Core measures of inflation are moving in the right direction, and at a quickened pace.

Key Points

- Inflation is heading in the right direction. Pressures are building.

- The slight upside surprise in the inflation data occurred underneath the surface.

- There was no evidence to suggest an urgent need to adjust monetary policy. The doves will have to wait.

Summary

What goes up, must come down (unless it enters space). The 5.5%qoq spike in petrol in the Sept quarter, was only partially reversed with a 0.6% fall in the Dec quarter. Food prices also fell, as they always do. The headline print of inflation rose a mediocre 0.1%, holding the annual rate at 1.9%. The numbers were a positive surprise, for a change. Kiwibank and market consensus saw 0.0%qoq and 1.8%yoy.

As economists, we don’t like volatility in numbers. So, we rip out the volatile stuff to get a handle on how pressures are building – it’s “core” to what we do. When we rip out the erratic stuff we choose to ignore, like petrol and food, the numbers look much better. And that’s the good news. Underlying, or core, inflation has continued to lift. And that’s what we want to see. Because rising inflation is a sign of strong growth and employment. Let’s take this as good news.

The report shouldn’t change anyone’s view on the NZ economy. Most of the risks we face are in the future. At a time when we forecast a meaningful lift in, fiscally stimulated, growth, the risks we face offshore are growing. The availability and price of credit (loans and mortgages) are also likely to be adversely impacted by the RBNZ’s assertive capital requirements on banks. But this will be a slow burn over the next five years. Our outlook is good, not great, and there are many risks.

For rates and currency market traders, there was no smoking gun. There is no definitive evidence to justify the rate cuts priced into the Kiwi interest rate curve. That doesn’t mean the cuts will or should be removed. Risks are aplenty.

Food and fuel prices slow CPI inflation

As expected, both food and fuel prices were key elements of the report. The food group fell 1.3%qoq as signalled earlier by the food price index. But a fall in food prices is typical at this time of year. Petrol prices were on average 0.6%qoq lower in Q4 as the slump in fuel prices seen at the end of the year. Importantly, we haven’t seen the last of the late-2018 drop in petrol prices. Lower petrol prices will also feed into the first quarter of 2019. And petrol prices have stabilised in January.

Working the other way, was a surprisingly large lift in prices of recreational good and services, which jumped 2.5%qoq. Also, the transport group rose 1.1%qoq as a seasonal jump in international airfares and vehicle rentals far outstripped the fall in fuel prices.

Non-tradables inflation is doing the heavy lifting

Non-tradables inflation – the domestically generated stuff - was much more solid than we and the RBNZ had expected. Non-tradables inflation came in at 0.7% in the quarter, to see annual non-tradables inflation lift 0.2%pts to 2.7%. Largely offsetting non tradables inflation was tradables, which fell 0.4% in the quarter, a sharper fall than we had anticipated.

StatsNZ also made a few tweaks to accommodation services in the December quarter. Stats has now split out overseas accommodation prepaid in NZ from domestic accommodation services and shifted it into tradables inflation. This exercise simply shuffling things around between tradables and on-tradables items. Headline inflation was not affected.

Core inflation is lifting

Offering some form of solace for the hawks was the fact that underlying measures of inflation held up well in the December quarter. Core inflation is an important guide to future inflation. Core measures reflect where inflation is likely to end-up once temporary shocks have faded. Core inflation is solid because of persistent and generally sticky areas of inflation, such as prices for housing and household utilities. On an annual basis, housing-related inflation came in again at 3.1% yoy. Rents, construction costs and council rates all contributed handsomely to the annual figure.

Looking more closely at core measures of inflation. Headline inflation less food, energy and fuel prices recorded a second consecutive 0.6%qoq lift and a 1.5%yoy annual rise – the strongest since the third quarter of 2017. Moreover, StatsNZ’s trimmed means measures, which removes volatile price swings from inflation, moved up to between 2.0-2.1%yoy across the different trim measures. Tthere is still underlying upward momentum in inflation at present, and it may be premature to talk about RBNZ OCR cuts. We await the RBNZ’s own core measure of CPI inflation, the sectoral factor models, to be released at 3pm today. Based on CPI figures released so far, there is a good chance the RBNZ’s meassure holds at recent levels – close to the middle of the RBNZ’s inflation target band.

Market Reaction

The Kiwi interest rate curve (swap rates) has hardly budged on the report. The 1 and 2-year rates are just 1.5 to 0.5bp higher, whereas the later rates (5-year and beyond) haven’t moved at time of writing.

The Kiwi dollar swooped into action, gliding higher to 0.6753, from 0.6720.

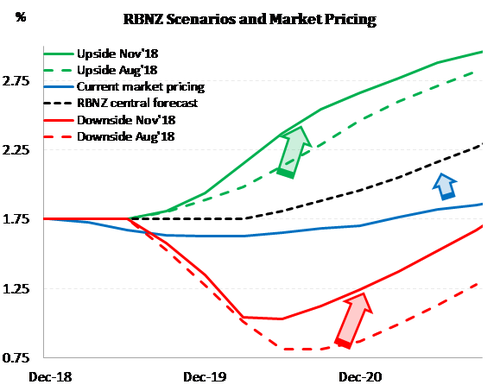

The rates market has moved further and further away from the RBNZ’s central OCR track – see the blue arrow in our chart. The market has a significant chance of an RBNZ OCR cut, or three, priced in. Before the release, the market had 13bps of a cut  priced in – so half a chance at a 25bp cut.

priced in – so half a chance at a 25bp cut.

Markets have been choppy of late. Because traders are nervous. The news flow has disappointed. Economic numbers are underwhelming. And we don’t like being underwhelmed.

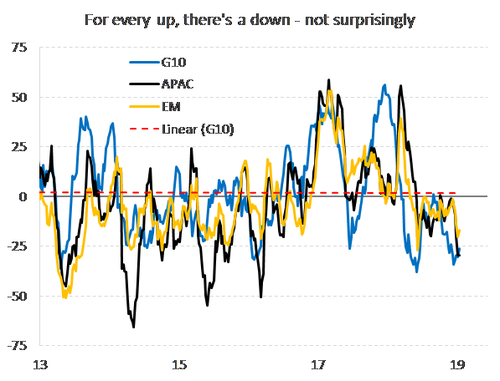

Citibank’s data surprise indices provide a snapshot of economic performance, relative to expectations. The world is a darker place. Our colourful picture paints an unfortunately ugly landscape. The economic news has been broadly negative. And there hasn’t been any escaping the headlines. Data surprise indices for Global, G10, EM, Asia, US, China, EU, UK, Australia and New Zealand have all nosedived into negative (we’re not happy) territory. The news out of the collective G10 has been loud, obnoxious, and unsatisfactory. The news out of the US has been loud, obnoxious, and unsatisfactory. Trump’s tweets have been loud,… ok, you get the picture.

The synchronised downturn in economic news versus expectations has driven somewhat panicked trading in financial markets. What is somewhat surprising in the unsurprising decline, is the diminishing reads in the EU. The Brexit burdened UK is actually holding up relatively well. That’s mainly because expectations are so deflated in the UK to begin with. Whereas they actually had hope a while back in the EU, and even told us they’d start tightening this year. Well, they won’t be tightening until they start getting positive news.

The cool thing about data surprise, is that we adjust to the news. The news is bad, so we revise down our expectations, and eventually get surprised on the upside (again). Upside surprises may be a risk in the second half of 2019. Wouldn’t that be a surprise!