The labour market is tighter than a year ago, weaker than a quarter ago, and lazy in filling out forms.

Here are the Key Points

- The labour force survey was longer, and led to interview fatigue. The response rate to the new, and 20min extended, survey fell away. It’s harder to read.

- At face value, employment growth stalled, unemployment rose, and participation fell. None of this is good. But the report’s face value has declined.

- The labour market has clearly tightened over the last year. And the unemployment rate of 4.3%, is still a smidge below the RBNZ’s forecast 4.4%. We’re on track.

- The risk of an RBNZ rate cut has risen, meaningfully, in recent months. Because offshore developments have worsened, and the outlook for credit growth is clouded.

Our take on the data

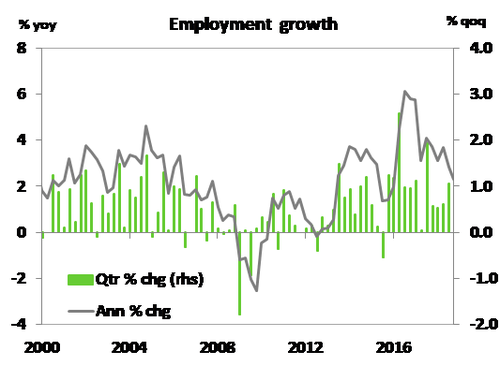

The December quarter labour market data revealed more payback in the numbers than we had expected. In the Household Labour Force Survey (HLFS) the unemployment rate rebounded to 4.3% from an upwardly revised 4.0% recorded in Q3 – this is higher than the 4.1% we and the market had expected. Employment growth was soft too, up just 0.1%qoq compared to the solid 1%qoq recorded in the previous quarter. On an annual basis employment growth slowed to 2.3%yoy from 2.8%yoy.

However, StatsNZ noted that the addition of the one-off Survey of Working Life (accompanying the HLFS) distorted things a bit. It is believed that some respondents may have said that they were not in the labour force, when in fact they were employed, just to avoid answering the additional (+20min) survey. StatsNZ made some adjustments to account for this behaviour and issued caveats. Had these adjustments not be made, the unemployment rate may have been more like 4.4% – reversing the entire drop recorded in Q3. Wage growth was in line with our expectations in the December quarter. Another 0.5%qoq increase was recorded in the private sector Labour Cost Index (LCI) to take annual wage inflation to 2%yoy. Further wage inflation is coming. We have a sizable $1.20/hr lift in the minimum wage to $17.70/hr to come into effect from 1 April this year. In addition, firms continue to express difficulty in finding staff.

StatsNZ noted that for the December quarter that longer term trends provide a better steer on the direction of the labour market. We couldn’t agree more. Over the last year the direction of the labour market has generally been one way. That is, the labour market has tightened, demand for labour has been more than enough to offset a growing labour force, and wages are rising. Compared to the RBNZ’s November Monetary Policy Statement (MPS) forecasts the labour market is developing in line with their view. As a result, there is likely to be limited implications from today’s labour market report for next Wednesday’s February (MPS). Financial markets are more focused on global developments, such as a slowing Chinese economy, US-Chinese trade negotiations, and to a lesser extent Brexit. We still maintain our view that the RBNZ will keep the cash rate unchanged at 1.75% this year and will begin gradually hiking from mid-2020. Since the start of 2019 risk to our view have clearly shifted to the downside.

Market reaction

Kiwi interest rates declined immediately upon release of the awkward numbers. The focal point of the Kiwi interest rate curve is the 2-year swap rate. The 2-year rate (used by banks to manage 2-year fixed rate mortgages) declined to 1.85% - the lowest level ever. The 5-year rate didn’t want to be left behind and nosedived to 2.01% – the lowest level ever. The 10-year swap rate fell to 2.45% – NOT the lowest rate ever. The lowest 10-year rate was 2.36% in 2016 – remember, when Brexit was voted. Imagine where it would go if Brexit is implemented. The bigger picture is important here. Interest rates are low, and likely to fall further in the near term. Our Government can issue 10-year paper (IOUs) at less than 2.2%! We’d argue they could issue 30-year paper from less than 3%. And international investors would line up to buy in size. Access to cash is not our problem. High interest rates are not our problem. Accessing the funds to build quality infrastructure is our problem. Because we have a shortage of workers to complete the projects… Our labour force is actually too tight in large parts.

The little Kiwi flyer has soared against the Aussie battler, breaking through 96c. The Kiwi/Aussie currency cross was as low as $0.9370 last week, and had found some wind beneath tiny wings. The Aussie economy is cooling, and the housing market is falling. Calls for Reserve Bank of Australia (RBA) rate cuts are growing louder, and louder. So relative to OZ, our currency is that much more attractive – well, until today! After a strong run, the Kiwi was dumped, and the Kiwi/Aussie crossed dropped from near 96 to near 95.