Key Points

- Another strong labour market report, with the unemployment rate falling to 4.4% - a nine-year low.

- Employment growth was solid, posting a respectable 3.1% yoy lift in line with our forecast.

- However, wage growth surprised a little as shown by the LCI rising only 0.3% qoq – slightly short of the broad market consensus of a 0.4% qoq rise.

- The RBNZ is likely to take comfort in today’s employment figures that it’s meeting one of its two monetary policy mandates, but disappointing wage growth is unlikely to have gone unnoticed.

- We still expect wage growth will pick up over 2018, albeit gradually, due to the tightening labour market, the minimum wage hike, and rising inflation.

- For now, the RBNZ is likely to be patient until its happy inflation is well on its way to the 2% target midpoint before hiking the OCR, in our view around mid-2019.

Summary

NZ’s economy continues to generate jobs to accommodate a growing population, but wages are only inching higher despite a tightening labour market. This has been the story of NZ’s labour market for a while now, a theme that was repeated in the March quarter according to Stats NZ’s suite of labour market surveys (including the Household Labour Force Survey (HLFS), Quarterly Employment Survey (QES), and the Labour Cost Index (LCI)). The unemployment rate eased to 4.4% - a nine year low – slightly below our pick of 4.5%. Importantly, there was a wider sense of labour market strength within the figures with the underutilisation rate (a broader measure of capacity in the labour market) also falling to 11.9%. Employment growth came in at 0.6% in the quarter, on par with the growth in the working age population, taking annual employment growth to 3.1% yoy. However, a fall in the labour force participation rate to 70.8%, still elevated by NZ standards, helped direct the unemployment rate lower. Not all the data presented were a sign of strength, the QES’s measure of total weekly paid hours, a loose proxy for GDP growth, increased a slight 0.1% qoq to take the annual rate down to 2.0% yoy.

Today’s figures showed surprise weakness in wage growth, the private sector LCI came in at 0.3% qoq below the consensus forecast of 0.4% qoq, and kept annual wage growth unchanged at 1.9% yoy. Last year’s Care and Support Workers Pay Equity Settlement continued to prop up annual wage growth, and StatsNZ noted annual wage growth would have come in at 1.6% yoy excluding the pay deal. Today’s labour market report is likely to give the RBNZ comfort that its new employment mandate is being met. However, the paltry 0.3% qoq rise in the LCI still shows that the Bank has work to do on the inflation front. In our view we expect the Bank to keep the OCR unchanged at 1.75% until May next year.

Full-time employment drives jobs growth

In another bright spot in today’s data, the respectable 0.6% qoq rise in employment in the March quarter was driven by a decent rise in full-time employment, which increased by 12,000 or 0.6% qoq. In addition, jobs growth was dominated by employment of women over the quarter. Consistent with GDP growth over much of 2017, the industries that experienced notable growth in jobs at the start of 2018 were centred on services sectors. Business services, retail trade, and public administration industries all experienced significant increases in their headcount in the year to March. Despite the construction sector experiencing a large backlog of work, employment in the sector barely grew over the year to March 2018 (+0.5% yoy). This is a further sign that the construction sector is being held back by a lack of capacity, and is consistent with surveys of business confidence that show difficulty finding staff is a major impediment to growth.

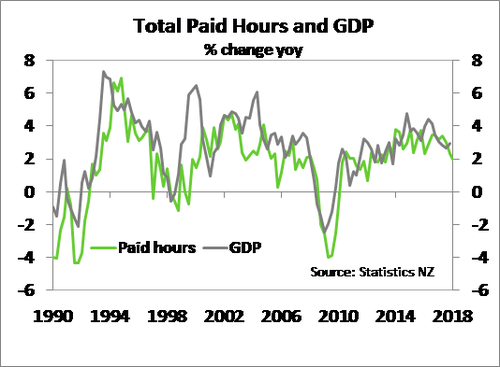

While employment increased in the HLFS, the QES told a different story. For instance, the number of total filled jobs fell 0.2% qoq in Q1, and was only 1.2% yoy higher than a year earlier – the lowest annual increase in six years. As StatsNZ has noted in the past, the two surveys can diverge due to differing coverage (e.g. the QES excludes many agriculture occupations). But there was some additional weakness in the QES with growth in total hours paid by employers falling to 0.1% qoq from 0.4% qoq it the end of 2017. Total weekly paid hours can be seen as a loose proxy for GDP growth and suggests a risk to growth over the March 2018 quarter (see figure below).

Employment growth only kept pace with the rise in NZ’s working age population in the quarter. Nevertheless, the unemployment rate managed to ease a touch to 4.5% helped by a fall in the participation rate to 70.8%. The participation rate is down from the surveys high of 71.1% recorded back in the September quarter, but in a sign that the labour market is drawing people to work, the participation rate remains elevated by historical standards. Reinforcing the fall in the unemployment rate was a 3,000 drop in the number of people captured as unemployed. Further evidence that the labour market is heading in the right direction, the relatively new underutilisation rate also fell and reached 11.9% from 12.2% previously. The underutilisation rate is a broader measure of capacity in the labour market and not only captures those unemployed, but also the underemployed and those people that would work if they could (e.g. currently involved with childcare). This result is likely to further support the idea that the RBNZ is meeting its labour market mandate.

Still a distinct lack of wage growth

The main surprise of today’s labour market report was a fall in wage growth. The private sector LCI, a pure measure of wage inflation, dipped to 0.3% qoq from 0.4% qoq in the December quarter. The LCI had been largely bumbling along at a reading of 0.4% qoq for over two years. The only exception was the September 2017 quarter, which lifted 0.7% qoq, thanks to the Care and Support Workers Pay Equity Settlement. On an annual basis the LCI was 1.9% yoy higher, but would have been around 1.6% without July 2017’ Pay Equity Settlement. While wage growth remains disappointing, household income growth looks fairly robust. The QES measure of average hourly earnings was 3.6% yoy higher, driven by a 4.0% yoy lift in the private sector. In contrast to the LCI, average hourly earnings include increases in wages due to people being promoted or moving to higher paying jobs.

Policy implications

With the RBNZ now explicitly mandated to support “…maximum levels of sustainable employment” the labour market report takes on added importance. However, right now it’s all about inflation, or lack thereof. The current tight labour market that is continuing to generate jobs growth, suggests that the RBNZ is meeting its employment mandate. Today’s labour market figures show we are moving in the right direction. The missing piece of the puzzle is wages growth, however. It is not good enough. And here lies the RBNZ’s stance. Employment growth has been adequate, but inflation has fallen short, particularly wage inflation. Policy settings are loose, but clearly not too loose. The need to unwind loose policy settings is a debate for a much later date. We continue to expect the first RBNZ rate hike to be a 2019 story. For now, easy does it.

Market reaction

The financial market reaction to the report was muted. The flying Kiwi dollar hit some mild turbulence and flattened out quick smart. Interest rates were a little lower, but not a lot. We had a weak session overnight, and that has been reflected into our day. The 2-year swap rate was 2.285%, then it was 2.295%, and now it's 2.275%.