- Finally, we have received some good news on inflation. Inflation looks to have peaked, globally. We are simply importing less inflation. This is great news. The world war on inflation is turning.

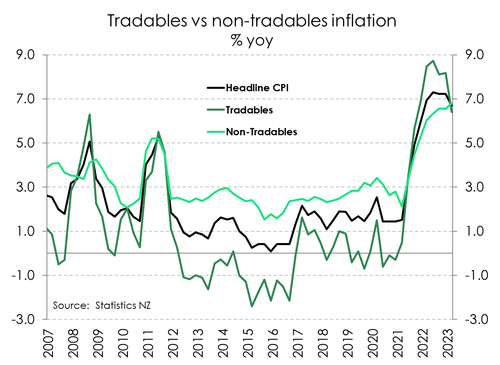

- Imported inflation eased from 8.2% to 6.4%. That was the pleasant surprise. Petrol prices are down 8.3% over the year. And the outlook for global prices has continued to improve.

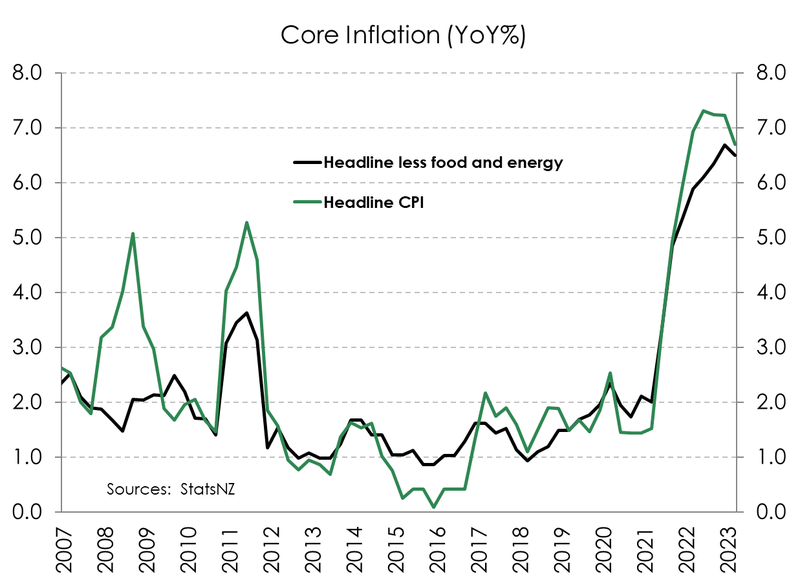

- Domestically generated inflation, esp. construction related prices, remains sticky, and lifted from 6.6% to 6.8%. Core measures of inflation, which strip out volatile stuff, came in lower.

- We’re confident we’ve seen the peak in inflation, with the annual rate comfortably below 7% at 6.7%. We still expect the RBNZ to deliver a 25bp hike to 5.5% in May. And that should be it. Done. Interest rates have also peaked.

We need to take this report for what it is – good news. The annual rate of inflation has dropped below the psychological 7% run rate, to 6.7%. It’s a convincing move lower. And we expect further falls from here. We continue to forecast an easing in the inflation rate towards 3.3% by year-end. So prices are still rising, but at a much more reasonable rate. If we’re right, inflation will be back within the RBNZ’s 1-to-3%yoy target band early in 2024. Job done... And interest rates have peaked.

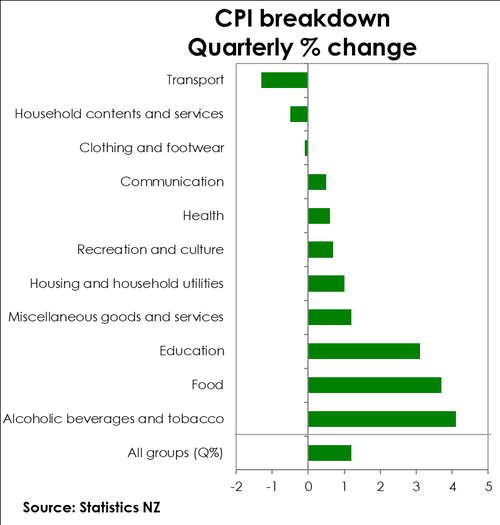

When we slice and dice the data, we see some markedly mixed moves in prices. But the key takeaway was the reduction in the breadth of price rises. Within the basket of goods measured, only 63% recorded gains, down from 72% last quarter. And the origin of the price rises is shifting. Half of our inflation has come from offshore. And it’s that half that’s providing the relief. Tradables (imported) inflation has dropped sharply from 8.2% to 6.4% - and we forecast a fall to 1% by year end. There’s a good chance of some imported deflation into 2024. Petrol prices have dropped 8.3% over the last year, and we expect to see further falls in oil prices into 2024, as global demand wanes. Central banks have lifted interest rates at a rapid rate to rein in inflation. And it’s working.

It's not all good news, however. There are still some hot spots. Food price inflation is being felt, with a whopping 3.7% gain in the quarter alone. Devastated crops in the Hawke’s Bay will take years to recover. Construction related costs are still too high, although they have moderated a touch. And the rebuild from the flooding and cyclone will prove to be inflationary. When we look at local prices, non-tradables, we see an awkward lift from 6.6% to 6.8%. Although the all-important core measures have eased from ~6.4-to-6.6% to 5.9%-to-6.1%.

We have broken the back of the inflation beast. And we should see the last RBNZ rate hike in May. Although it is not needed, the RBNZ is likely to hike the cash rate by 25bps (a downsized move from the 50bp last time) to 5.5% - as telegraphed in the RB’s February Monetary Policy Statement. We stick to our call that the move beyond 5% is going to be a step too far. And we expect to see a material contraction in economic activity.

The RBNZ is doing whatever it takes to tame inflation. And the good news in today’s report is that inflation is running well below the RBNZ’s forecast (7.3%).

We expect the next move, after May’s decision, will be a rate cut. And we’ve pencilled in a move by the RBNZ in November. By November, we are likely to in the middle of a mild recession. A recession engineered by the RBNZ, in order to tame inflation.

Basket breakdown: some up, some down.

Food and housing-related inflation were the main drivers of the lift in consumer prices, once again. But in an interesting development, prices pressures were less broad-based. Over the quarter, a little over 60% of all items in the CPI basket posted a lift in prices. That’s compared to the series-high of 72% share recorded in the final quarter of 2022.

Food and housing-related inflation were the main drivers of the lift in consumer prices, once again. But in an interesting development, prices pressures were less broad-based. Over the quarter, a little over 60% of all items in the CPI basket posted a lift in prices. That’s compared to the series-high of 72% share recorded in the final quarter of 2022.

Food was at the helm of the quarterly lift in consumer prices, adding 0.7%pts to the headline rate. Over the quarter, food prices rose 3.7% with material lift in the price for fruit & veg as well as grocery foods. Given the severe weather events earlier this year, it’s no surprise to see material lifts in the price of fruit and veg (9.5%qoq) and grocery foods (4.4%qoq). Compared to a year ago, food prices overall continue to accelerate, up 11.3% from 10.7%. The usual excise duty on tobacco, at this time of year helped to push prices up 4.1% for the Alcoholic beverages and tobacco group.

Housing was another strong driver of quarterly inflation, contributing 0.3%pts. But price pressures continue to ease. The largest and most persistent driver of non-tradables inflation, housing-related inflation, eased further in the March quarter. The home ownership price index, which includes house construction, rose 1.1% in the quarter as wage rises and some rises in the price of materials came through. And annually, home construction costs fell to 11.1%. Though still elevated, it’s a material slowdown from the 18% peak recorded late in 2021. There’s no denying the serious capacity constraints that the construction sector continues to face. However, the supply disruptions that have dogged the sector are easing with shipping costs falling. And rising mortgage rates and the ongoing correction in the housing market will further weigh on the building sector.

The price impact of the recovery in tourism continues to feed through. Compared to a year ago, prices for recreation and culture services are up 3.4%. Domestic accommodation services, in particularly, has lifted close to 30%yoy.

Price movement over the March quarter, however, wasn’t all one way. Clothing and footwear prices fell 0.1% , and the 5.1% drop in prices for furniture and furnishings brought the household contents group down 0.1%. We’d expect this discounting to continue over the coming months. For one, consumer confidence is subdued and the appetite to spend is waning in the current environment. With less demand, there’s less ability for businesses to lift their prices.

Petrol prices also fell further over the March quarter, down 2.6%, which was the single largest contributor to the 1.3% overall drop in transport prices. Compared to this time last year, petrol prices are down 8.3%. International airfares also dropped over the quarter, down 4.3%. Although this may be a bit of payback following back-to-back quarters of double-digit lifts in prices. Faced with a perfect storm of stretched air transport capacity and strong demand for travel, airfares lifted sharply. But we expect prices to normalise in the coming months. The transport group overall is likely to experience sizable volatility over the coming quarters. Government policy such as previous cuts to petrol excise tax and half-price public transport will be reversed in the coming quarter.

Core inflation continues to cool.

With the Cyclone distorting the short-term view, the more important measure to follow is core inflation. The underlying trend in inflation remains uncomfortably strong but appears to be easing. Key measures were suggestive that inflation is past its peak – a development that has been repeated in other developed countries. For instance, the trimmed-mean measures of inflation (exclude volatile price movements), eased further in the March quarter. On an annual basis, trimmed-mean measures fell to between 5.9% and 6.1%, down from 6% and 6.6%. Headline inflation less food, household energy and fuel posted a 0.9% gain, much softer than last quarter’s sizable 2% gain. Annual core inflation cooled to 6.5%, from the apparent 6.7% peak.

Domestic inflation accelerates.

Just as we’ve seen unfold overseas, we expect inflation to continue on a downtrend this year. In fact, even with the weather events at the beginning of the year, we have seen a convincing slowdown in inflation. The disinflationary momentum is building. Imported or tradables inflation is likely to fall this year. We’ve seen global commodity prices ease and shipping costs have clearly turned south. And it's starting to show in the numbers. Over the quarter, tradables inflation lifted 0.7% - that’s the weakest quarterly rise since the end of 2020. On an annual basis, tradables inflation looks to have peaked at 8.7% in the middle of 2022. Today’s report showed a steep fall to 6.4%. That’s good news. Half of the inflation that we are experiencing right now, came from offshore.

Just as we’ve seen unfold overseas, we expect inflation to continue on a downtrend this year. In fact, even with the weather events at the beginning of the year, we have seen a convincing slowdown in inflation. The disinflationary momentum is building. Imported or tradables inflation is likely to fall this year. We’ve seen global commodity prices ease and shipping costs have clearly turned south. And it's starting to show in the numbers. Over the quarter, tradables inflation lifted 0.7% - that’s the weakest quarterly rise since the end of 2020. On an annual basis, tradables inflation looks to have peaked at 8.7% in the middle of 2022. Today’s report showed a steep fall to 6.4%. That’s good news. Half of the inflation that we are experiencing right now, came from offshore.

The focus is now shifting away from imported inflation and toward domestically generated inflation, which remains heated. Today’s report showed non-tradables accelerated over the quarter by 1.7%, and the annual rate has lifted to 6.8%. – a new record high since Stats NZ began reporting the domestic/imported split. The Cyclone and the following rebuild frustrates the outlook for domestic inflation which will frustrate the RBNZ. Hot and sticky domestic inflation means it’s a slow journey back to target.

One more rate hike to go.

The RBNZ’s latest policy announcement once again demonstrated their resolve in bringing down inflation. The RBNZ is sticking to its pre-set path. And that path has one more hike to 5.5%. We must expect a 25bp move in May – despite today’s print coming in well below the RBNZ’s forecast of 7.3%.

However, we believe the RBNZ is nearing the end of its current tightening cycle. There’s growing evidence that their actions to date are dampening demand. Business and consumer confidence remain downbeat. Businesses aren’t willing to invest, and household budgets are feeling the pressure. After 500bp (and likely another 25bp) of tightening, it’s time for the RBNZ to pause and assess the impact. Monetary policy operates with a lag. And we’re yet to see the full impact of past actions on today’s economy.