- Painful inflation is a global problem. Inflation is proving to be much more persistent and widespread. The war against inflation will continue to heat up. But there has been a positive development – shipping costs are falling. And capacity is increasing with more ships.

- Global shipping costs were one of (the many) catalysts for rapidly rising inflation during the pandemic. The sharp fall in shipping costs, and easing of pressures on supply chains, will be a welcome development for importers and exporters.

- We expect to see a sharp fall in tradables (imported) inflation into next year. But non-tradables (domestic) inflation will prove to be more difficult to contain.

During the early stages of the pandemic, officials threw everything, including the kitchen sink, at the crisis. Trillions of dollars in fiscal stimulus (government spending) fuelled demand. And fiscal stimulus was supported by aggressive monetary stimulus. Central banks eased financial conditions by slashing interest rates aided by copious amounts of QE (money printing). We saw a demand shock. Spending on goods, globally, lurched higher as we spent less on services (esp. travel related). Supply chains were tested, and they failed. Supply couldn’t meet demand.

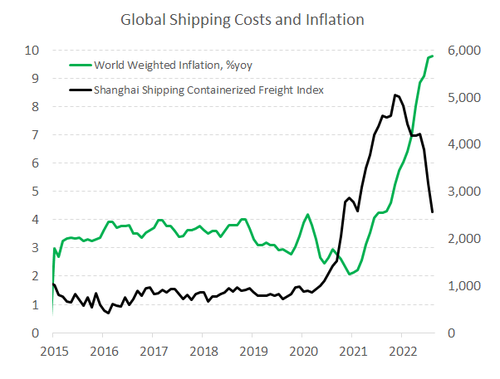

There had been an underinvestment in shipping over the last decade. And the ability to ship goods was severely impacted by Covid lockdowns at the ports. Global supply chains seized up. Shipping costs spiked with the increased pressure, and delivery times blew out. Importers were forced to order, and hold, more stock throughout their supply chains as they tried to keep up with demand. We went from a “just in time” inventory management, to “just in case”. Our first chart shows the rapid rise in shipping costs, and the subsequent spike in inflation.

There had been an underinvestment in shipping over the last decade. And the ability to ship goods was severely impacted by Covid lockdowns at the ports. Global supply chains seized up. Shipping costs spiked with the increased pressure, and delivery times blew out. Importers were forced to order, and hold, more stock throughout their supply chains as they tried to keep up with demand. We went from a “just in time” inventory management, to “just in case”. Our first chart shows the rapid rise in shipping costs, and the subsequent spike in inflation.

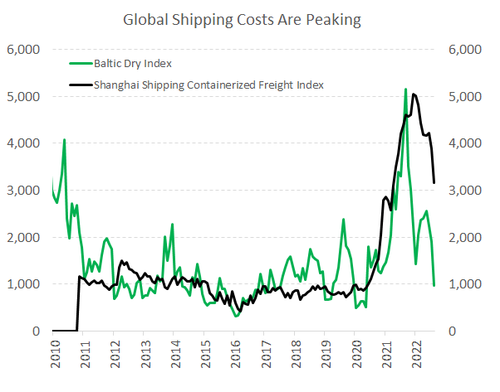

Our second chart shows the swift decline in the Baltic Dry Index and the Shanghai Shipping Containerized Freight Index. Both indexes have fallen sharply. Our third chart confirms the reduction in pressure on supply chains. In part because future shipping capacity will expand. Capacity is likely to grow with a steady increase in new ships being built. We have heard numerous anecdotes from our importer and exporter clients about the reduction in cost and time. This is a big step in the right direction.

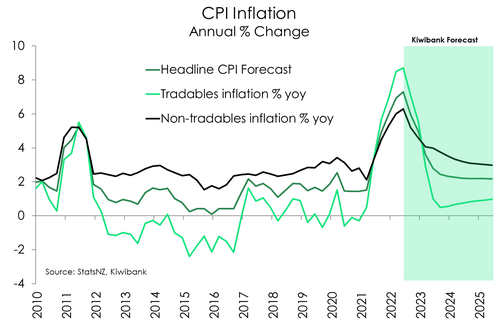

We are by no means back to ‘normal’. And we must reiterate that the war on inflation will continue well into next year. We just wanted to highlight the good news amongst the bad. Our fourth and final chart illustrates our inflation forecast into 2024.

Tradables inflation hit 8.7% in the latest (June quarter) CPI print. We expect this to be the peak. Supporting the move lower, there is likely to be an easing in commodity prices into next year as demand wanes. The main driving force in our forecast decline in inflation is in the tradables components.

Domestically generated inflation, however, is of greater concern. The gain in non-tradable inflation has been especially strong. On an annual basis, domestic inflation hit 6.3%. Housing related costs were the main driver, with construction of new dwellings up a whopping 18% over the year. Wages are also on the rise. Domestically generated inflation is likely to be much stickier, and harder to contain.

Overall, the current headline inflation rate of 7.3% may prove to be the peak, but we expect inflation to remain stubbornly above 3% well into 2023. The RBNZ has their work cut out for them. For more on our inflation outlook, see “Prices just keep on rising. Inflation has hit 7.3%. We hope it’s the peak”.

Central banks are in the process of mopping up extraordinary stimulus and reducing demand. We have seen central banks deliver outsized rate hikes in quick succession. This will continue. For more on our outlook for interest rates, and exchange rates, please see “Human behaviour: interest rates invert as inflation peaks and growth slows”.