- House prices took another hit in August. The REINZ House Price Index was 5.9% down on last year. The median house price across Aotearoa fell by a similar rate to $800,000.

- House sales, a lead indicator of prices, did show improvement in August. Sales were 18% lower than last year, an improvement on July’s 35% drop. However, last year’s delta lockdown is distorting annual comparisons.

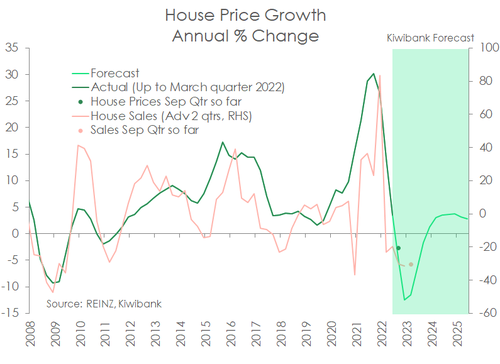

- House prices have further to fall in the near term. As mentioned in our latest housing supply and demand note, we are forecasting house prices to be 13% lower by year end before a modest recovery.

Largely one-way traffic.

The run of play in the housing market continues to be largely in one direction, according to the latest data from REINZ. The REINZ House Price Index (HPI), fell another 1.4% in August to be 5.9% down on the same months last year. The median house price across Aotearoa of $800,000 was down by the same rate as the HPI in August. The rapid rise in mortgage rates this year continue to weigh on the market as debt servicing becomes increasingly expensive.

It’s hard to find good news from within the latest housing market data. But we did try. For instance, there were early signs that the trough in house prices might be on the horizon. The 4,891 sales recorded by REINZ in August were almost 8% up compared to July (seasonally adjusted). And compared to last August, sales were18% lower. Up from the 35%yoy drop recorded in July. Importantly, annual comparisons of sales from August to September will be distorted by last year delta lockdowns – mostly centred on Auckland. Nevertheless, sales are a forward indicator of house price movements, loosely leading house price growth by around six months (see chart above). As recently mentioned in our latest housing supply and demand note, we are forecasting house prices to be 13% lower by year end. A dramatic fall for sure. But a 13% trough would only take the HPI back to levels seen at the start of 2021. From early next year we see a gradual recovery in prices. Gradual because significant new housing supply is far outstripping new housing demand.

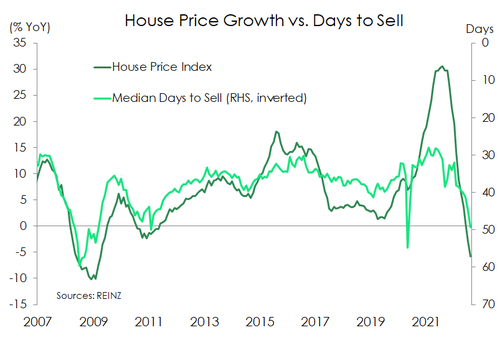

Delta distortions aside, buyers seem to have the upper hand. The level of listed supply remains high by recent standards. And elevated supply is likely to dent any market gusto during the coming spring season. In addition, the median number of days to sell (DTS) a property rose further in August to 49 days. That is the highest DTS since May 2020 –resulting from the first nationwide covid lockdown – and a full 10 days above the long-run average. We will want to see a fall in days to sell before we are confident that house price growth is turning around (see chart above).

Delta distortions aside, buyers seem to have the upper hand. The level of listed supply remains high by recent standards. And elevated supply is likely to dent any market gusto during the coming spring season. In addition, the median number of days to sell (DTS) a property rose further in August to 49 days. That is the highest DTS since May 2020 –resulting from the first nationwide covid lockdown – and a full 10 days above the long-run average. We will want to see a fall in days to sell before we are confident that house price growth is turning around (see chart above).