“And the longer I wait, the harder I'm gonna fall…” Ladyhawke

- The risks to the economic outlook may have receded, but they have not evaporated. We take this opportunity to refresh our outlook with rosy hues.

- Politicians are finally trying to make “friends” with lonely central bankers. But so far, Government policy is proving to be little more than an acquaintance.

- Should the coalition step up and deliver more fiscal stimulus in the May budget, we may have seen the low in interest rates. If not, Adrian Orr will do more.

In our June forecast update, we spoke of “Fake plastic trees: the greenshoots of global growth need even more stimulus.” Because “The weight of ageing demographics, fiscal austerity, regulation and populist protectionism overwhelms.” These forces may remain in play for years/decades to come. NZ’s economic growth has cooled below potential, as expected. The Government’s fiscal position is a little worse than expected. And inequitable income growth continues to disappoint. But the outlook is a little brighter. The incoming bank capital regulations are more digestible, and the Government (finally) recognises the part it needs to play in boosting the productive capacity of the economy. Years of underinvestment created a shameful infrastructure deficit, and sapped our potential.

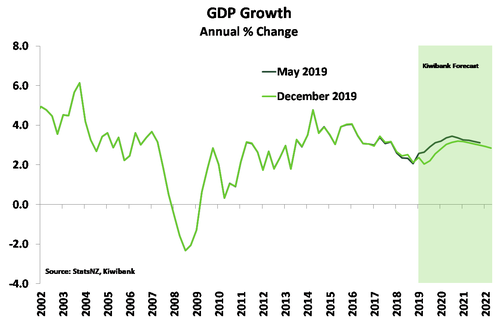

NZ’s inefficient economy has slowed. Growth hit 2.3%yoy to end 2018, down from 3.4%yoy a year earlier. And growth remained at ~2.4% in the year to September 2019. The economy is growing below its potential rate of around 2.75%. Subpar growth is a thorn in the side of the RBNZ, perpetuating the struggle to lift inflation “sustainably” back up to its 2% target midpoint. The good news is business confidence is now improving, the housing market (particularly Auckland’s) is bouncing back, and the global growth outlook has turned positive. We’ve revised our forecasts, by effectively pulling forward the growth we had expected in 2021/22, into early 2021. The fiscal impulse did that.

Central banks around the world remain at the ready to (re)stimulate if required. Here in NZ, the RBNZ cut the OCR to a new all-time low of 1% in August. And the RBNZ remains at the ready to cut below 1%, if required. We expect the RBNZ to deliver another cut to 0.75%, but not until August. Another cut is likely to keep nudging growth and expectations in the right direction. And we believe there’s a 20-30% chance the RBNZ is forced to keep going to 0.50% if conditions deteriorate. The policy action taken to date is likely to support growth, we hope. But one more nudge offers good assurance. Lower interest rates, and no real impact expected from bank capital changes on residential lending, will underpin the undersupplied Kiwi housing market. Confidence is key, and confidence is improving.

Strong and reliable fiscal investment is crucial in supporting confidence throughout the economy. Much of our forecast growth comes from government initiatives. But more investment is needed in the outer years, beyond 2020/21. NZ’s near-record terms-of-trade is cushioning the export sector for now. But slower global growth may lower our export prices in time. The time has come for the fiscal investment era to drive our growth aspirations.

We have taken some comfort in international developments, but we remain sceptical. It would be naïve to think the so-called phase I deal between the US and China is meaningful, and not easily undone. Let’s face it, we’re only one 2am Tweet away from unwinding all hope of a trade deal. And they haven’t dealt with the underlying issues around technology warfare and intellectual property rights. The recent bout of better-than-bad news could easily wane as 2020 matures. The global economy is expected to eke out growth of around 3.5%, far from great. But the most encouraging sign is the lift in fiscal responsibility, as governments face continued populist threats.

We’d want to be more than ‘shovel ready’ during the next downturn. We’d want to be ‘shovel muddy’ and ready for more.

Never dance alone: monetary policy still needs a friend…

“When I'm over all the motion, I'm waiting so we move along”

Optimism is returning to Kiwi firms and households. But we still face headwinds from offshore. If we rewind just a few months, the US-China trade war was intensifying, and global growth forecasts were being repeatedly slashed. Locally, business confidence was drying up, and firms reined in investment and hiring intentions. Policy uncertainty wasn’t helping either. The Government had done its part in scaring business and investors with large minimum wage hikes, and threats of taxes. The RBNZ proposed lift in bank capital added to fear of a credit crunch. And forward indicators pointed to a slowdown into 2020. Just a few months later, heads have lifted, and we have a growth mindset.

A run of positive developments has given us confidence that growth may have troughed in 2019, and will strengthen over 2020. Since May, the RBNZ has delivered 75bps of interest rate cuts – with a notable 50bps delivered in August alone. Record low mortgage rates stimulated the housing market, particularly in Auckland. Although we had forecast the OCR cuts, policy certainty has been delivered too. The RBNZ has delivered less onerous bank capital requirements than initially proposed (see Box B). More recently, the Government announced a $12bn boost in infrastructure spend (see Box A). There is likely to be a lot more fiscal stimulus too. The May 2020 Budget will enable the Government to show their resolve on key issues from infrastructure build, education, housing affordability and well-being. And it’s an election year. The Government has a huge fiscal war chest to deploy, at precisely the right time in history.

A run of positive developments has given us confidence that growth may have troughed in 2019, and will strengthen over 2020. Since May, the RBNZ has delivered 75bps of interest rate cuts – with a notable 50bps delivered in August alone. Record low mortgage rates stimulated the housing market, particularly in Auckland. Although we had forecast the OCR cuts, policy certainty has been delivered too. The RBNZ has delivered less onerous bank capital requirements than initially proposed (see Box B). More recently, the Government announced a $12bn boost in infrastructure spend (see Box A). There is likely to be a lot more fiscal stimulus too. The May 2020 Budget will enable the Government to show their resolve on key issues from infrastructure build, education, housing affordability and well-being. And it’s an election year. The Government has a huge fiscal war chest to deploy, at precisely the right time in history.

Kiwi economic fundamentals are also building behind the scenes. NZ’s terms of trade (Kiwi purchasing power) has hit new highs boosting incomes. The elevated ToT has been driven by export prices, even as global growth and trade slowed. Over the second half of 2019, dairy prices hit a purple patch. The headline dairy price index has gained 8% since June, and the all-important whole milk powder price was up 11%. Fonterra upgraded its forecast dairy payout for the 2019/20 season to $7-$7.60/kgms. If realised, the payout would be at least the fourth highest since the cooperative was forged. Prices for meat have also looked tasty. China has imported all the meat it can. Because an outbreak of the African swine fever has decimated pork supplies.

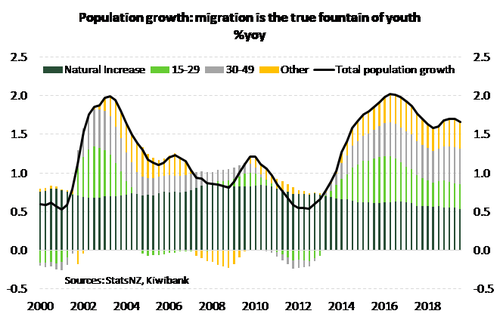

The other strong fundamental has been population growth, which remains well above average. Last year’s census put the resident population at 4.7m in early 2018 – up around half a million people (or 11%!) since 2013. The population surge was not quite as strong as expected. But since then population growth has defied forecasts of a decline and sits at 1.7%yoy, well above the average of 1%yoy. All driven by a rebound in net migration.

The weakness seen earlier in the year, has retracted our starting point. But from early 2020, growth is expected to accelerate, mainly owing to above trend population growth, a high ToT, a strengthening housing market, and policy stimulus. GDP growth is expected to peak at a 3.2% rate by mid-2021, slightly lower than our previous estimate of 3.3%, and due to the lower starting point. Policy stimulus is both monetary and fiscal, finally. The Government’s infrastructure spending should boost activity from the second half of next year. However, there is a question of how much Capex the Government can achieve. There is limited spare capacity, particularly in the construction sector. Any spare capacity should be quickly absorbed next year. The lack of capacity explains the relatively quick peak in forecast growth.

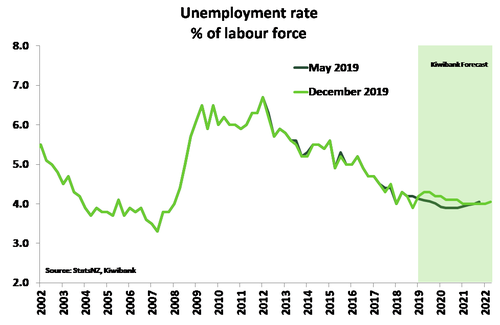

Despite recent headwinds, the labour market remained a granite bedrock. The 4.2% unemployment rate is close to ‘full-employment’. We expect the unemployment rate to hold close to 4.3% before fading gradually over the forecast period. Our new forecast track is slightly worse than previously expected, and we have lowered our wage inflation forecasts as a result.

Despite recent headwinds, the labour market remained a granite bedrock. The 4.2% unemployment rate is close to ‘full-employment’. We expect the unemployment rate to hold close to 4.3% before fading gradually over the forecast period. Our new forecast track is slightly worse than previously expected, and we have lowered our wage inflation forecasts as a result.

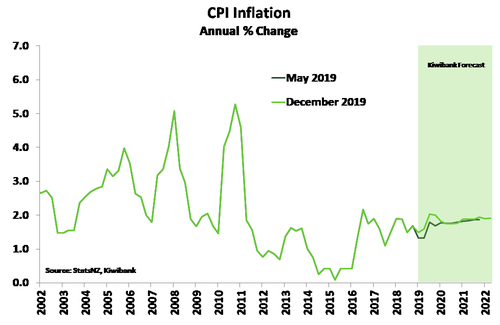

We are forecasting inflation to temporarily lift towards 2% early next year, as the fall in the Kiwi currency lifts tradables or imported inflation. Non-tradable or domestic inflation hit 3.2%yoy in Q3, the highest in almost a decade, but it’s unlikely to be sustained. Inflation has been structurally lower for years – particularly on the tradables side. Inflation has only popped above the RBNZ 2% target midpoint once since 2011. After the temporary spike, inflation will likely pull back from Q3 next year. We forecast only a very gradual return to 2% over the forecast horizon, as non-tradables inflation strengthens from both monetary and fiscal policy stimulus. A strengthening currency is likely to dampen imported inflation. Reflation is the gameplan.

Box A: fiscal stimulus is coming

In the HYEFO, the Government lifted investment intentions by $12bn to address NZ’s shameful infrastructure deficit. But $12bn hardly turns the fiscal dial. Net debt to GDP is forecast to lift to just 21.5% in a few years’ time, before falling back below the budget irresponsibility rules target of 20%. The meaningless target is well below the Government’s capacity to lift debt to tackle an infrastructure deficit. And we have a significant infrastructure deficit. Because successive Governments have underspent at a time of rapidly rising population.

The question is whether the economy has the capacity to absorb additional spending. Slowing economic growth since 2016 has created some spare capacity, but not a significant amount. There are constraints in areas needed to deliver infrastructure, such as construction. So, the task is difficult, but not insurmountable. We must target unemployment rates substantially below guestimates of full employment to unlock idle labour and give the unemployed a second chance. Nevertheless, increased Government investment provides an impulse for growth in the coming years.

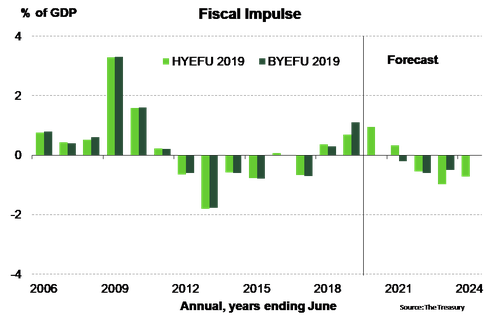

The Treasury’s fiscal impulse analysis indicates that the boost in capital spending, as well as an initial operating deficit, will provide a shot in the arm to growth in the first two years of Treasury’s forecast period (see chart). The more sustained boost to growth than had been previously projected shows Fiscal policy doing its part. We argue fiscal policy should do more, a lot more. After growth in net capital spending peaks in 2020/21, there is a fiscal drag on growth. How unfortunate.

Box B: Bank capital constraints are restrictive, but not as much

"…and will ensure bank owners have a meaningful stake in their businesses" Adrian Orr, RBNZ Governor

The finalised RBNZ capital requirements are less onerous on the banking system. More capital is required by all banks, but the composition and timing are less severe than the original proposal. The proposal has hung over the financial system for a year now, and impacted credit availability. The finalised review gives the industry some certainty and enables banks to construct a game plan. And banks have more time to do so.

The bank capital review will make the financial system safer, no doubt. And the new rules and regulations will improve the competitive environment for banking in NZ. The impact of the review is incredibly difficult to quantify, however. There is a price impact (interest rate) and supply impact (credit availability). The tweaks and changes made to the final review, significantly reduces the likely impact. Estimations of the impact range from the RBNZ’s own 20bps, to bank estimates of 30-to-60bps (down from earlier estimates of 60-to-140bps) on the price and supply of credit). Whatever the (reduced) impact on interest rates, the RBNZ can cut the OCR to offset. And the supply of credit will be monitored and addressed if tightened too far. If the combined impact is just 20bps, then the likelihood of further RBNZ rate cuts has reduced, significantly. Good news for savers.

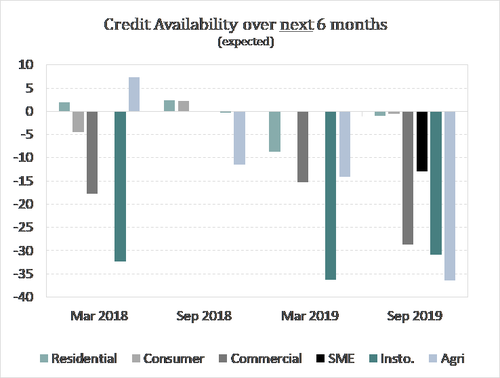

We will watch the RBNZ’s credit conditions survey, which has deteriorated. Credit availability is well below average and contracting in parts (agriculture and commercial). Lending to residential (mortgages) remains relatively unscathed. And we think the supply of residential mortgage lending will remain relatively unscathed. Mortgages have the lowest risk weighting. We expect a slight improvement in the forward-looking aspects of the survey, given the clarity around bank capital requirements.

Credit growth has surprised us on the downside. Credit conditions tightened in the leadup to the RBNZ’s decision on bank capital. And businesses have shown a lack of appetite to invest. Our housing credit growth forecasts are marginally lower over the next few years. However, the stronger and sustained lift in house prices is expected to see stronger housing-related credit growth thereafter. Business lending was particularly weak in 2019 and we have lowered forecasts over the entire period.

Underpinning confidence in consumer spending and SME business (the backbone of Kiwi ingenuity), is the improving outlook for the (Auckland) housing market.

Wild things: rampant house demand needs supply…

“When you're always almost lonely, You forget to take it slowly”

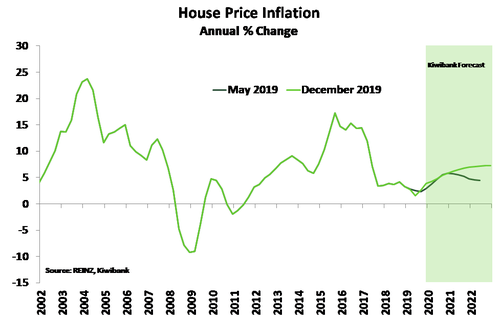

House prices have risen faster than we had expected back in June. National house prices were up 5.6%yoy in November, the strongest rate in 2½ years. Auckland’s housing market is showing signs of life, printing the first annual increase in over a year. Sales activity is lifting, despite a lack of listed property, and the median number of days to sell has steadily fallen in spring.

Our June forecasts assumed a peak rise in national house prices of between 5%-6%yoy by the end of next year – but we’re already there. Our view assumed regional house price gains would slow as prices took their relative place compared to Auckland. But a lack of house listings has seen bold price gains in parts of the country continue. The 20%yoy surge in Whanganui/Manawatū is a prime example. We forecast national house price gains to rise to around 7%yoy in the coming years, and we’ve grown in our conviction. A return to the heady house price gains of 2015/16 are unlikely, however. Several policy changes have weighed on sentiment, and include restrictions on foreign purchases, tightening of the bright-line test, and the closing of the negative gearing tax loophole. In addition, the RBNZ maintains relatively tight LVR restrictions. And affordability is a huge constraint, that can only be met with affordable supply.

Our June forecasts assumed a peak rise in national house prices of between 5%-6%yoy by the end of next year – but we’re already there. Our view assumed regional house price gains would slow as prices took their relative place compared to Auckland. But a lack of house listings has seen bold price gains in parts of the country continue. The 20%yoy surge in Whanganui/Manawatū is a prime example. We forecast national house price gains to rise to around 7%yoy in the coming years, and we’ve grown in our conviction. A return to the heady house price gains of 2015/16 are unlikely, however. Several policy changes have weighed on sentiment, and include restrictions on foreign purchases, tightening of the bright-line test, and the closing of the negative gearing tax loophole. In addition, the RBNZ maintains relatively tight LVR restrictions. And affordability is a huge constraint, that can only be met with affordable supply.

NZ’s housing market has a chronic shortage of affordable dwellings. Over the last few years, we’ve highlighted the undersupply as both a frustration, and support for prices. In August last year we quantified the under supply at 100,000 (see Crystal ball gazing conjures up three P’s of property: Population, Preference, and Policy). Earlier this year, we re-estimated the whopping and worsening shortfall at 130,000 (see NZ’s housing shortage is getting worse, not better). Plenty of work to be done. And we continue to forecast a strong lift in construction.

Anxiety: the downside risks dominate our thinking

“I’ve always been so cautious, But I’m sick of feeling nauseous. It’s not that I am losing, This wall of my own choosing”

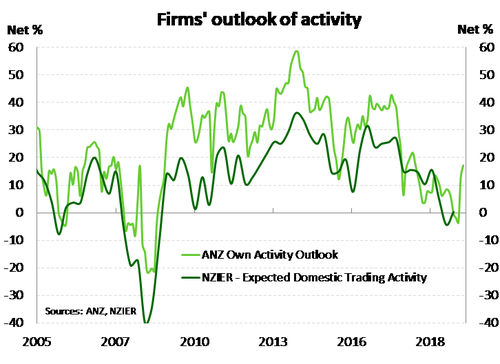

Just a few months back, business confidence was in a funk. The release of both the ANZ Business Outlook survey for September and NZIER’s QSBO for Q3, disappointed. Both surveys were weak, and worsening. Business confidence had been in the doldrums since the 2016 election. Firms were going through labour pains. They complained of tight labour markets, expensive labour prices, and Labour policy uncertainty – especially around capital gains tax. Profitability was being squeezed, and thoughts on minimum wage hikes and greater taxes plagued the minds of many (see A lack of business confidence will cause cuts… And The fall in business confidence is a crushing blow).

It seems the Government has provided a little more policy certainty. But the labour market remains tight in parts. Nevertheless, confidence in the business community has turned, sharply, in just two months. In the latest ANZ business confidence survey, out earlier this week, firms lifted their heads high and start boosting the expectations for their own activity and investment – both key indicators of current and future activity.

It seems the Government has provided a little more policy certainty. But the labour market remains tight in parts. Nevertheless, confidence in the business community has turned, sharply, in just two months. In the latest ANZ business confidence survey, out earlier this week, firms lifted their heads high and start boosting the expectations for their own activity and investment – both key indicators of current and future activity.

The main driver for firms planning to lift investment is “the level of spare capacity, and skilled labour shortages.” One glaringly obvious side-effect of hiking minimum wages (without better education and training to equip workers for the future) is substitution. In a world of accelerated automation, more firms will opt to invest in capital (robots) over low-skilled labour.

Let it roll: markets high on risk

“Too many hard times, too much to think about. So let it roll…”

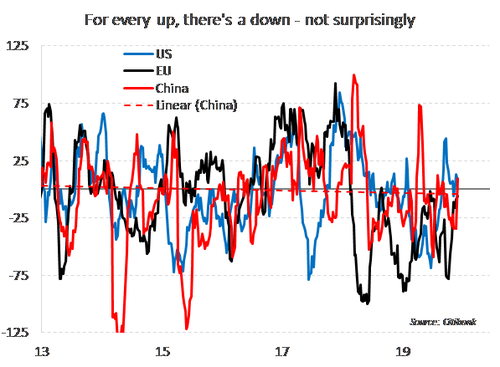

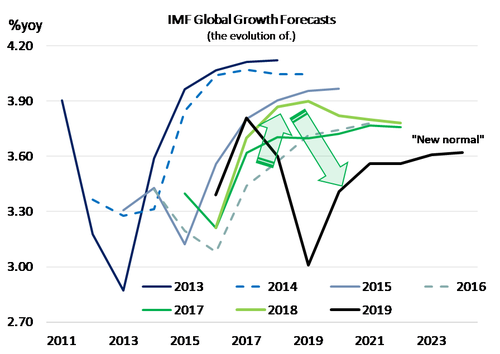

Global financial markets have been boosted by a wave of optimism. 2017 and 2018 were ‘good’ years. The IMF revised their forecasts higher as US growth excelled under the Trumpian sugar rush. And riding on the back of good news, data surprise indices have been climbing higher and higher. Of late, markets have been acting like kids in a candy store, bouncing excitedly when a fresh batch of news is brought out from the backroom.

This positive market sentiment however has been built not on concrete floors but sandy shores, and the foundation is starting to crumble. If anything is certain, it is that for every up there is a down. A reversion to the mean is inevitable and global growth rates already appear to be on a glide path lower. In mid-2019, the IMF made a 180° turn as they revised downward their growth forecasts for the years ahead. And in August, yield curves were inverting – a sign of distress and expected recession.

This positive market sentiment however has been built not on concrete floors but sandy shores, and the foundation is starting to crumble. If anything is certain, it is that for every up there is a down. A reversion to the mean is inevitable and global growth rates already appear to be on a glide path lower. In mid-2019, the IMF made a 180° turn as they revised downward their growth forecasts for the years ahead. And in August, yield curves were inverting – a sign of distress and expected recession.

Our economic potential is being inhibited by a number of factors. One being the tectonic shifts in demographics. Over the last 50 years, we have witnessed not only greater female labour market participation but also a greater tendency for women to remain engaged in the labour market for longer. Running parallel to this is the decline in fertility rates, signalling a delay in motherhood. The unintentional consequence: an ageing population.

The reign of fiscal austerity in the post-crisis world (since 2008) has also severely limited the outlook for growth. Productivity has disappointed due to an underinvestment in infrastructure and education. The unwillingness of governments to loosen the purse strings confuses most. This strange new world we find ourselves in following the GFC grossly resembles “Bizarro world” where the divergence from theory has become the new reality.

Another deterrent to growth has been the current stance of bank capital regulation. The repricing of credit (money was “too cheap” prior to the 2008 crisis) is ongoing. Regulation has impacted the price, by restricting the supply of credit. Lower rates of credit creation have undoubtedly lowered nominal growth. However, talks of a “great global deregulation” in bank capital have grown from bedroom whispers to rooftop shouts, inciting mixed feelings. On the one hand, it threatens recent efforts made to strengthen the international banking system post-crisis. But credit is the oil in the economic engine. And this reversal may be the oil change the world economy needs.

Then there is the rise of the populist protectionist. “Anti-system politics” is a threat to global trade, and a threat not seen since the 1930s. The flag-bearer of populism, aka Trump, is fighting on many fronts. The US-China trade “war” continues without resolution. It is becoming increasingly clear that this is not a war on tariffs, but intellectual property and technology transfer. Ultimately, the war hinges on China’s willingness to commit to structural reform. Mexico, on the other hand, has shown little resilience, quickly succumbing to US trade threats over border protection. We suspect that Trump has unfinished business with Mexico and may even continue to engage other nations that hold a trade surplus to the US.

Over on European soil, the situation is more mixed. While Johnson’s landslide victory has provided us with certainty that Brexit will go ahead, it has unveiled new uncertainty as to what will eventuate come Britain’s exodus. Moreover, the success of Brexit could mean the rise in anti-EU policies within the EU, which would only create more discord in the global economy. As always, uncertainty clouds the growth outlook. For now, the British pound is riding high, but we expect volatile times ahead as negotiations roll on.

Indeed, the prevalence of populism has not stopped there. The year that was saw the Chilean government declare a state of emergency as unrest spread throughout the nation. Mass protests and rallies on issues of inequality, cost of living and privatisation have consequently crippled Latin America’s best credit-rated economy.

Sadly, in today’s international landscape, the grass is not always greener on the other side, with political disruption between Hong Kong and mainland China continuing to escalate. In all this, international waters seem murkier than ever. Naturally, the question arises: How can the Kiwi sailboat navigate its way? One answer: a well-equipped toolbox.

We have a solid trifecta of well-managed government books, a sound financial system and (finally) a fiscal commitment to tackle the gaping infrastructure deficit. Whether this commitment was made in hopes (desperation) to be re-elected or if it stems from a more genuine concern for the economy, is ultimately immaterial – all that matters is that the fiscal dials are turning. And thus, so long as we utilise the dusty Keynesian map, we’ll find ourselves aboard the mighty Emirates Team NZ’s yacht, voyaging (somewhat) smoothly in the new year.

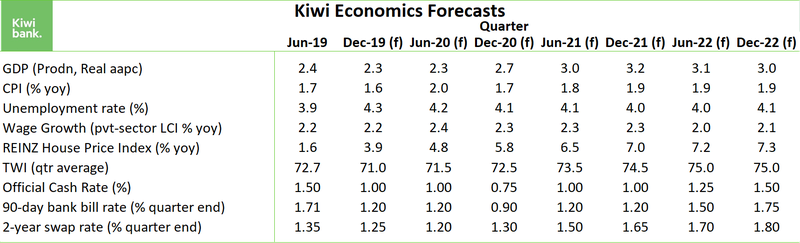

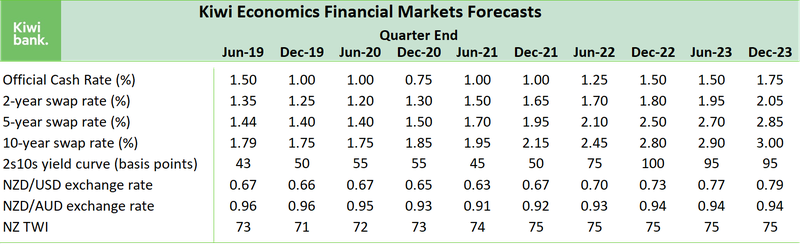

Forecast Tables