- Delta has dented business confidence, but demand looks to have held up. A net 29% of firms still experienced rising activity over the September quarter.

- The current lockdown has thwarted plans to invest and expand business. But hiring intentions have strengthened. A greater share of firms intends to increase headcount in Q4. Because a rebound in demand is expected once the restrictions are eased.

- Cost pressures have eased dramatically in the third quarter, leading to falling pricing intentions. A result at odds with record capacity utilisation and ongoing global supply-chain issues.

The latest Business Opinion survey (QSBO) from NZIER provided more insight into the current delta disruptions. Business confidence took a hit over the September quarter. But importantly, firms outlook for activity and hiring held up well.

Firms’ view of business conditions were down 9 points to a net 8% of firms expecting deteriorating conditions ahead. The fall was nowhere near as sharp as the 37pt plunge seen during last year’s lockdown. Surprisingly, domestic trading activity over the September quarter actually lifted. Businesses have learnt to adapt to life in lockdown. Nevertheless, we’re picking a 7% fall in third quarter GDP. A short, sharp fall from lockdown. More importantly, expected trading activity held up pretty well. A net 9% of firms see expanding activity ahead. The survey suggests once the current disruption ends, economic activity will bounce back. We had tentatively picked an 8.5% rebound in GDP in the December quarter. However, with some form of lockdown, esp. in Auckland, dragging into the fourth quarter our forecast may be somewhat hopeful.

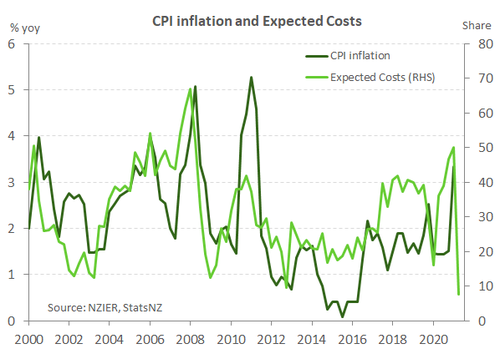

Cost pressures and pricing intentions look to have cooled dramatically in the September quarter. A fall was expected. However, the extent of the fall was shocking, with a net 8% of firms expecting cost increases ahead – a level not seen since 1999. The result contrasts with capacity utilisation, hitting a survey high, and ongoing global supply-chain woes.

The RBNZ is likely to take heart once again from the resilience seen in some key QSBO’s outlook measures. Demand is holding up well to current disruptions. Although this will depend on how covid spreads and future restrictions play out as we aim for high levels of vaccination. Today’s QSBO is unlikely to do anything to dissuade the RBNZ from delivering a 25bp rate hike at tomorrow’s MPR.

Costs soften despite capacity pressures firmly in the redline.

Costs pressures look to have eased in the third quarter. A net 23% of firms experienced rising costs, down a massive 31pts. Lockdown is probably not the most appropriate time to push through price increases on customers or let them know price increases are coming. Only a net 8% of firms see rising costs in the coming months, an unbelievable level not seen since 1999 (see chart below). It’s hard to imagine that such a low share of firms currently expects rising costs. For instance, capacity utilisation hitting a survey high of 96.1%, global supply chain issues continue, and firms report rising fuel and shipping costs. Even last year’s nationwide level-4 lockdown didn’t generate such a vacuum of cost pressure. Perhaps businesses’ landlords have been more understanding in the current lockdown. For now, we are chalking the rapid dive in expected cost pressure down as an anomaly until other data back up this reversal. NZIER notes that the latest QSBO points to easing cost-push inflation pressure, but this is at odds with the international experience.

Costs pressures look to have eased in the third quarter. A net 23% of firms experienced rising costs, down a massive 31pts. Lockdown is probably not the most appropriate time to push through price increases on customers or let them know price increases are coming. Only a net 8% of firms see rising costs in the coming months, an unbelievable level not seen since 1999 (see chart below). It’s hard to imagine that such a low share of firms currently expects rising costs. For instance, capacity utilisation hitting a survey high of 96.1%, global supply chain issues continue, and firms report rising fuel and shipping costs. Even last year’s nationwide level-4 lockdown didn’t generate such a vacuum of cost pressure. Perhaps businesses’ landlords have been more understanding in the current lockdown. For now, we are chalking the rapid dive in expected cost pressure down as an anomaly until other data back up this reversal. NZIER notes that the latest QSBO points to easing cost-push inflation pressure, but this is at odds with the international experience.

Pricing intentions eased too. A net 7% of firms expect to increase prices in the coming months, down from a net 54% in the June quarter. Even the building sector with its acute labour and material shortages, and who noted an increase in pricing in the September quarter, sees a fall in price pressure back to average levels in the coming months.

Investment down, hiring up

The Kiwi economy was on a tear heading into the Delta lockdown. Supercharged economic growth of 2.8% was recorded in the June quarter and the labour market had returned to full employment. Importantly, business investment intentions had strengthened over the quarter. The current lockdown however has thrown a spanner in the works. A greater share of firms are expecting a deterioration in economic conditions over the year ahead. Naturally, such expectations stall any plans to expand business. Now, only a net 13% of firms surveyed intend to increase investment in plant and machinery over year ahead, down from 20%.

There were however pockets of optimism in the QSBO report, especially on the hiring front. Encouragingly, hiring intentions strengthened over the September quarter. While fewer firms increased headcount in the quarter, a net 42% of firms intend to hire in the coming quarter (up from net 22%). As we’ve learnt from previous lockdowns, demand is deferred not destroyed, and economic activity bounces back once the restrictions are lifted. We’ve already seen electronic card spend come of its lockdown lows. Given that a rebound in demand is most pronounced in the retail sector, it’s not surprising to see hiring intentions particularly strong (net 61% of firms). It seems that firms are looking beyond the current disruption and preparing for a surge in activity.

There were however pockets of optimism in the QSBO report, especially on the hiring front. Encouragingly, hiring intentions strengthened over the September quarter. While fewer firms increased headcount in the quarter, a net 42% of firms intend to hire in the coming quarter (up from net 22%). As we’ve learnt from previous lockdowns, demand is deferred not destroyed, and economic activity bounces back once the restrictions are lifted. We’ve already seen electronic card spend come of its lockdown lows. Given that a rebound in demand is most pronounced in the retail sector, it’s not surprising to see hiring intentions particularly strong (net 61% of firms). It seems that firms are looking beyond the current disruption and preparing for a surge in activity.

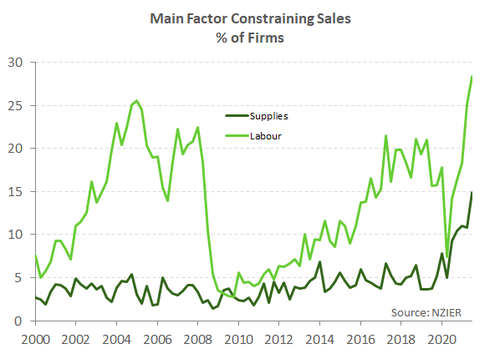

There’s clear demand for employment. But the shortage of skilled labour is becoming even more acute. A record high of a net 72% of firms reported difficulty in finding skilled labour. A shrinking pool of available workers due to the closed border questions whether such demand can be met.