Underlying weakness

June 2017 quarter Labour Market Review

Key Points

• The fall in the unemployment rate to 4.8%, masks underlying softness in the labour market.

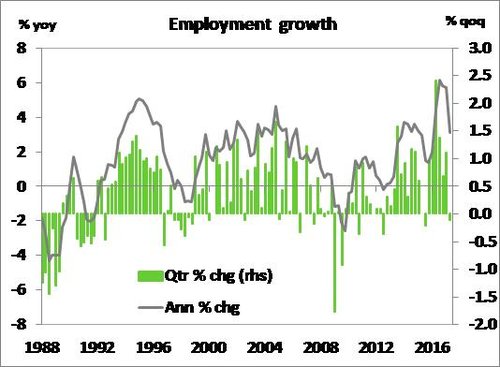

• Instead of posting a respectable rise as expected, employment fell 0.2%qoq in the June quarter.

• The unemployment rate was saved by a notable -0.6% point drop in the labour force participation rate to 70% - still historically high.

• Wage growth looks to be stuck in neutral, recording a muted 1.7% yoy overall.

• For the RBNZ, today’s data is likely to further convince the Bank that the OCR should stay unchanged for an extended period. We maintain our view that the OCR will remain on hold until late 2018, but acknowledge that downside risks to our view have risen.

Summary

On the surface, today’s June quarter labour market data from Statistics NZ looks respectable with the unemployment rate falling 0.1% point to 4.8% - the lowest unemployment rate since December 2008. However, scratch the surface and the suite of labour market data (including the Household Labour Force Survey (HLFS), Quarterly Employment Survey, and the Labour Cost Index (LCI)) seems less encouraging. Instead of recording a reasonable rise in employment, as we and the market had expected, total employment actually fell 0.2% qoq or 4,000 people in the second quarter. Saving the unemployment rate from experiencing a rise was a notable 0.6% point drop in the participation rate to 70% – still an elevated level by the HLFS’s standards – as there was a jump in the number of those not in the labour force.

Labour market data is notoriously volatile and underlying today’s figures was a partial reversal in the surprise jump in self-employed workers in the March quarter. While employment growth looks more modest, the labour market is expected to continue to tighten – albeit gradually. The economy is still growing soundly, and surveys of business sentiment continuing to shown that firms have an appetite to increase headcount.

Despite a general soft tone to today’s labour market report, there were a few signs of ongoing labour market tightness. In addition to a lower unemployment rate the HLFS’s underutilisation rate fell 0.5% points to 11.8% - also the lowest rate since late 2008. Nevertheless wage growth remains stuck in neutral, with the private sector Labour Cost Index (LCI) posting the eighth consecutive 0.4% qoq increase and a 1.6% yoy gain.

Today’s data adds to generally weaker-than-expected domestic data of late and backs up the RBNZ’s desire to keep the OCR unchanged for an extended period. We maintain our view that the OCR will stay put at 1.75% through to the end of 2018. However, we acknowledge that downside risks to our view have increased in light of generally softer data.

Unemployment rate belies a softer labour market

As we and the market had expected the unemployment rate fell 0.1% points to 4.8% in the June quarter, but underlying the fall was a generally soft labour market report. In contrast to a widely expected increase, employment actually fell 0.2% qoq or 4,000 people in the second quarter of 2017 to be 3.1% higher yoy. The saving grace for the unemployment rate was a sharp 0.6% point drop in the labour force participation rate to 70% - although it’s worth noting that the participation rate remains at an historically elevated level. The rise in the labour force participation rate was driven by more people leaving the labour market in the second quarter. This result is at odds with the ongoing record levels of net migration, with a large share of migrant arrivals in NZ to work.

Following the release of March quarter labour market data, we had noted that the strong jump in employment may have been artificially elevated by a surge in the number of those self-employed in Q1. In the June quarter there was a partial 15,000 reversal of the number of these reporting to be self-employed, following the 25,000 jump in the March quarter. To get a better sense of underlying employment growth over the first half of 2017, the QES (which does not survey self-employed without employees) showed total filled jobs were 3.1% yoy higher in Q2, up from a more modest 2.4% yoy rise.

Despite the fall in employment and the labour force participation rate, there were some signs of ongoing labour market tightening. In addition to the lower unemployment rate, the underutilisation rate fell 0.5% points to 11.8% - also the lowest rate since late 2018. Part of the reason for this may come in a shift of people form part-time to full-time roles. The number of full-time employees rose 0.7% qoq at the same time as the number of part-time employees dropped 1.8% qoq. In addition, the QES revealed a notable 0.9% qoq lift in total weakly paid hours, which were 3.5% higher than a year ago. And while wage inflation was soft (see below), the unadjusted LCI recorded a 3.1% yoy rise.

Wage growth stuck in neutral

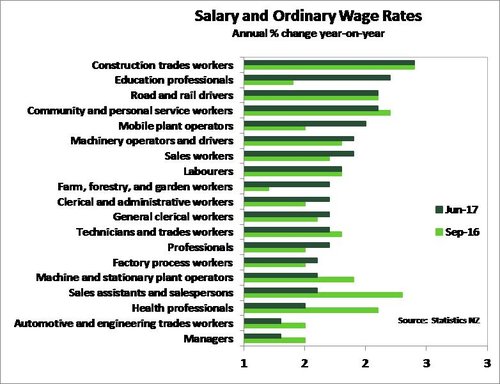

Wage growth was once again muted, with the headline LCI recording a 0.4% qoq increase to take annual wage inflation to 1.7% yoy – on par with June quarter CPI inflation. The private sector LCI (the RBNZ’s preferred measure of wage inflation) resembles a broken record, increasing 0.4% qoq in the June quarter the same rate of growth for two years straight. Annual private sector LCI wage growth managed to edged up 0.1% points to 1.6% yoy. By occupation, wage rates were broadly muted with the exception of education professionals (related to the annual process of the Ministry of Education’s renegotiated collective employment agreement) and sales assistants, which both recorded 0.7% qoq gains. On an annual basis, trades related to the construction sector stood out in terms of wage and salary increases, which recorded a 2.4% yoy increase (see figure below).

The ongoing softness in wage growth in the face of labour market tightening is not unique to NZ, with a number of other developed economies experiencing similar trends. The lack of wage pressure suggests that there is more spare capacity in the labour market than previously thought. In NZ, record levels of net migration adding to labour supply has been a prominent driver of growing spare capacity. However, spare capacity in the labour market is in contrasts to business sentiment surveys that have revealed a growing share of firms are experiencing increased difficulty in finding suitable staff. In NZIER’s latest Quarterly Survey of Business Opinions a net 47% of firms reported difficulty finding skilled staff. We still expect to see wage growth begin to pick-up in the coming quarters given these noted skill shortages, and recent increases in inflation give employees a stronger case for wage rises.

The ongoing softness in wage growth in the face of labour market tightening is not unique to NZ, with a number of other developed economies experiencing similar trends. The lack of wage pressure suggests that there is more spare capacity in the labour market than previously thought. In NZ, record levels of net migration adding to labour supply has been a prominent driver of growing spare capacity. However, spare capacity in the labour market is in contrasts to business sentiment surveys that have revealed a growing share of firms are experiencing increased difficulty in finding suitable staff. In NZIER’s latest Quarterly Survey of Business Opinions a net 47% of firms reported difficulty finding skilled staff. We still expect to see wage growth begin to pick-up in the coming quarters given these noted skill shortages, and recent increases in inflation give employees a stronger case for wage rises.

Policy implications

For the RBNZ today’s June quarter labour market data adds to other data that points to weaker inflation over the coming quarters. Data such as: weaker core inflation, weaker GDP growth and ongoing strength in the currency. In the RBNZ’s mind recent developments are likely to reinforce the Bank’s view that the OCR will remain unchanged for an extended period. We still maintain that the RBNZ will keep the OCR unchanged at 1.75% until the end of 2018, but acknowledge that downside risks to our view have risen.

Market reaction

There was a sharp market response to this morning's labour market data. The NZ dollar, which was already drifting lower following events overnight, fell half a cent against the USD to around $0.7420 post release where it has remained since. Wholesale interest rates also fell following this morning’s report, with the 2-year swap rate hitting a low of 2.19%. More importantly, the softer labour market report led to market pricing for a RBNZ rate hike to move out to September 2018 – one month later than previously envisaged.