Key Points

- Global growth has improved, led by developed nations. Trade wars represent the biggest threat.

- Locally, the Kiwi economy is in a bit of a sweet spot. Growth is close to trend, the fiscal position is strong, and interest rates are low.

- Inflation, particularly foreign inflation, is weak. Wage inflation is the key, and likely to strengthen.

- With Kiwi interest rates expected to stay well below US rates, the Kiwi dollar can provide some support.

Summary

Our forecasts show an economy growing a little above trend into next year. Slightly above trend growth should lead to a slightly faster reduction in spare capacity. The global backdrop is conducive to strengthening price pressure, with solid demand. The missing piece of the economic puzzle, inflation, should be found in time. Once found, the RBNZ will begin to lift interest rates. They will take their foot off the economic accelerator and start normalising policy. So the message is clear, don’t fear rampant inflation or rapidly rising interest rates. But both will rise in coming years. This is good news.

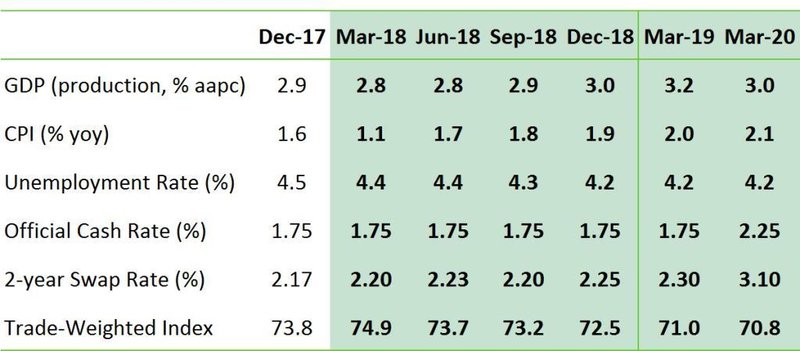

We provide a suite of forecasts out two years. The highlights in the first table, are detailed are in the last table. Economic growth of around 2.9% yoy this year will hopefully be followed by above trend growth of 3.5% yoy early next year. Inflation will strengthen from 1.1%yoy today, to 2.1% yoy this time next year. Stronger headline inflation, along with hikes in the minimum wage rate, will enable a healthy lift in wage inflation to 2.5% by the end of next year. All going well, we expect the RBNZ to be in a position to lift interest rates at the August MPS (we had previously pencilled in May). The Kiwi interest rate curve will move well in advance, and flatten aggressively into RBNZ hikes. The Kiwi dollar is likely to remain on a downward path, until the RBNZ moves to a hawkish bias (early in 2019). The outlook is good, but not yet great. And there are risks.

There are always risks. And most of New Zealand’s risks are foreign. The first is trade protectionism. The rise in protectionist policies post crisis is alarming. Since 2009, the number of trade restrictions has increased every year. Now we face the possibility of a trade scrap between the world’s largest economies, China and the US. Trade wars don’t end well. And New Zealand is now more exposed to an Asian slowdown than ever before. Another risk is the end of the great financial experiment. Central banks around the globe will move, slowly, to unwind some of the most extraordinary monetary policies ever seen. Financial markets are likely to become more volatile, and may react adversely to the draining of stimulus. And then there are the banks. A tightening in financial market conditions may lead to a significant rise in bank funding costs. The Australian Royal Commission may also crimp credit growth on both sides of the Tasman. It depends on how comfortable Kiwi regulators are.

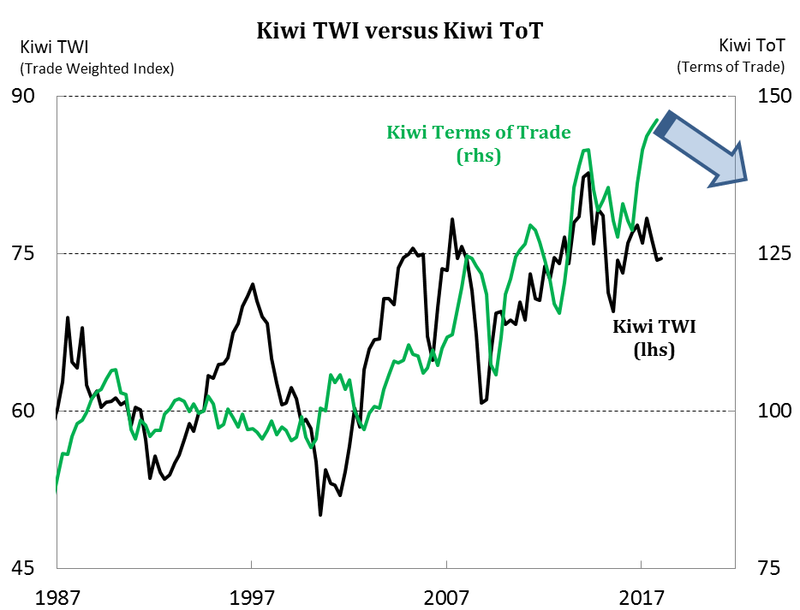

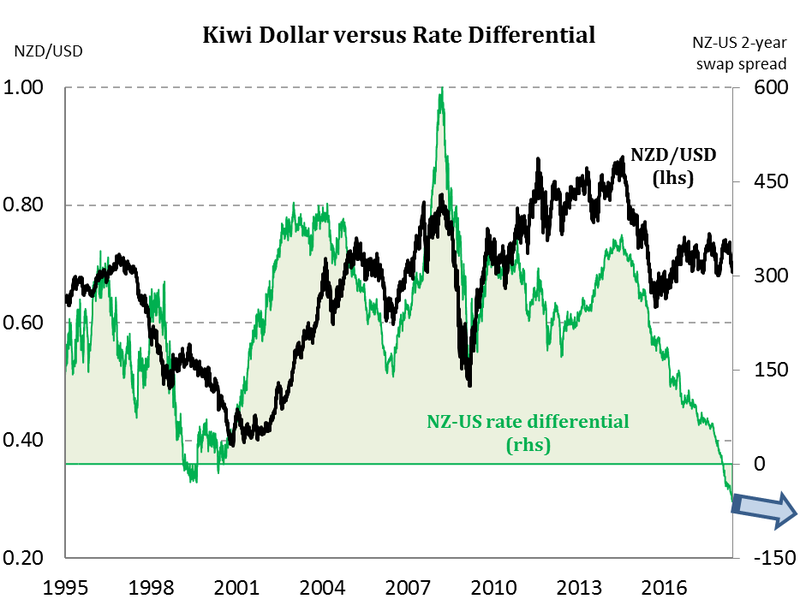

The Kiwi dollar faces divergent forces, but diminishing value

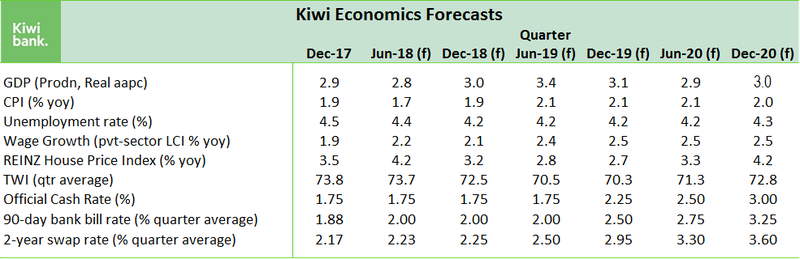

Table 1: Kiwibank’s key economic forecasts

Global developments are net positive, for now

The global economy is still recovering from the crisis of 10 years ago. A financial market crisis takes a lot longer to recover from. And a global financial market crisis takes even longer. The banking crisis of the 1890s was remarkably similar to the great financial crisis of 2008. US unemployment spiked from 4% to 18.4% in 1894, and only returned to 4% in the early 1900s. 11 Australian banks went bust during the 1893 meltdown. It took close to 10 years to recover. There was also a sharp rise in populist political parties as we saw in the 1930s and in the last 5 years. Panics like these take a long time to recover from.

Calls for recessions or seismic slowdowns just because we’re 10-years into this recovery, we believe, are premature. Monetary policy, globally, is still highly accommodative. The US are closer to a neutral setting than any other central bank. But the US Federal Reserve (Fed) are still some way away from “tight” policy settings. And they still have a mammoth balance sheet to unwind. In Europe, we’re still waiting for the ECB to stop printing money, to buy interest rate product, to hold (global) interest rates down. The world is poised for more growth.

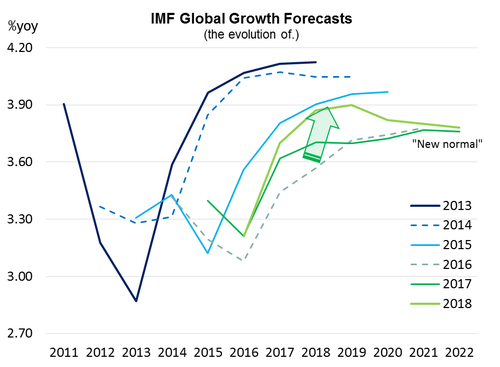

For the first time in a long time, global growth has improved, and led to a lift in expectations. Most of the “surprise” has come from the developed world. From the depths of despair, during the Brexit vote of 2016, developed market growth has risen from the ashes. Strong global growth is a great backdrop for our export sector. And our terms of trade (ToT) has hit record highs. Now, thoughts of Quantitative Easing (QE) 1, 2, 3, 4 and forever, have turned to Quantitative Tightening (QT).

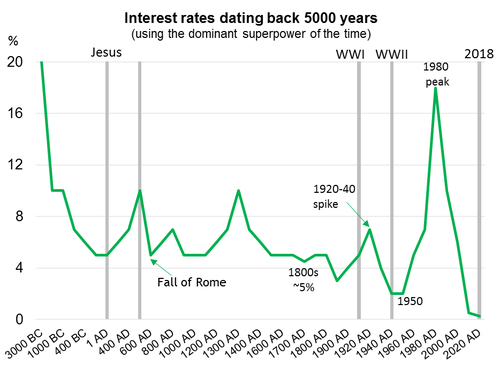

For the first time in a long time, central banks around the world are facing the same direction. They all want to follow the Fed. The great financial crisis led to the great financial experiment, and the advent of negative interest rates. Negative interest rates are a first in the history of mankind, and we have 5,000 years of history. Unwinding the loosest policies ever prescribed will be challenging. The US led us into the great financial crisis, so the Fed will lead us out of the great financial experiment. And the Fed has picked up the pace.

The US is growing at a healthy 2.9% yoy, with strong employment growth, and inflation running just a touch below the 2% yoy target. Trump’s fiscal largesse, with lower taxes and higher spending, has boosted expectations (especially the equity market). Europe has surprised most analysts to print 2.8% growth, well above “potential”. But the EU Bloc has yet to generate much in the way of inflation, with core measures at 1%. The Brexit burdened UK has benefited from a softer currency and is growing at 1.2% with 2.5% inflation. The bounce back from the Brexit vote in 2016 was impressive. A weaker currency helps. Japan has seen a surprising spike in wage inflation; a most unusual development for the demographically challenged nation. China’s growth has cooled to a respectable 6.8%, as officials try to elongate the cycle. China’s growth today contributes the same to global growth as it did many years ago when China’s growth was in the double digits. China is simply much larger today. A little further south, the economy to watch over the next 20 years is India. India is growing at 7.2%, and there are some large transformations taking place. It is a numbers game, and India has more numbers than most. In the next five years India will have more people than China. In 10-15 years, India will be the 3rd largest economy, overtaking Germany and Japan. India will move up our trading partner rankings as well. The good thing about India is, being a former British colony like us, they speak English and have a similar legal system. They also love that game where the Aussies scuff up the ball and bowl it underarm…

To date, economic growth may have improved, but the missing ingredient is still inflation. We believe global prices will eventually lift as the spare capacity that still exists is soaked up by solid demand. The recent rise in oil prices is a double edged sword, however. Rising oil prices are clearly inflationary. Oil prices feed into just about everything. But rising prices can crimp demand, especially when driven by supply shocks (not a lift in demand). We believe oil markets are better supplied, with shale producers in the US profitable at these levels. We will see a spike in Kiwi inflation on the back of the rise in oil prices, but will it be sustained? We think it will.

The rise in US interest rates has enabled the Kiwi dollar to come under some downward pressure. We expect the downward pressure to persist. The Fed’s cash rate is near the RBNZ’s of 1.75% today. The Fed want it at 2.5% in early 2019, and over 3% the following year. The US trajectory is higher than ours. Negative interest reate differentials put downward pressure on our currency, precisely when we need it most. We see the NZD finishing the year around 69-70c. Only a little lower from current levels. But it’s the persistence of the decline that counts. We have a higher tradables inflation trajectory as a result. On that note, let’s speak in native tongue, and cover the Kiwi economy.

The Kiwi economy is going through some growing pains

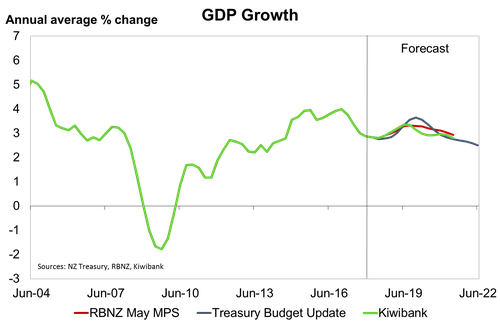

The NZ economy is expected to strengthen over 2018. But constraints on capacity are likely to restrain growth. Economic growth came in at around average (2.5-3.0% yoy) over 2017. The return to average follows a period of rapid growth, led by a boom in construction, buoyant tourist activity, and rapid population growth. Growth was crimped last year as capacity constraints emerged, particularly within construction and tourism. And election uncertainty also weighed on business confidence. The election hangover lingered for longer than we had expected. However, some of the pessimism reflects a historical bias against Labour-led governments in business surveys. Firms’ measures of own activity, a better indicator of GDP growth, have also softened. But the economy should still grow slightly above trend in 2018.

The NZ economy remains supported by some fundamental pillars, including strong population growth – although net migration is starting to ease – stimulatory monetary policy, and a record terms of trade. Toward the end of 2018, fiscal policy is expected to provide a boost to growth. The boost includes previously announced initiatives from the Government’s 100-day plan, such as the Families package (which lifts transfer payments to many and replaces tax cuts proposed by the previous Government). In addition, the operating budgets of many government departments and agencies have been raised. These polices are expected to support household and government spending over the next few years. We anticipate growth will begin to lift later this year to peak around 3.5% yoy over the first half of 2019. Further out, the Government’s Kiwibuild programme (aiming to create 100,000 new affordable homes over the next 10-years) kicks in. While that does help to support growth, lasting capacity constraints and the fact that some housing will be bought off plan, in our view limit the uplift on growth provided by this policy. GDP growth slows back to trend around the end of our forecasts.

The labour market continues to tighten, with the unemployment rate hitting a nine-year low of 4.4% at the beginning of 2018. That is consistent with some measures of full employment, such as the non-accelerating inflation rate of unemployment (NAIRU). Rising GDP growth to 3.5% yoy, should see the labour market tighten further. We forecast the unemployment rate to bottom around 4.2% in the middle of next year. Underlying wage growth should lift as the labour market is stretched. In addition, significant hikes to the minimum wage, aimed at lifting it to $20/hr by April 2021, add between 0.2%-0.5% points to annual wage growth from the June quarter 2018. The rise in wages hinders employment, however, as firms substitute away from labour to capital. If you are going to automate, rising labour costs will accelerate your decision. Slowing growth into 2020 then contributes to a slight rise in the unemployment rate at the end of the forecast period – back to 4.4%. A rise, but it is not a concern.

We expect inflation to head back to the RBNZ’s 2% target midpoint by early 2019, much sooner than the RBNZ (a year later), or Treasury. Part of the lift is driven by stronger tradables inflation, thanks to a weaker Kiwi dollar, and generally stronger global prices (including oil). Since February oil prices have steadily risen to levels last seen almost four years’ ago – WTI lifted back over US$70/barrel in mid-May. More recently the NZ dollar has depreciated as a resurgent US dollar has strengthened against other major currencies. From late 2018 above trend growth also pushes up non-tradables (domestically generated) inflation as capacity constraints become more widespread. The Government’s desire to lift the minimum wage to $20/hr is also expected to add to underlying inflation pressure – the so-called second round impact.

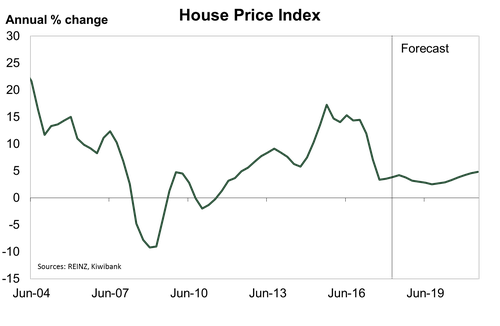

The housing market has recovered from the lows recorded in sales in the middle of last year. House prices nationally are appreciating just shy of 4% yoy, although this is largely the result of the regions playing catch-up to the main centres. Auckland’s market in particular remains muted. There has been growing uncertainty in the investor segment as the Government is gearing up to implement policies targeted at speculators. These policies include the tightening of the bright-line capital gains test on house sale, removing the negative gearing tax loophole and banning foreign ownership of the existing housing stock. These policies, and the uncertainty associated with them, are expected to hamper house price appreciation over much of the forecast period. But we don’t expect a major correction in housing. The housing market in undersupplied and mortgage rates remain low. And unemployment is expected to fall, not rise sharply. Housing corrections are often driven by haemorrhaging households suddenly unemployed or stuck with rampantly rising rates. Neither is expected over the next few years. The jobs market will remain tight. And the RBNZ will keep interest rates relatively low. They will rise, however.

House prices are expected to eventually pick-up. But we certainly don’t expect a return to growth rates seen in recent years. We expect investor restraints, rising interest rates next year, and a steady stream of new supply to restrict house price gains from here.

The monetary policy stance is decisively easy

On the RBNZ’s dual mandate, the economy has generated “an unprecedented increase in employment”, and employment is running close enough to trend. The RBNZ is currently meeting this mandate. On the darker side of the mandate, the inflation outlook is too tepid. RBNZ forecasts show a very slow return to the 2% target mid-point by December 2020. It’s hard to lift interest rates when you don’t see a sustained lift in inflation for over 2 years. They want to be pleasantly surprised first.

In the May MPS, the RBNZ revised down its forecast of inflation, much of it in the near-term, to reflect softer tradables inflation. The revisions to the RB’s CPI track were minor, with inflation expected to rise after hitting a trough of 1.1% yoy in March 2018. In our view, we believe the RB’s inflation outlook is too tepid. We see inflation taking just 9-12 months to return to the 2% midpoint. It is a question of how sticky that return to target proves to be.

Benign underlying inflation is the main focus for the RB. Capacity pressures have yet to feed into underlying inflation. The Bank see’s non-tradables inflation remaining around the current rate of 2.3% yoy until mid-2019 (when the recent fall from the fees-free tertiary education policy drops out) before rising over 3% yoy in 2020.

The RB are at least comfortable with inflation expectations, as they remain anchored to the 2% midpoint. The RBNZ has de-emphasised the impact of inflation expectations on actual inflation. Firms’ price setting behaviour is now more backward looking, and driven more by actual (weak) inflation, rather than expectations of future inflation. Nevertheless one of the risk scenarios presented by the bank is that firms revert to expectations of inflation to guide pricing decisions. The RB’s upside scenario incorporates a familiar lift in global inflation. The risk we all expect, but we have failed to find. Under the upside scenario the RBNZ indicated that it would begin hiking the OCR by the end of 2018, and deliver around 50bps of additional hikes over the projection period. And then there is the downside risk.

The RBNZ’s downside risk is something Kiwi banks are monitoring closely. Financial market conditions have tightened offshore. The spread between rates banks can fund at and cash rates, has widened. To date, the pass-through from US financial markets to Australian financial markets has been clear. Aussie bank funding costs are higher. There are a plethora of forces at work. But Kiwi financial markets have not reacted in a similar manor. It is still a risk. Although we believe it is a diminishing risk.

One of the Achilles’ heels of Australian and New Zealand banking systems is the partial reliance on foreign funding. Developments in foreign funding markets can significantly impact the cost of banking domestically. And it is generally the cheapest source of bank funding. Regulation has forced a reduction in the reliance of foreign funding.

If funding costs blow wider, interest rates offered throughout the economy rise. The spread between the RBNZ’s cash rate and mortgage rates, for example, widen. If persistent, the current monetary policy setting becomes less accommodative. And if that occurs at a time when the economy still needs support, the RB will lower the cash rate to keep settings as they were prior to the blow out. A risk we think will dissipate near term. We will watch with interest.

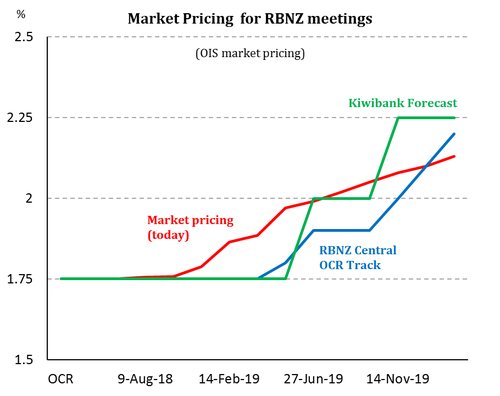

Market pricing (expectations) of RBNZ policy is fair. We expect a slightly more assertive lift in the cash rate from August 2019, compared to the RBNZ. But our expectations are largely matched on the market. What this means is interest rate markets are efficiently priced, and there is unlikely to be dramatic change to mortgage and lending rates over the next 6-9 months. But lending rates will most likely start to lift next year, as the RBNZ comes into play mid-year. Term (fixed) rates will begin to lift first. Because term rates incorporate future pricing of a higher RBNZ cash rate. We forecast the 2-year swap rate to lift from ~2.20% today, to 2.25% by year end (so effectively no change), before lifting more aggressively over 2019 to around 2.95% to end the year. If the RBNZ normalising policy at a gradual pace, the 2-year will continue to rise over 2020 to end the year around 3.5%. 2-year fixed mortgage rates are priced off the 2-year swap rate. We are forecasting a rise in the 2-year rate over the next 2-3 years. Managing interest rate exposure is a discussion we will hopefully have as we head into 2019.

Kiwi Fiscal stance is inherently healthy

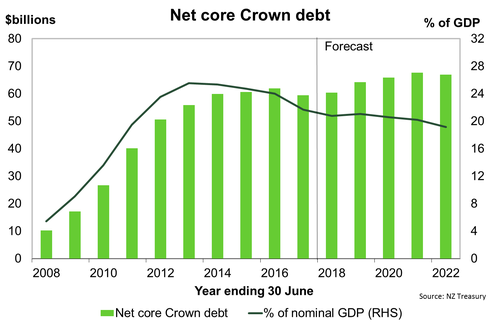

New Zealand’s fiscal position is one of the most enviable in the world. Surpluses are projected to grow over the next five years. Net debt as a percentage of GDP is low to start with, and projected to drop below 20%. It is debatable as to whether Governments need to hit the self-imposed target. But the discipline itself is admirable, and to the liking of rating agencies. The health of the economy, and therefore budget, has enabled a significant boost in spending, with ambitious building plans.

In Budget 2018, tax revenue was forecast to rise by over $23bn over the next five years, $5.7bn above HYEFU forecasts. Tax is higher for three reasons. First, the greater-than-expected tax revenue to date increased the starting point. In the nine months to March revenue was already $1.1bn ahead of the HYEFU forecast. Second, a stronger starting point enables a stronger outlook, and a lift in projected revenues by $3.4bn. Third, tweaks to tax policy on GST (Amazon tax), and the removal of the negative gearing loophole for property investors, boosts the coffers. More money means more spending.

Budget 2018 included an additional $2.8bn of operating spending each year, higher than the $2.6bn in HYEFU. The lift in spending is directed toward key social services, such as health, education and foreign affairs. The Government will fork out $41.8bn on capital expenditure over the next five years – in line with the HYEFU forecast. However, the Government has rejigged its forecast capex numbers and assigned money previously set aside for future budgets to meet urgent priorities. For instance, spending on education infrastructure was lifted by $300mn. Capital spending directed to district health boards was almost tripled to $1.4bn to cover well documented issues with hospitals. Investment in Kiwibuild, to build 100,000 affordable homes in 10 years, remains around $2bn.

The slightly higher cash short-fall, driven by a slightly higher near-term capex, will be funded by a slight increase in debt issuance. Slight changes don’t mean big consequences. The NZDMO will issuance just $1bn more out to 2022. Calls for a cheapening in NZGBs (higher interest rates) would be misplaced. The DMO are adding liquidity to a bond market that has received great demand. NZ bond yields are lower than US bond yields. The idea that NZGBs must include a “liquidity premium” has proven outdated. We may see NZGBs with a “scarcity premium”, as ACGBs once had. New Zealand’s net debt has declined from a peak of 26% to 21% today, and is forecast to fall below the 20% target by 2022. The 20% target is not needed to maintain current ratings. The Government has plenty of room to boost infrastructure spending in future budgets. Rating agencies are more lenient on debt issued to fund infrastructure. Because good infrastructure boosts productivity, and productivity boosts projected revenues.

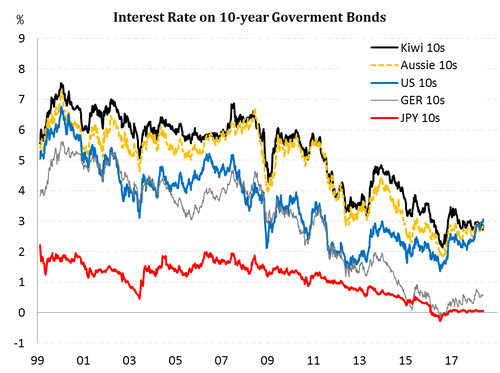

Kiwi rates are really low, and not at risk of revolt

The interest rate on a US 10-year Government bond has risen above Australian and New Zealand Government bonds. We believe it is the first time US rates have remained above antipodean rates for a sustained period of time - there were a few brief blips in 1999-2001.

Why does this matter? Well firstly, economic fundamentals, including demographic trends, influence the level of interest rates above all else. Credit ratings don’t have much influence on the highest of high-grade. Ratings are much more useful in the lower-to-junk credit space. And New Zealand is miles away from low-grade.

Ratings agency Moody’s rates New Zealand as AAA, as good as it gets. S&P rates New Zealand as AA+, pretty much as good as it gets. By comparison the US are rated AA+. They are the global superpower, with the largest bond market, and have arguably the most powerful military in history. If they’re not AAA, well, it doesn’t matter. When the US was downgraded by S&P their bonds rallied, interest rates fell and their currency hardly budged. S&P had fired their bullet. And the US marched on without missing a step. The GFC taught us not to blindly follow others. And we have learned not to outsource our due diligence. The US downgrade is just one example.

Let’s look at the UK, our old mothership. The UK was downgraded following the Brexit vote in 2016, not once, but twice! The UK’s double-notch downgrade took them beneath New Zealand’s rating. UK bonds rallied more than any other on the planet, pushing yields lower. The economic outlook deteriorated, so interest rates fell. So a theoretically far riskier bond, received a much higher price. In theory, UK bonds should have fallen out of bed like Greek bonds. But they’re not Greek bonds, they’re high quality bonds, just not as high quality. So why do we fight tooth and nail to maintain a rating the same as the US and above the UK? We don’t have to.

For international investors, ratings are important and useful. But they’re not the be all and end all. Diversification is more important in a world with a diminishing pool of highly rated assets (A+ and above). New Zealand has ample room to lift debt and expand. So much so, we’re in an enviable position.

Danger zone: there are storm clouds brewing

Ongoing geopolitical risks add to the possibility of a global trade war. The rise of the populist protectionism is worrying, and has been a growing risk long before Trump took the stage. The number and size of protectionist policies has grown every year since 2009. IMF, the World Bank, and many central banks are most nervous about

de-globalisation. And they have warned of the potential consequences to global growth for years. But when we are hurting we look to protect ourselves. The lack of income growth over the last decade has people demanding change (Grexit, Brexit, Frexit, Nexit and Trumpit). We haven’t seen this level of populism since the 1930s. In the 1930s a savage trade war lead to a bloody world war. What we are experiencing today is a far cry from the 1930s. But we have to flag the real risk of rising tensions.

Australia is a tiny open economy somewhere near the edge of the earth. We’re next to them, and even smaller. A global trade war will hurt us directly through our largest trading partner China. A Chinese slowdown will also hurt us indirectly through our second largest trading partner, Australia. Trade war is the modern (nuclear-era) war, and will severely impact Kiwi trade, growth and financial markets. If a trade war does develop, the RBNZ would be forced into action, and slash the OCR in response. But we’re miles away from that today.

Over the weekend some great news developed. Apparently China is addressing US$200bn of the US trade deficit directly. China makes more money out of the US in bilateral trade, hence the US deficit. And China will look to increase imports of US agriculture and energy, to better balance the books. For now, the BuFGs (Big un-Friendly Giants) are playing nice in the global sandpit. Let’s face it, when the US and China start throwing toys at each other, we all get hurt. A truce of sorts may be developing. A truce of sorts will fuel global growth. A truce of sorts will help Kiwi exports. In terms of economic allsorts, that’d be great.

On the upside, stronger-than-expected global growth and inflation may see faster unwinding of accommodative global monetary policy. But the removal of extraordinary stimulus brings extraordinary risks. We’re in the age of regulation, post crisis. And we have never seen such an extraordinary amount of money printing (QE). Quantitative Tightening (QT) is a known unknown. As monetary policy is normalised, central banks will be challenged by haemorrhaging in vigorously regulated financial markets.

Increased volatility in financial markets is likely. The greater the volatility becomes, the slower stimulus will be withdrawn. It is a dynamic path, with continuous feedback. If QT leads to extreme volatility, and/or falling equity markets, QT will be postponed or stopped indefinitely. There is no pre-set course. Central banks have more control than they are given credit for. And central banks have decisively, and effectively, reduced volatility to boost confidence in the recovery. Ultimately, growth and inflation will drive the pace of QT. If QT hurts growth, QT will stop, until growth proves resilient. The risk of QT causing unforeseen volatility is one that may postpone the global recovery, but not end it.

Remember, central banks want reflation. Ex-Fed Chair Ben Bernanke put it best when he said, “One benefit of reflation would be to ease some of the intense pressure on debtors and on the financial system more generally.” Reflation, or inflation or top of solid growth, solves a lot of problems and flatters debt metrics.

New Zealand’s open economy always faces a plethora of foreign risks. We believe the above risks are very possible, but not yet probable. So for all of the Trump talk, taxes have been reduced, spending has been boosted, and a deal may have been struck with China. The EU has outperformed all analyst forecasts. The world is a better place than it was just two years ago. So we have grown in confidence. We are now more comfortable with our positive outlook.

Detailed Forecast Table