Crystal ball gazing conjures up three P’s of property: Population, Preference, and Policy…

…and we’re Painfully undersupplied.

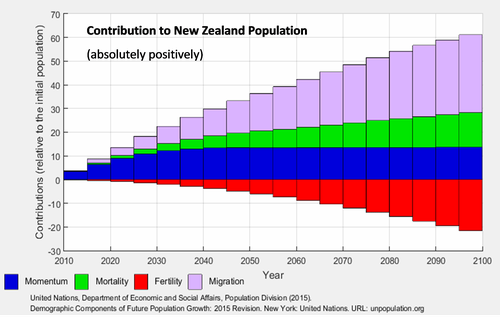

- The largest migration boom ever recorded is receding, slowly. But we will remain attractive to migrants, and our population won’t peak.

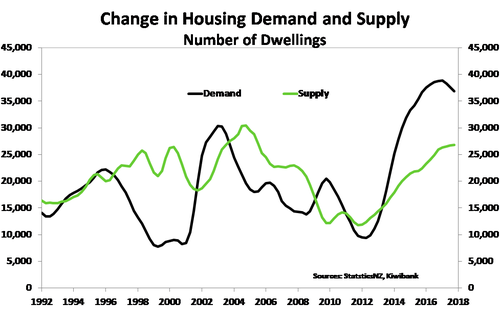

- We have a shortage of over 100,000 homes. Supply has not kept pace with demand. Demand is still growing, capacity constraints are being hit, and we need more affordable dwellings.

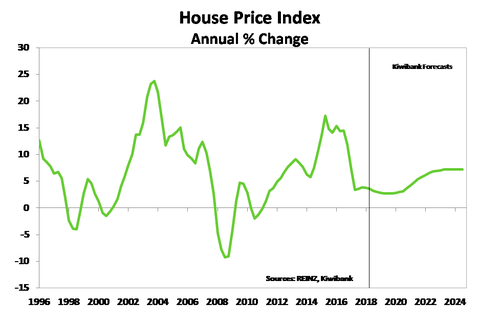

- Policy changes, like capital gains tax, will hinder confidence. But the fundamentals outweigh tweaks to taxes. We expect property prices to consolidate, before regaining traction into the mid-2020s – aided by income and population growth.

The Kiwi housing market has recovered from the lows in sales recorded last year. National house prices are up 4% yoy. Although gains are largely being made in the regions, as they play catch-up. Auckland’s market remains muted. Investors are uncertain, and therefore cautious. The Government is gearing up to implement policies targeted at speculators. These policies include tightening the bright-line capital gains test, removing the negative gearing tax loophole and banning foreign purchases of existing stock. The policies, and the uncertainty associated with them, may hold back house prices over the next few years. But we don’t expect a major correction in housing. Because the fundamentals are solid, and there are no signs of any sinkholes.

The housing market is undersupplied and mortgage rates are low. And unemployment is likely to fall, not rise sharply. Housing corrections are often driven by haemorrhaging households suddenly unemployed or lumped with rampantly rising interest rates. Neither is expected. The jobs market should remain tight. And the RBNZ will keep interest rates low. Mortgage rates will rise eventually, however.

When gazing into the property crystal ball, you must conjure up the three Ps: Population, Preference, and Policy. And we see a Kiwi property market far from the precipice. We forecast a period of consolidation due to investor restraint, rising interest rates, and a lift in supply into the 2020s. Auckland house prices are consolidating; and the risk is they fall, but not far. A small fall would be a slight correction from past excesses. We forecast a meaningful lift in prices, nationally, into the mid-2020s.

Population growth may be peaking, but will not contract.

The first step to analysing any market, is establishing demand. The more people we have, the more houses we need. Population has outgrown supply of housing for 10 years. We are undersupplied, and we are not stationary. Our population will continue to increase, and for the next hundred years according to UN guesstimates.

New Zealand has had rapid population growth over the last five years, adding 420,000 people (mostly migration). Prior to 2013 it took twice as long to expand by the same number. Migration flows are multifaceted; fewer Kiwis have left, more Kiwis have come home, and we continue to attract foreigners. The rapid rise in population has compounded the shortage in housing. The shortage is particularly acute in Auckland, the first port of call for many migrants. The RBNZ estimates Auckland would have built 40,000-55,000 more homes from 1996 to 2016 had it matched building rates in the rest of the country (RBNZ Discussion Paper). The shortage continues to compound today, based on our estimates.

New Zealand has had rapid population growth over the last five years, adding 420,000 people (mostly migration). Prior to 2013 it took twice as long to expand by the same number. Migration flows are multifaceted; fewer Kiwis have left, more Kiwis have come home, and we continue to attract foreigners. The rapid rise in population has compounded the shortage in housing. The shortage is particularly acute in Auckland, the first port of call for many migrants. The RBNZ estimates Auckland would have built 40,000-55,000 more homes from 1996 to 2016 had it matched building rates in the rest of the country (RBNZ Discussion Paper). The shortage continues to compound today, based on our estimates.

Population growth has started to slow, as net migration eases from record highs. The drop off has been driven by a rise in non-NZ citizen departures. Even with the forecast pull back in migrant intake, it will take some time before the rate of construction matches demand. Even if, or when, construction catches up with increased demand, there is still the cumulative housing shortage to address. Our analysis shows a national housing shortfall of over 100,000 homes. And the shortage will to get worse before it gets better. At current rates of construction, it could take several years to alleviate the housing shortage. Despite what happens around the edges of the market, including tax changes, there is plenty of work for the foreseeable future. The mighty Kiwibuild will help, even if there is some crowding out (economist speak for ‘some of it was going to be done anyway’).

It is all fine and good to want to build. It’s even better that we’re prepared to pay to build. But it’s hopeless if we don’t have the capacity to build. The RBNZ estimate there is a 9,000 shortage of residential construction workers in Auckland alone. Auckland building consents are finally closing in on the highs recorded over a decade ago. In the year to May there were 12,300 dwelling consents issued. A most welcome development. But it remains to be seen whether Auckland can maintain the burgeoning pipeline, given the capacity constraints already felt. And housing supply concerns are no longer just an Auckland issue. A number of the regions around the country have seen growth in demand outstrip construction, including Waikato, Wellington, and the Hawke’s Bay.

So in terms of undersupply becoming oversupply and fuelling a housing market correction, we don’t see it. Not in the next 10 years at least. This is neither good nor bad news. It’s a source of continued frustration. Only significant investment, and some creative policies (on migration) to alleviate labour shortages will address imbalances, over the long term.

Preferences change, ever so slowly.

Let’s face it, the “Kiwi dream” of the quarter acre block overlooking water is only available to a select few. And even the select few who own such a dream face significant gains in subdividing. Once the kids have flown the coop, the need to hold onto a massive backyard diminishes. We have a huge intergenerational transition taking place. The baby boomers are retiring. And when you retire, you might look to unlock some of your land-locked wealth (if you have it). We’re seeing some Auckland boomers, as a prime example, leaving in droves for the cheaper regions. And why wouldn’t you? The exodus of some Aucklanders has boosted surrounding regions, namely Northland, Manawatū-Whanganui, Waikato, and the mighty Hawke’s bay. Our preferences are ever-changing.

The regions are becoming increasingly attractive to retiring boomers. The regions are also becoming increasingly attractive to younger Aucklanders, priced out of Auckland. Regional house prices are rising as a result.

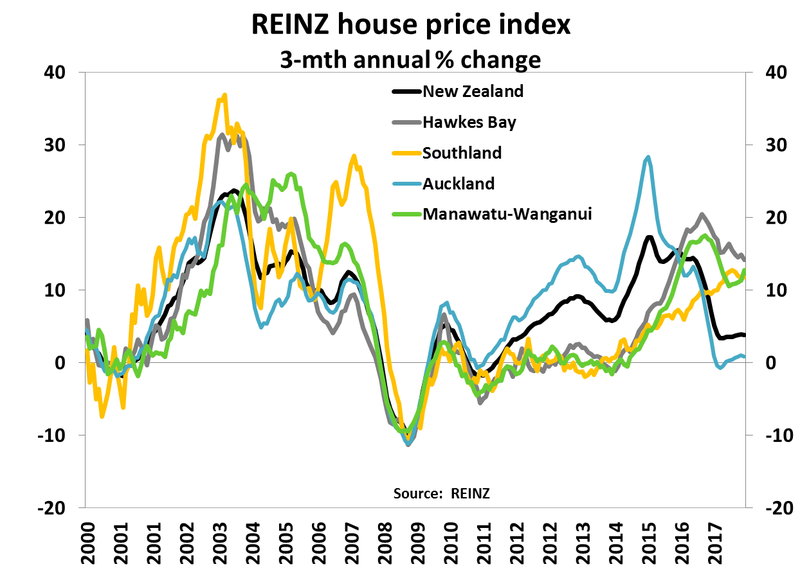

The wind has died down in the City of Sails. Following a period of heated activity, Auckland’s housing has been put on ice, and has diverged from most parts of the country. Annual house price growth in Auckland is just above zero. In contrast, house price gains are notably higher in most other parts of the country, as regions play catch-up to Auckland. Sales activity has picked up off the floor in Auckland, and is now rising. But activity is still low compared to a few years ago.

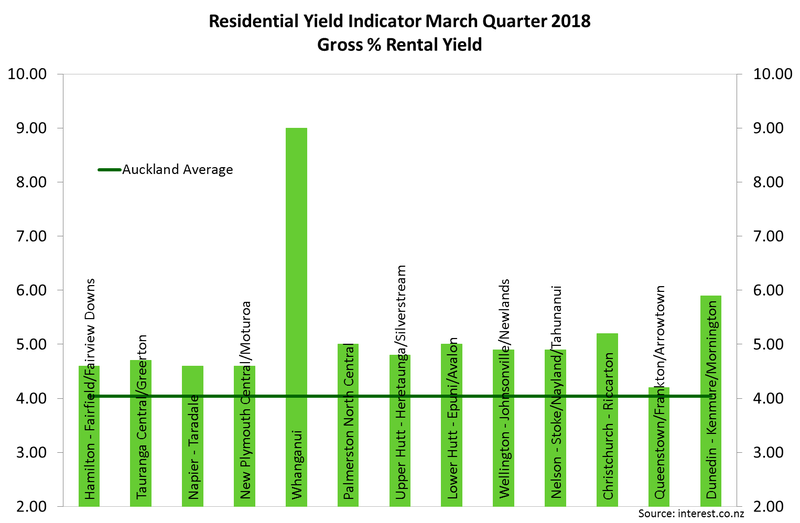

Sales activity quietened quickly across NZ in 2017, but a few regions have experienced a decent recovery. The “hot” areas now include parts of Gisborne, Rotorua, the Hawke’s Bay, and Manawatū-Whanganui. And the feverish feeling on the ground is seen with shortened times properties spend on market. There’s been a flood of interest from northerners (Aucklanders) on a southern pilgrimage. House price growth reached 13% in May in Manawatū-Whanganui, on par with the rate seen in July last year. Southland is also a part of the country that has shown a little more resilience in sales activity, and house prices have lifted 12% yoy in May, compared to 9.5% yoy a year ago. Interestingly, these standout regions also have some of the highest rental yields in the country. Give them yield, and investors will come.

For property investors searching for yield, places like the Hawke’s Bay may offer a higher return. Whanganui is off the charts, offering 9% rental yield. Also, the RBNZ’s loan-to-value ratio (LVR) on investor-related lending may have forced investors to look at cheaper property, given the reduction in available leverage (or larger deposit required). $100,000 deposit goes a lot further south of the Auckland border. North of border, the wildlings have encountered more Aucklanders in search of cheaper dwellings. Mangawhai has experienced a surge of Aucklanders willing to live on the outskirts of the supercity, and commute the vast distance back. Agents on the ground say ~500 people a day commute from Mangawhai to Auckland, spending a good 1.5-2 hours in a car EACH way. At least they fall outside Auckland’s petrol levy…

The Canterbury housing market is in a cool, still wearing a swanndri category, for reasons specific to the region. For too many years now, the market has been distorted by the post-quake rebuild. The resulting recovery in housing supply has had a depressing effect on the housing market. House price appreciation in the region did not experience the highs seen elsewhere. More recently, house prices in Canterbury have flatlined, and so too have sales and activity.

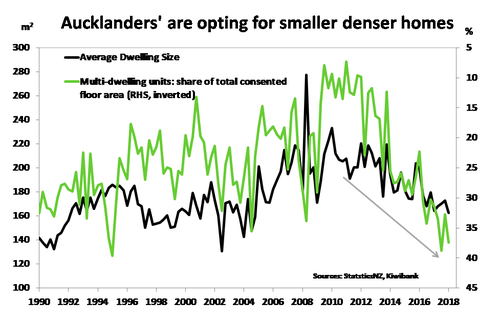

More of us prefer higher-density dwellings. Apartments are often surrounded by funky cafes and shops, and situated without crazy commutes. We have also attracted a large number of Asian migrants in recent years. Indian and Chinese migrants come from a higher density background. A 70sqm apartment is huge in comparison to Mumbai or Shanghai, for example. City hubs, like Chatswood in Sydney, have attracted Asian migrants, and driven prices beyond surrounding, previously more expensive (old money), suburbs. The same can be said for parts of Auckland. The desire for a quarter acre block is simply too hard in parts. And our tastes are changing anyway.

We either accept a higher-density dwelling, or move to a lower density region. Planning for higher density dwellings in Auckland is a long and difficult process. There’s a shortfall of construction workers. And the super-city’s infrastructure falls short of expanding needs. Investment is slow, and short of forecast demand. Planned investment into the regions will help hasten inter-regional migration, out of Auckland. Again, more investment is needed into the regions. The Government is in the process of boosting infrastructure spending into the regions. Policy can help.

Policy can have an impact, if only temporarily this time.

The most valuable attraction to our property market, is something we all take for granted. English property rights attract foreign buyers. Our legal rights are as stable as New Zealand itself. And New Zealand is one of the most stable countries, rated AAA under Moody’s and AA+ under S&P. The risk of losing access to your (foreign) money invested in NZ property is very slim indeed. Our property rights are attractive. And property is seen by some foreign investors as a safety deposit box. It doesn’t mean you won’t get taxed, however. And it doesn’t mean you shouldn’t. There are a number of countries forcing foreigners to pay to play. They all have two things in common: English property rights, and Chinese buyers. The wave of Chinese buying has cooled, significantly. Chinese policy has changed too.

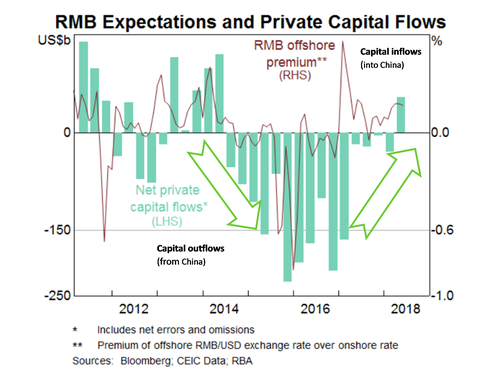

The massive capital outflows from China seen over 2014-2016 have stopped and started to reverse. China took steps to control its currency, the renminbi (RMB), in 2017. It is now much harder to take money out. It is no coincidence, in our opinion, that Auckland, Sydney, Melbourne, Vancouver, Singapore and parts of the US markets have all slowed down in response to either taxes on foreign buying, and/or the latest strangling of funds out of China itself. According to Juwai.com, a Chinese property platform, Chinese buying of overseas residential property fell 25% in 2017. Chinese policy changes may continue to impact our (mainly Auckland) market. In time, we would expect China to allow outflows to return. Although foreign policy is important to consider, local policy is much more important.

The massive capital outflows from China seen over 2014-2016 have stopped and started to reverse. China took steps to control its currency, the renminbi (RMB), in 2017. It is now much harder to take money out. It is no coincidence, in our opinion, that Auckland, Sydney, Melbourne, Vancouver, Singapore and parts of the US markets have all slowed down in response to either taxes on foreign buying, and/or the latest strangling of funds out of China itself. According to Juwai.com, a Chinese property platform, Chinese buying of overseas residential property fell 25% in 2017. Chinese policy changes may continue to impact our (mainly Auckland) market. In time, we would expect China to allow outflows to return. Although foreign policy is important to consider, local policy is much more important.

Compared to other asset classes, equities for example, there is a significant tax advantage in property investment in NZ. Last year’s change in government has heralded a number of policy changes, primarily aimed at investors. Policy changes include:

- The tightening of the bright-line capital gains test from 2 to 5 years (already in place);

- The removal of the negative gearing tax loophole; and

- Banning foreign purchases from the exiting housing stock (Overseas Investment Amendment Bill still working its way through Parliament).

We believe a combination, or all of the above, changes coming through will impact growth, but not the direction of our property market. Remember, you only pay these taxes when you have made money. The changes may influence the amount of risk, leverage investors are willing to take, but we doubt they will cause an exodus from the market. Only time will tell, and it’s obviously dependant on which polices are passed and how far they go.

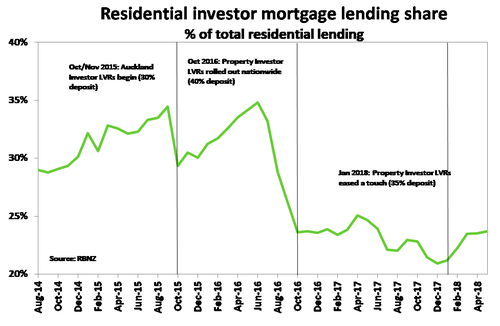

Another element of policy to keep an eye on is that which is directed by the RBNZ. At present the RBNZ is simply in no hurry to raise interest rates until at least the second half of next year. For investors, when the RBNZ is ready to hike rates, the speed will be gradual and the amount will be small compared to previous hiking cycles. On the RBNZ’s macroprudential policy, we don’t see the RBNZ loosening loan-to-value ratio (LVR) restrictions by much, or anytime soon. Loosening macroprudential policy may work against future tightening of monetary policy, as the Bank moves to tame rising inflation. Moreover, the RBNZ outlined three criteria that would need to be satisfied if it was to loosen LVRs, these include:

- Evidence that house price and credit growth have fallen to around the rate of household income growth.

- A low risk of housing market resurgence once LVR restrictions are eased.

- Confidence that an easing in policy will not undermine the resilience of the financial system.

One could argue all 3 have been met, but it’s certainly not definitive. Credit growth is slowing, but household income growth has yet to lift materially. The need to guard against excessive leverage building in parts of the system remains. But credit quality has improved materially since 2016. We believe the 2nd and 3rd requirements are easier to argue, now that the housing market has cooled, with Auckland’s lead. The 1st is a matter of judgement.

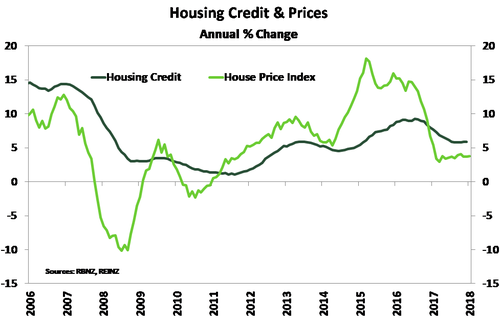

Housing credit growth has slowed since its recent peak at the beginning of 2017 (see chart). The slowdown was orchestrated by the RBNZ via tighter LVR restrictions on investor related lending, and tightening of lending across the banking industry. Credit growth has now stabilised around 6% yoy. However, credit growth still looks to be a small distance above household income growth.

Housing credit growth has slowed since its recent peak at the beginning of 2017 (see chart). The slowdown was orchestrated by the RBNZ via tighter LVR restrictions on investor related lending, and tightening of lending across the banking industry. Credit growth has now stabilised around 6% yoy. However, credit growth still looks to be a small distance above household income growth.

We know that a big element of household income growth, wage and salary growth, has been muted for a considerable period. While we expect household income growth to improve, as wages are poised to lift, its may be sometime before the RBNZ’s LVR criteria will be met. And if the RBNZ deems the criteria to be meet in the next year, we would only expect a modest adjustment akin to the last in November 2017 – shaving the LVR by 5%, and allowing a 35% deposit (down from 40%). Not a big move at all.

Box A: A shortage of homes should provide a floor under prices

New Zealand’s housing shortage, is a key factor that should keep house prices from falling significantly. The shortfall of housing is not evenly distributed across the country, with Auckland having a well-documented shortage for several years now. The RBNZ recently published a paper that estimates, relative to the rest of NZ, home building in Auckland was 40,000-50,000 short of what would be expected between 1996 and 2016 given rapid population growth. Housing shortages are not just an Auckland experience though, with places such as Hamilton, Palmerston North and Wellington also showing evidence of a shortage.

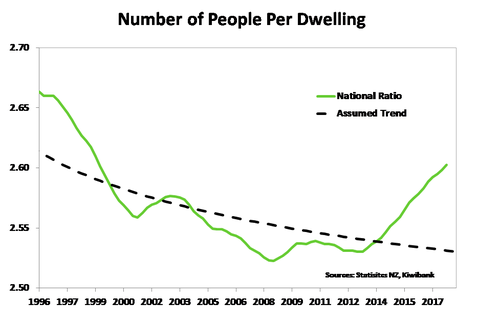

Estimating the scale of the national housing shortage is far from easy. But the number of people-per-dwelling (see chart below) can tell us something of the balance between housing supply and demand. Over time this ratio has trended lower because of shrinking family sizes, NZ’s aging population, and changing preferences. Under these conditions, housing demand will tend to grow faster than the general population. Therefore, if the number of people-per-dwelling takes off, as we have seen since 2013, housing supply is likely to be failing to keep up with demand. Think battery hens, rather than free range.

People-per-dwelling goes through cycles, but we are confident that over time it trends lower, especially given our ageing demographic. We have estimated a simple trend based on historical data that reflects the natural tendency of people-per-dwelling to fall (see chart). Using our people-per-dwelling trend we can then estimate the quarterly surplus/shortage of housing by figuring out how much larger construction activity would have to be for the number of people-per-dwelling to fall back to trend. However, more important for the housing market is the size of the cumulative shortage of housing.

To estimate the shortage, we need to know a point in time when NZ housing demand and supply was in balance. A likely period looks to be in the early 2000s. At the turn of the century the NZ economy was recovering from the fallout of the Asian financial crisis. Population growth was low, housing market activity was subdued, and the level of building consents had been drifting sideways for a few years. This all changed in the early 2000s, housing market activity took off, building consents then followed, and by early 2004 national house price appreciation peaked at over 20% yoy. It is likely that at some point over this period housing demand and supply were balanced. Based on our analysis, we estimate that since late 2002 NZ has accumulated a shortage of a little over 100,000 homes – most of which was generated in the past five years.

With population still growing above average, albeit slowing, the 100,000 shortage is likely to get worse before it gets better. The current supply response, including the Government’s Kiwibuild programme, will eventually eat into NZ’s shortage. Until then though, excess demand for housing is likely to keep house prices from falling sharply.

We provide some thoughts, and anecdotes, on the regions below.

We shine the spotlight on a few regions of interest.

Auckland is truly a supercity in size, and problems.

Auckland is truly a supercity in size, and problems.

The supercity has seen a supersized 40% surge in population this century, with a 10% jump in recent years. Housing supply has lagged. Auckland’s housing marketing has now cooled, and officially gone no-where in the last year. But it feels like it has gone backwards, a bit. Properties are regularly trading below CV – a product of high CVs and a softening market. Capacity constraints in construction are most acute. And the haemorrhaging of construction companies, such as Ebert, point to wider issues, and potential credit constraints going forward. The availability of credit may shrink. We expect a continued consolidation in Auckland house prices, with the risk of a mild contraction (around 3-5%). Any correction is likely to be mild, however, and would simply give back a fraction of past excesses. Affordability is a real problem. The cooling in migration and pull back in foreign interest will dampen pressures. The fact Auckland is massively under-supplied, suggests to us house prices will struggle to fall too far. And Barfoot and Thompson data show a plateauing in price, and agents expect a bounce in spring. We believe a meaningful 10-20% correction in prices is highly unlikely without a serious downturn, inducing a significant spike in unemployment. We don’t see that happening, despite all the risks brewing offshore.

Wellington is (finally) experiencing some growth.

Wellington is (finally) experiencing some growth.

Wellington has seen a 20% increase in population this century, with a meaningful 5% uplift in recent years.

“Wellington’s housing market is still fairly buoyant with large groups still attending open homes, even over the winter period. The number of offers on each property appears to have eased in the last 6 months, but there is still enough competition to sustain house prices. The investment market has slowed considerably since the LVR restrictions, but has really opened the door for first home buyers. We’re seeing a lot of activity with first home purchases and movers (from one property to another) in parts of Wellington Market, as house prices in Porirua and pockets of the Hutt Valley are still under the 500k cap. Kiwisaver is now a massive part of the First home buying process with almost all first home buyers accessing Kiwisaver for their first house purchase.” Shayne Hawtin, MMM (Triple M, is Mobile Mortgage Manager)

Whanganui is yielding above and beyond and attracting Northlanders.

Whanganui is yielding above and beyond and attracting Northlanders.

The Manawatū-Whanganui region’s population has hovered around 230k for years. But like most regions, population has lifted recently. And Aucklanders are to blame. The region’s population has lifted just 3% this century. All of that gain has occurred in the last few years.

“Customers and Accountants advise that Whanganui confidence is high, with tradies having to turn work away. Businesses are looking to increase staff levels but are finding it difficult to find good staff. There is a shortage of rental properties and houses on the market, due to new properties not being built for a number of years which in turn is creating demand/increased prices. There is also demand for vacant commercial land to develop, with 3 retail clients coming into town looking for space.” Natalie Sara, Business Manager.

The Hawkish Hawke’s Bay has been hectic, but is hibernating this winter.

The Hawkish Hawke’s Bay has been hectic, but is hibernating this winter.

The mighty bay has had its fair share of migrating Aucklanders. The pip fruit industry is outperforming, and the bay is vibrant. Population growth has lifted recently, and the bay is 3% larger (11% this century).

“Anecdotally, it feels like price growth has now stalled in the cities. Whether this is a seasonal winter blip or the start of price growth softening in Napier and Hastings won’t be known until the Spring sales kick-in. Outer lying areas such as Central Hawke’s Bay have enjoyed significant price growth over the last year. Rental stock remains in short supply. Commercial property continues to see a flight to quality, with satisfactory NBS ratings crucial to attracting national tenants.” Garth Duncan, Commercial Manager.

“Taupo/New Plymouth/Palmerston North/Hawke’s Bay: The same story across all these markets. Stable, but vendors are having to be more realistic about meeting the market. Where vendors pitch for top dollar, they’re finding buyers are backing away. A small power shift towards buyers, but sellers still generally hold all the picture cards.” Andrew Holford, Regional Manager

Gisborne is strong, really strong.

Gisborne is strong, really strong.

“Strong market if you’re selling. Sales volumes maintained but shortage of stock apparent with continuing upwards pressure on price.” Andrew Holford, Regional Manager

“The hospitality and trade sector labour market is somewhat of a pressure cooker, with customers struggling to fill vacancies advertised 12mths ago on the back of zero rental properties available or a willingness of owners to take properties off AIR BnB. With the looming summer months ahead and influx of tourists be prepared to wait 90mins for sirloin steak sandwich 😊.” Nick Hosking, Commercial Manager

The Bay with Plenty to offer.

The Bay with Plenty to offer.

“The completion next year of the Waikato Uni Campus will see an influx of students to the Bay, and we are now seeing proposals for large high-rise student accommodation, which in turn should have a flow on effect for retailers, and add much needed people to the CBD. Businesses are struggling to accommodate demand for services due to the lack of labour across all sectors.” Nick Hosking, Commercial Manager

Waikato is strong enough.

Waikato is strong enough.

“Housing continues to deliver growth in values and rents with continued demand. There has been a reduction in vacancies of retail, office, commercial and industrial space. Industries such as construction and civil works continue to be strong, however there is a finite time line to this with the completion of the Hamilton and Huntly bypasses in 2020. Fieldays activity was strong with record visitor numbers, increased retail sales and solid sales and enquiries on big ticket items. A number of our customers have said it was their best Fieldays ever.” Lloyd Upston, Business Manager

Christchurch has fallen into a relaxed hibernation.

Christchurch has fallen into a relaxed hibernation.

“I’d give ChCh a rating of 5 out of 10. The market is pretty quiet overall. Having had discussions with Mobile Mortgage Manager’s (MMMs) and real estate agents, the general feeling is that the market has gone into a form of relaxed hibernation. ChCh already seemed like it was heading that way about a year ago, and apart from a brief end of summer surge of activity (which is normal), things have been pretty slow. The investor market has died a death with weakening values in ChCh (E-Values seems to point at this too), and RBNZ LVR restrictions seem to have had the desired effect of cooling things off. On the flip side we’re seeing a resurgence in first home buyers. We are seeing more FHBers building, which is symptomatic of the way ChCh has been going. Many building companies are targeting these buyers. I still think there’s an over-supply of new houses here in ChCh, but time will tell. Hopefully as spring starts to poke its nose around the corner we’ll start to see a lift in activity, particularly if rates stay low like they are.” Alan Bush, MMM

Dunedin feels good, really good.

Dunedin feels good, really good.

It seems Aucklanders are travelling further south. “Dunedin feels like a 7, out of 10. Demand is still high as there seems to be a shortage of available properties, with most new listings selling very quickly and barely enough coming on the market to replace them. Clients are trying to purchase with multiple offers on the table and are telling us that there are large numbers of buyers turning up at open homes. We are also seeing an increase in buyers looking to purchase in the over $500k price range. A slight slowdown over the last couple of week but there’s still a large number of pre-approved customers out there searching for properties. There is a steady number of owner occupiers upgrading their homes and investors purchasing investment properties. First Home Buyers are also competing in the same market. Feels like there are a number of customers moving into the area from overseas and also buyers relocating from Auckland. Given it’s winter the number of applications and enquiries have remained steady.” Leanne Hannah, MMM

Nelson feels fine.

Nelson feels fine.

“Nelson feels like a 6. At present the market feels slow, with buyers not showing any urgency. This time of year is traditionally slow with vendors waiting for spring to list properties to obtain the best price. Town is quiet with a lot of commercial space available in the CBD. Tourism has also slowed down over winter months, even with the highway to Christchurch via Kaikoura now open.” Simon Parle, MMM

North of the wall, and the wildlings are busy preparing for winter.

North of the wall, and the wildlings are busy preparing for winter.

“Northland continues to be buoyed by the construction sector and ever-present requirement for affordable homes. The progression of the Hundertwasser project, along with granting of consent for expanding the ports berthing capacity and talks of a 200million convention centre are driving positivity in the region; as a result businesses are using the last two years successes to grow and diversify. A good time to be a business in northland.” Clarc Morris, Senior Business Manager