- The Kiwi economy surged in the third quarter, up 2.0%. Economic output expanded well above our forecast (and market consensus) of 0.9%.

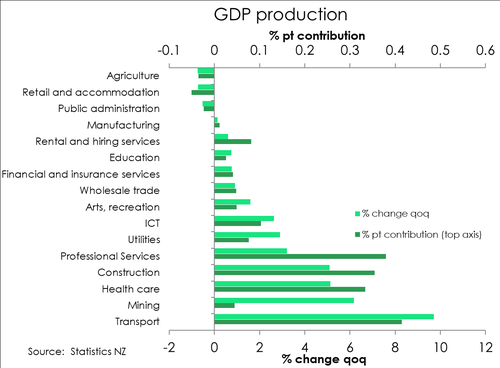

- The continued recovery in tourism over the quarter saw big gains in transport and recreational activities. The export of services posted another big double-digit increase. On the goods side, construction activity was up a strong 5.1%. And there’s still plenty in the pipeline. Although we expect a weakening over 2023.

- The RBNZ remains on an inflation fighting path. The headline GDP print came in above the RBNZ’s forecast of 0.8%. And we expect the RBNZ to deliver a 75bps hike in February to 5%. The RBNZ are planning on a further lift in the cash rate to 5.5%. We still see this as a step too far.

Void of any covid-related disruption, the Kiwi economy surged 2% in the September quarter. That’s an awesome print. And it came in above the upwardly revised 1.9% gain in the second quarter. The second quarter bounce came on the back of Omicron disruptions in the first quarter. On an annual basis, comparisons are complicated by last year’s Delta lockdown. Given such a low base, where output contracted, the Kiwi economy is a chunky 6.4% bigger than last year. That’s a great result, all things considered.

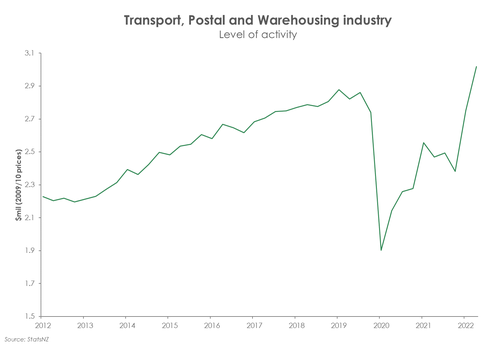

The report was incredibly strong with upward revisions. It was a services-led bounce. Mirroring the headline number, total services was up 2% in the quarter. And leading the way was the near-10% increase in the transport, postal and warehousing industry. There was also a large spike in export of services - so there's a strong tourism story coming through. Consistent with the recovery in tourism, recreational activity was up 1.6% in the quarter as well.

The large gain in construction was also a key feature of the report. Construction activity was incredibly strong, up 5.1%. And there's more in the pipeline - for a while at least. Investment in the construction space accelerated further in Q3, with residential building up 2.7% and non-residential up 4.7%.

The report is old, however. And there's no change to our outlook. Construction will be one of the major swings (south) over 2023. Household spending was weak in the quarter and will continue to soften over 2023, with rapid rate rises and falling property prices weighing on household confidence.

Financial markets reacted to the positive news, pushing wholesale interest rates and the Kiwi currency higher. Kiwi swap rates are factoring in a 73bp hike for February (we agree the RBNZ is most likely to deliver 75bps), and a 5.48% terminal cash rate (we reluctantly agree the RBNZ is likely to overtighten to 5.5%). The Kiwi currency is well supported around 64.5c and may push back above 65c. We think the reaction in financial markets will be short-lived, however. Global financial markets are still digesting the Fed’s decision to hike 50bps this morning, and looking for guidance from the BoE and ECB tonight.

Looking beyond the September quarter, the continued recovery in international tourism should see the economy close out the year on a positive note. After two summers without tourists, the sector is in for a busy one this year. The rebound in visitor arrivals should help a recovery in tourism and see the sector make a greater contribution to overall activity. A recovery in tourism however only delays an inevitable recession. With a weakening global economy and an exceptionally aggressive RBNZ, the outlook for Aotearoa is worsening.

Services still playing catch up.

Services were stonkingly strong in the September quarter. Total services, which represents two thirds of the economy, rose a solid 2%. And again, it was transport activity (air transport in particular) leading the way with a near 10% rise in the quarter alone. The September quarter captured the full reopening of our border. And the transport industry continues to make up for lost time. But the jump is largely a one-off. Such growth will eventually slow as border crossings normalise.

Services were stonkingly strong in the September quarter. Total services, which represents two thirds of the economy, rose a solid 2%. And again, it was transport activity (air transport in particular) leading the way with a near 10% rise in the quarter alone. The September quarter captured the full reopening of our border. And the transport industry continues to make up for lost time. But the jump is largely a one-off. Such growth will eventually slow as border crossings normalise.

Slightly offsetting the rise in transport was the fall in retail trade and accommodation, down 0.7% in the quarter. It’s a bit of payback from the 5% Omicron rebound in Q2, but also indicative of today’s environment. High consumer prices continue to weigh on households. Households are battling higher interest rates, falling house prices and an erosion of their purchasing power. The appetite for consumption is waning. Indeed, household consumption fell further in the September quarter, down 0.1% following Q2’s 3.4% decline.

Also within services, the health care sector posted an unusually large 5% gain in the quarter. It’s due to a shuffling around of activity from the public admin industry to the health care industry.

On an annual basis, the services industry claims the top prize for strongest growth. The impact of last year’s Delta lockdown was most pronounced on the services sector, with activity contracting 2.7%. But a year later, and the services industry is up 7.3% - a strong print given the soft starting point.

The goods-producing industry performed largely as expected. Helped mostly by construction, the industry posted the largest

quarterly growth across the three main industry groupings. Overall activity jumped 2.4%, following the deep 3.9% contraction

due to a reshuffling of business activity classification in Q2. Manufacturing jumped in Q3, but it was construction that’s the  darling of the goods-producing industry. Construction activity was incredibly strong over Q3, up 5.1%. Total building volume picked up the pace, rising 3.8%, following a 3.1% increase in Q2. Despite ongoing challenges with acquiring materials and staff, building activity continues to rise. And it looks like there’s still plenty in the pipeline that will support activity near term. Investment in construction – both residential and non-residential – accelerated in the September quarter.

darling of the goods-producing industry. Construction activity was incredibly strong over Q3, up 5.1%. Total building volume picked up the pace, rising 3.8%, following a 3.1% increase in Q2. Despite ongoing challenges with acquiring materials and staff, building activity continues to rise. And it looks like there’s still plenty in the pipeline that will support activity near term. Investment in construction – both residential and non-residential – accelerated in the September quarter.

Going the other way, the primary industries recorded a 0.2% drop in activity. Agriculture continues to battle unfavourable weather conditions. Activity contracted 1.4%. Offsetting this was a rebound in mining activity, up 6%.

Spending in the economy closely mirrored production.

On the other side of the same coin, expenditure GDP posted a solid 2% rise in the September quarter too. Mirroring the jump in transport and warehousing services, exports of goods and services were up 7.8%. The recovery in international tourism  continued in the quarter and bolstered services exports. However, goods exports, specifically dairy and meat, also experienced an impressive rise. The solid jump in construction activity in the production measure shined through in investment activity. The industry continues to chug through a significant backlog of house building. Infrastructure-related construction also featured in the quarter.

continued in the quarter and bolstered services exports. However, goods exports, specifically dairy and meat, also experienced an impressive rise. The solid jump in construction activity in the production measure shined through in investment activity. The industry continues to chug through a significant backlog of house building. Infrastructure-related construction also featured in the quarter.

Subtracting from GDP was a second consecutive fall in private consumption, albeit a small 0.1% contraction. Household spending looks to be wilting in the face of the surging cost of living, declining wealth – largely the result of falling house prices – and rising interest rates. In the September quarter consumers pullback on services related spending after several quarters of solid expansion. The relaxation of restrictions on socialising at the start of 2022 saw a jump in spending on hospitality and accommodation. More recently, a worsening economic outlook has seen consumers trim discretionary spending. Household belt tightening is likely to intensify over 2023.

Bigger than we had thought.

As is the case each September quarter, GDP data is subject to revisions as StatsNZ incorporates newly available, and more accurate, annual benchmark data. The latest revisions have lift GDP higher. Looking at GDP volumes, since the start of 2020 the size of the economy was an accumulative $8bn larger than we had thought at the June quarter.

The larger economy would go some way in explaining why for instance the Government’s tax take was surprisingly strong since Budget. The important thing for us though is that these revisions do little to change our forecast for a recession next year. The forces at play, such as the RBNZ’s aggressive tightening of monetary policy, will weigh much more heavily on demand in the coming quarters.

Tourists to the rescue.

Looking beyond the September quarter, the return of tourists should see the Kiwi economy close out the year on a positive note. As our drawbridge has been let down, we’ve seen an encouraging return of international visitors. Whether it’s our friends from across the Tasman or higher-spending travellers from the US, Canada or the UK – they’re all coming back. Tourism was once our biggest export industry, contributing 20% of total exports. That contribution has fallen to 2%. And currently, international tourism spend is down over 90% on 2019 levels. But after two summers without tourists, the sector is in for a busy one this year. The rebound in visitor arrivals should help a recovery in tourism and see the sector make a greater contribution to overall activity. And the return of tourists comes at an opportune time. Because the spend up of foreign dollars will help to offset the weakening demand by Kiwi consumers. However, the ability of the tourism sector to service increased demand comes into question given the resourcing constraints (particularly staffing) the sector faces. The summer period is typically the peak in international tourism. And the sector may struggle to keep up.

The inevitable.

The global economy is weakening, and so too is ours. Consumer confidence is subdued, business investment intentions are deteriorating, and the housing market remains in a downtrend. But the RBNZ have unambiguously signalled further increases to the cash rate. Because at 7.2%, Kiwi inflation remains uncomfortably strong. And stubbornly high inflation expectations are testing the RBNZ’s inflation-fighting credibility. The RBNZ is firmly fixated on returning inflation to target. And there was nothing in today’s report that would have rocked their resolve.

But an exceptionally aggressive RBNZ means a recession is an inevitable outcome. Much higher interest rates are being set to reduce demand (namely household consumption) to better meet constrained supply. But the sheer weight of rising interest rates is set to push the economy into recession from the middle of next year. We are forecasting a three-quarter contraction in activity from the June quarter to leave the economy 0.7% smaller at the end of 2023.