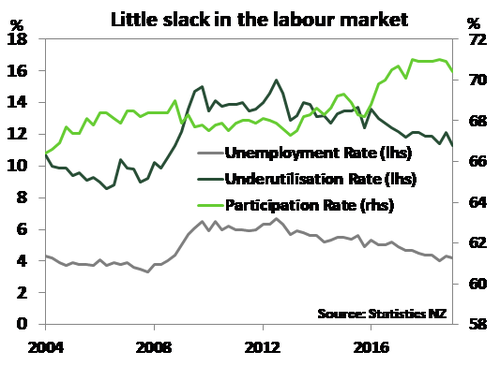

The unemployment rate of 4.2% is solid.

Image source: Sweet Ice Cream Photography

Key Points

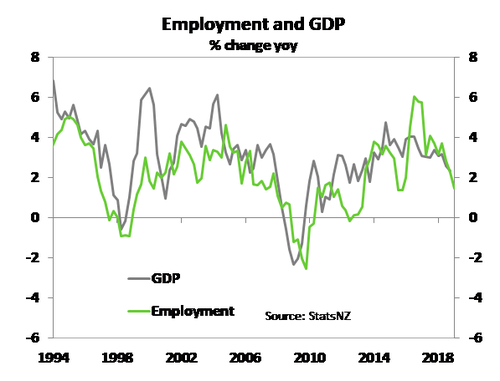

- The Kiwi employment report was weaker than expected. The number of jobs fell 0.2% in Q1. Growth in employment has lost momentum.

- Kiwi were also discouraged, with a fall in the participation rate. But the decline in unemployed people was greater, pushing the unemployment rate down at 4.2%.

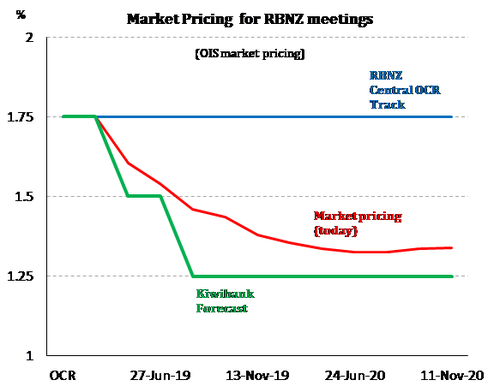

- The labour market stats are what we call a lagging indicator. They take a while to turn. And the softness in the numbers reflects the pessimism in the business surveys. The report won’t add a great deal to the RBNZ deliberations this week, and next. We believe the RBNZ will deliver a 25bp cut to 1.5%.

Summary

We will start with the good news. The number of people unemployed fell, and the unemployment rate dropped to just 4.2%. Estimates of “full employment”, a mythical rate we aspire to achieve, are around 4-to-4.5%. We we’re doing well.

The concerning news, was the drop in the participation rate. At face value, potential workers were seemingly discouraged. And employment growth has lost momentum.

We were surprised by the weakness of employment growth. The softening casts another slightly dim light on next week’s MPS. A low unemployment rate at 4.2% and an employment rate (of 67.5%) at historically elevated levels, means the RBNZ can still take comfort in knowing that it’s meeting its maximum sustainable employment mandate. But for how long? With signs of a slowing economy, the RBNZ is unlikely to rest on its laurels.

We were surprised by the weakness of employment growth. The softening casts another slightly dim light on next week’s MPS. A low unemployment rate at 4.2% and an employment rate (of 67.5%) at historically elevated levels, means the RBNZ can still take comfort in knowing that it’s meeting its maximum sustainable employment mandate. But for how long? With signs of a slowing economy, the RBNZ is unlikely to rest on its laurels.

We expect the RBNZ to deliver a 25bp cut to the OCR to 1.50% next week.

Employment disappoints

Despite a surprise 0.2%qoq fall in employment in the March quarter, the unemployment rate managed to ease back to 4.2% as we had expected. The saving grace was a much sharper drop in the labour force participation rate than had been expected. The participation rate fell to 70.4% the lowest since mid-2017 and down from the recent record of 71.0% seen in Q3 last year. It’s hard to know if this fall in the participation rate will be sustained – this number does jump around a bit, and we have seen the fall in net migration start to stabilise.

Employment growth is slowing. Compared to last year, employment was 38,500 higher or up 1.5%yoy. That’s a big stepdown from the 2-4%yoy rate of growth recorded over the last 18 months. Similarly, the Quarterly Employment Survey’s (QES), a survey of businesses rather than households, showed that total filled jobs in the quarter were 0.1%qoq lower and just 1.2%yoy – a rate it hovered around throughout 2018.

NZ’s labour market is showing all the signs of a late cycle slowdown, but without rising wages growth. Firms are still finding it difficult to source suitable staff, which has been an impediment to growth for some. And firms are unable, or unwilling, to lift the price tag to attract workers. Something that any economics 101 course would say shouldn’t happen. But with business confidence dented, and fierce competition in parts, wages growth has been left in the doldrums.

Wage growth still not impressing

A tight labour market should be adding to a pick-up in wage inflation – but the evidence here is still not obvious. The RBNZ’s preferred measure of wage inflation, the labour cost index (LCI), recorded an unexpectedly modest 0.3% qoq lift at the start of 2019. This lead annual wage inflation sticking to 2.0%yoy the same rate that was recorded in Q4.

In real terms, wage growth picked up in Q1, given CPI inflation over the same period slowed to 1.5%yoy. This is a positive for consumers, who are also experiencing lower mortgage rates too. However, rising wage growth is also eating into firms’ profitability, and as we have seen from surveys of business confidence, firms remain unwilling or unable to pass on rising costs. This risks future decisions around hiring and investment.

Wages will rise further even if a tight labour market is not doing as much as expected. The Government has kicked things off here. On 1 April the minimum wage jumped $1.20/hr to $17.70/hr and will be captured in June quarter data.

Market Reaction was quick

The market has read the report as soft, and rightly so.

Heading into the data release, the market was precariously priced. The key 2-year swap rate was trading at 1.68%, and was pushed lower to 1.63%. The move was driven by greater expectations of RBNZ rate cuts. Pricing for the RBNZ MPS next week has risen to a 60% chance (up from 50% prior to the report). At 60%, there’s still room for plenty of action on the day, next Wednesday.

The Kiwi dollar has dropped half a cent from ~0.6680 to a low of 0.6629, and has stabilised at 0.6650 at time of writing.

Next week’s RBNZ MPS decision is a big one. With the market roughly 60/40 on the decision to cut, or not to cut. That means the binary outcome will generate a significant move in markets, either way. A cut will see a 10bp fell in rates for the meeting itself, as yields drop meaningfully (10-15bps) out the curve. A decision to hold at 1.75% would equally see a 15bp lift in rates for the May OIS, as yields rise (10-15bps) across the curve. The commentary around the decision will either soften, or exaccerbate the moves in markets. It’s shaping up to be a very eventful RBNZ call. The 2-year swap rate could end next week plus or minus 20bps from 1.63% today (1.43-1.83). That’s a world traders love.

If we’re right, and the RBNZ cut twice by mid-year (June or August), interest rates have at least another 15-25bps to fall. The market will have to imply at least 5-10bps of another cut to 1%.