 – confounding all forecasters. StatsNZ stands firmly behind these figures. There is no way to describe the labour survey other than, it’s on fire! The employment rate at 68.3% is the highest on record, and the labour force participation rate lifted to an equal all-time high of 71.1%. People want to work and they are finding work. The unemployment rate was down, and so too was the underutilisation rate (people wanting to work more hours) at 11.3%. The QE Survey was not as bold as the HLF Survey but did follow the direction. The solid labour market is expected to support consumer spending. Consumer confidence has drifted lower in recent months, as households respond to heightened uncertainty. But today’s report shows a solid foundation. It’s hard to imagine consumer confidence continuing to wane with such a solid jobs market.

Wage growth, as measured by the private sector LCI, came in slightly ahead of our forecast. The LCI increased 0.5% qoq to take annual wage inflation back to 1.9% yoy, down from 2.2% yoy in the June quarter where we had a notable minimum wage hike. Wages will rise over the next year. Inflation is on the rise, so workers have more reason to argue for higher pay. There are chunky minimum wage hikes scheduled over coming years and, as highlighted by today’s figures, the labour market is tight. Tight labour markets generate wage pressure. So there’s plenty for the RBNZ to mull over. And they’ve missed on most of their forecasts.

Plenty to smile about

Looking at the detail, there were some welcome developments.The number of unemployed fell by 13,000, and 11,000 were in the 15-24 age group – an age group that is particularly exposed to fluctuations. Both part-time and full-time employment lifted in the quarter. Part-time experienced a decent 1.6%qoq rise, but this may reflect payback following a 1.4%qoq fall in Q2. Virtually all measures of labour market slack fell in the quarter adding to the trend of labour market tightness. The unemployment rate, underemployment (those wanting to work more but can’t), and the underutilisation rate fell. Filled jobs were up a modest 0.3% qoq leaving the annual increase unchanged at 1.2%. Meanwhile total weekly paid hours were up. This is a great news story, and the Stats department promise it’s not fake news.

Policy implications

Today’s labour market data was decidedly strong. The third in a trifecta of glamour statistics we economists love the most. The purple patch of cool Kiwi data takes the risk of an OCR cut off the table. The screws have tightened a little further on the RBNZ’s decidedly dovish view. A view they are likely to defend for now at least. The RBNZ is meeting its labour market mandate to support “…maximum levels of sustainable employment”. This leaves the Bank focused on inflation. Inflation is coming, and wage growth is ready to play its part. We have further chunky minimum wage hikes ahead over the next few years as the Government looks to reach its goal of raising the minimum wage to $20/hr by April 2021. Moreover, firms are still finding it tough to source suitable staff – a problem unlikely to go away as net migration eases. Competition among firms to attract the staff they need is likely to lift wages.

We expect the RBNZ’s focus on inflation to be fully expressed in tomorrow’s November Monetary Policy Statement (MPS). Local economic data of late indicates some upside to near-term inflation. We would expect the RBNZ to acknowledge these developments, including today’s data, stronger-then-expected Q2 GDP growth, CPI inflation well ahead of the Bank’s August forecasts, and an exchange rate that has weakened. Ultimately though, we don’t believe these developments will be enough to push the RBNZ to alter its OCR outlook track and their message that “The direction of our next OCR move could be up or down”. The RBNZ is keen to see how growth evolves as we move through 2019. Disappointing business confidence figures continue to cast a shadow over the economy, and threatens the sustainable rise in inflation the RBNZ is after. In our view, growth will hold up. We see the next OCR move by the RBNZ being a hike, and one that is delivered around May 2020 – six months or so earlier than the Bank is currently signalling.

Market reaction

The financial markets reacted swiftly. In our weekly commentary titled “Adding a hawkish feather to a dovish headdress” we noted the risk of a more hawkish RBNZ tomorrow, due to the run of solid economic news: “On our view, swap rates should rise and the currency will maintain support. The 2-year swap rate is likely to end the week around 2.10%, bang on our year-end forecast. The currency could take a look at 67c. If the RB turn out to be hawkish, then we could see the 2-year swap rate punch through 2.15% and start looking up at 2.20% - levels not seen since the August MPS. The Kiwi dollar would use 67c as a stepping stone back to 0.6750c. Such a reaction would undo the work of the last MPS. But this is the risk this Thursday.”

Well the reaction has come a day early – thanks to the stellar employment numbers. The 2-year swap rate was catapulted to 2.13% today, up from 2.03% Monday, and 2.06% earlier this morning. There’s a good chance we end the week at 2.18%, and the year at 2.25%. We may see a move towards 2.35% if mortgage related fixing kicks in.

The Kiwi flyer has catapulted through 67c, as expected, and is having a look at 0.6750 (currently 0.6735). The Kiwi flyer is up 70pts on the day, and has bounced of a recent low of 64.50. Our yearend target of 65c may be a little light, but the USD is hard to gauge right now – it should be stronger based on economic fundamentals, but may be weaker based on mid-terms.