“Hey, you're playing with my delirium. And the longer I wait the harder I'm gonna fall” Lady-hawke

“More sooner, is a safer strategy to achieve our targets, than slower for longer… Wake up and go and spend” Orr-dove

- The RBNZ cut the OCR to 1.0%. And we don’t think they will stop there. 50bp moves are normally reserved for emergencies, the last being the Canterbury earthquake. But today, it was a front loading of what was needed.

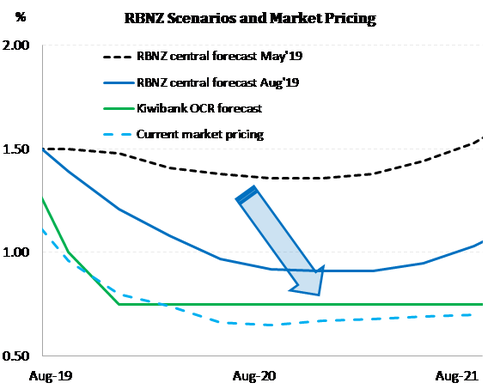

- The RBNZ’s OCR trajectory shows a move to 0.91%. That’s the bank’s way of saying there’s over a 35% chance of another move to 0.75%. We put the probability at 60-70%, in November – 6 months ahead of our previous call.

- The key takeaway for financial markets is interest rates will likely fall even further and hold in an even lower for longer range. And we continue to expect a volatile descent in the Kiwi dollar.

The RBNZ delivered a 50, wow!

There’s heightened uncertainty globally. And “Lower interest rates were clearly needed” Adrian Orr. The RBNZ front-loaded market expectations, and broke the back of the Kiwi dollar with a 50bp thump in the OCR to just 1.0%. 50bp moves are normally reserved for emergencies, the last being the Canterbury earthquake. But today, it was a front loading of what was needed. And there’s at least another cut to come, probably in November.

“Global interest rates are declining, and we’re part of that cyclical behaviour. Global interest rates are at a secular low, so it’s not even cyclical.” Adrian Orr

One key message from the media statement, was “monetary policy is still effective”, although we’d argue with diminishing returns. What that means, is the central bank will keep cutting if growth and inflation continues to disappoint. When asked about fiscal policy, particularly on infrastructure, Orr wisely noted:

“Our fiscal authority is already very proactive… It’s imperative that that money is spent. It’s even greater if it’s spent incredibly wisely on longer term infrastructure… Hurdle rates of return to investment are lower to put in long term infrastructure... It is a fantastic global opportunity to be putting in that longer-term infrastructure.” Adrian Orr

The reaction in financial markets was swift. Kiwi interest rates had fallen substantially leading into the MPS. Because the US Fed had cut interest rates last week, and the RBA was ahead of the RBNZ in cutting to 1.0%. The outsized 50bp move by the RBNZ to 1%, what took the RBA two moves, steamrolled interest rates. Wholesale interest rates are 6-26bps lower across a steeper curve. The ‘Shock and Orr’ statement slapped the Kiwi dollar through 65c without stopping through 64c. Financial conditions are a little easier now.

The reaction in financial markets was swift. Kiwi interest rates had fallen substantially leading into the MPS. Because the US Fed had cut interest rates last week, and the RBA was ahead of the RBNZ in cutting to 1.0%. The outsized 50bp move by the RBNZ to 1%, what took the RBA two moves, steamrolled interest rates. Wholesale interest rates are 6-26bps lower across a steeper curve. The ‘Shock and Orr’ statement slapped the Kiwi dollar through 65c without stopping through 64c. Financial conditions are a little easier now.

The weaker outlook kept the MPC awake from Dusk Till Dawn

Today’s unusually large 50bp cut shows that the committee has become increasingly concerned around the outlook for growth – and hence their employment and inflation targets. They had to act, and act they did! The global backdrop has deteriorated further, with the US-China trade war fuelling investor uncertainty. Adding insult to injury, Europe is looking fragile too. The RBNZ is worried that heightened uncertainty and the weaker global backdrop will weaken export commodity prices, and continue to hamper local spending and investment. We’re just not spending enough. Not firms, not households, and not the Government.

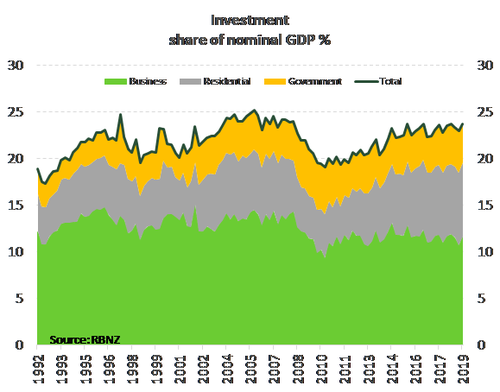

Firms’ investment activity has been weak, backed-up by persistently anaemic investment intentions revealed in business confidence surveys. But this weakness seems structural in nature (see chart below). The Bank presented some more detailed analysis in the Statement around investment, which has disappointed even considering record low interest rates. The RBNZ finds weak investment is partly a confidence game, and partly longer-term structural changes in the economy. The NZ economy has become increasingly dominated by less capital intense service industries.

Households have been more cautious in relation to the housing-related investment, and there is the wealth effect of falling house prices on consumption to consider. The housing market has been subdued for some time following years of excess. But more recently, a period of policy uncertainty and more restrictive conditions for property investors has added to the lull in markets such as Auckland and Queenstown. Policy uncertainty has diminished with a CGT being ruled out as a policy option for the Government. Lower interest rates should also help to simulate activity in the housing market and investment in homes that we need. More needs to be done to alleviate the capacity constraints in delivering much needed infrastructure of course.

Finally, Government spending has been slow to come on stream. Fiscal policy is however expected to support the economy over the coming year. But even Treasury’s fiscal impulse analysis suggests Fiscal surpluses will detract from growth further out. We continue to argue fiscal policy has been too constrained in light of a weaker economic outlook and the current infrastructure deficit. Moreover, the Government has plenmty of fiscal headroom and faces such cheap interest rates (the Government can borrow for 10 years at 1.15%!).

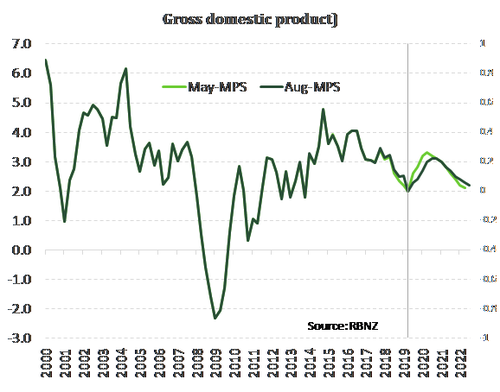

As we have noted, the outlook for NZ growth is looking shakier and growth is expected to remain below trend over the rest of this year. A 50bp cut goes some why to getting economic growth back above trend and ensure inflation returns to the Bank’s 2% target midpoint. The RBNZ revised down their near-term outlook for growth, peaking at a little over 3%yoy by the end of next year.

We now put a move to 0.75% as an 80-90% certainty. Which means the probability of a move to 50bps has grown from our earlier estimate of 20-30%, to 40%. The probability of cuts below 50bps diminish rapidly, in our opinion, but are still possible, as the RBNZ indicated today that cuts would still be effective. In a deteriorating world, the RBNZ would also embark on other courses of action, like QE, QE2, QE3 and some sort of jujitsu move on the yield curve (we miss Richard Fisher quips). The point here is, we have plenty of monetary ammunition if needed. But what we really need is the Government to unleash some of it’s fiscal firepower.

Currencies will attract volatility. The Kiwi flyer (currency) could hold up well in a world muddling through. But the Kiwi will drop like a stone in a disorderly world. Our currency will do what we need it to do, when we need it most. If not, the RBNZ will intervene.

The Kiwi flyer is headed south for the winter

The Kiwi flyer is headed south for the winter

The yield on the 10-year US Treasury bond has fallen from 2.6% in April, to just 1.7% (-90bps). Over the same period, the 10-year Kiwi Government bond yield has fallen from 2.07% to a new record low of just 1.16% (-91bps).

The pivotal point of the Kiwi curve, the 2-year swap rate, has dropped from 1.75% in April to just 1.0% (-75bps). Bank’s use wholesale swap rates to offer fixed-term mortgage rates.

The Kiwi dollar reacted violently to the MPS. The Kiwi dollar had fallen from 0.6790 in July to 0.6488 last week, before stabilising around 0.6530 into the MPS. The ‘Shock and Orr’ statement slapped the Kiwi dollar through 65c without stopping through 64c. The Kiwi hit a low of 0.6378, before stabilising around 64c at time of writing.

We continue to forecast a volatile descent for the Kiwi, to 63c. And we wouldn’t be surprised to see the Kiwi test 60c at some point this year. If the RBNZ continue to 0.75%, then we expect the Kiwi to experience another leg lower to 58c. Threats of recession

If you’re an exporter, these measures are aimed at you.

If you’re an importer, hedging exposures to a declining currency can assist.

The Kiwi/Kangaroo cross is key

The RBA left the cash rate unchanged at a lower 1.0% yesterday. The accompanying statement was cautiously optimistic. And we see the RBA’s decision to hold as just a matter of timing, not direction. The RBA is still likely to cut in coming months, and we expect a move to 50bps by early 2020.

The RBA had to acknowledge that “...it is likely to take longer than earlier expected for inflation to return to 2 per cent.” And the RBA’s final paragraph suggested the central bank may still cut the cash rate in coming months. And we believe they will have to.

“It is reasonable to expect that an extended period of low interest rates will be required in Australia to make progress in reducing unemployment and achieve more assured progress towards the inflation target. The Board will continue to monitor developments in the labour market closely and ease monetary policy further if needed to support sustainable growth in the economy and the achievement of the inflation target over time.” (RBA Aug’19)

Why does a Kiwi bank care about an Aussie central bank? Well, Australia is our second largest trading partner. And our economies face similar global forces. The RBNZ and the RBA now have the same level OCR at 1%. The RBA is dealing with an Australian economy in a worse position. There has been a shock to credit creation, with the Aussie banks tightening the purse strings following the Royal Commission. House prices are still falling, albeit at a slower rate. Household consumption is weakening. Growth has disappointed. And inflation is weaker than expected. The labour market has remained tight, with a low unemployment rate, but the outlook is clouded. Sound familiar? New Zealand also has a tight labour market, but we’re wary of where we may end up this time next year. It’s a global phenomenon.

We expect the RBA to cut to 50bps, and that supports our view the RBNZ will cut to 75bps.

Related articles and content

Property insights – why we think New Zealand’s housing shortage is getting worse, not better.

Fake Plastic Trees – why we think the greenshoots of growth need even more stimulus.

Top 5 reasons behind falling interest rates