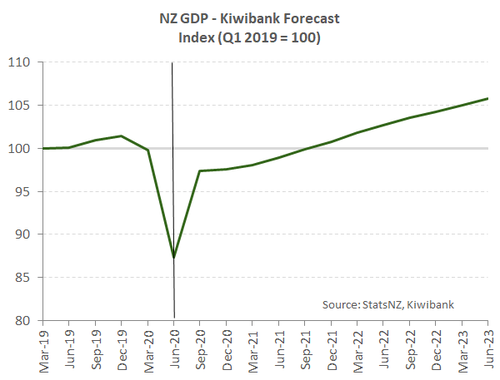

Confirming a v-shaped recovery.

- Unperturbed by Auckland’s level 3 lockdown and an upcoming election, business sentiment rebounds in the third quarter. A net 1% if firms experienced a lift in activity, up almost 40%pts.

- However, it’s easy to get carried away with the sharp rebound in confidence. But NZ’s economy is by no means out of the woods. Policy support such as the wage subsidy is fading, the global covid pandemic is worsening, and closed borders continues to weigh heavily on tourism.

- We still expect the RBNZ to move ahead with a funding for lending programme in November. Followed by a 75bp cut to the OCR early next year.

NZIERs latest business outlook survey showed NZ business has quickly picked up the pieces from the damage caused by April’s nationwide lockdown. The significant policy stimulus delivered to fight the pandemic and NZ’s faster than expected bounce out of lockdown is confirming a v-shaped recovery. After stabilising in the June quarter business confidence lifted and a rise in demand led to a sharp jump in activity. A net 1% of firms experienced an increase in trading activity, up from a net 37% in the June quarter experiencing less activity. In terms of overall confidence, a net 39% of businesses expect a deterioration in general economic conditions in the year ahead – up 19%pts. The move up covid alert-levels in August likely provided a slight drag on the recovery in activity. But the disruption was not a large enough to derail the third quarter rebound.

The latest QSBO surveyed firms ahead of the latest election, so does not reflect NZ business take on the weekend’s Labour party landslide. However, political polls did signal a strong result for the Labour party, and sentiment may reflect the writing that was on the wall. Yesterday we saw a positive reaction to the election in financial markets. And the certainty delivered by a decisive result will likely see a further lift in confidence.

The recovery in demand also flowed through to improvements in both hiring and investment intentions. A net 16% of businesses expect to increase headcount. That’s well up on the 28% of firms planning to shed jobs in the June quarter, but still below the survey average.

The rebound in confidence and key underlying measures is certainly heartening to see. But it is easy to get carried away with the recent run of local data. For instance, the rebound in activity is from a deep hole generated by covid. NZ economic activity is unlikely to return to pre-covid levels for a year or more. The support provided by the Government’s wage subsidy has dried up. The global outlook has deteriorated as a resurgence of covid cases has emerged among some of our key trading partners. And our borders remain closed, and firms reliant on visitor arrivals will likely do it tough over the typically busy summer tourist season. A concern echoed by service sector firms in today’s survey. The services sectors are now the most pessimistic. More policy support ahead is expected. With the RBNZ moving ahead with its funding for lending programme in November. Followed by a meaningful 75bp cut to the cash rate early next year.

Confidence translates to jobs and investment

The recent lift in demand has given firms a boost of confidence. Current conditions have improved, and firms are feeling more upbeat about expanding business. Employment demand has recovered, with more firms looking to increase headcount in the next quarter. And although investment intentions remain weak – net 10% of firms are planning to pare back building investment – this caution is waning. Investment intentions should continue to improve now that we’re on the other side of the election. Stronger demand is also supporting the pricing power of firms, especially those in the retail sector.

Building our way out of covid

Consistent with other surveys of business confidence, the construction sector has had a complete reversal of fortunes. Flipping from being the most pessimistic to the most optimistic industry in Q3. More builders than not indicated rising activity and orders. And the construction sector is supported by a decent pipeline of work. A net 33% of architects reported more government-related construction work over the coming year. That is the highest reading in three years, and chimes with the last election. NZIER noting this as evidence the Government’s planned boost in infrastructure spending is working its way through. Even the pipeline of commercial construction is starting to fill up again. A surprising development given the covid crisis has accelerated trends such as working from home – denting the demand for office space.

The manufacturing industry showed a divergence of fortunes between domestic and export output. Export sales look to have fallen in the third quarter. A net 12% (-2%pts) of manufacturers experienced a fall in exports over the period. A decent rebound is expected in the December quarter. Nevertheless, weaker exports highlight the ongoing damage that is being caused by the pandemic. While NZ has been fortunate to have eliminated community transmission of covid. Cases are rising once again in several of our key trading partners. The global economy is suffering and will likely weigh on the demand for NZ exports.

The manufacturing industry showed a divergence of fortunes between domestic and export output. Export sales look to have fallen in the third quarter. A net 12% (-2%pts) of manufacturers experienced a fall in exports over the period. A decent rebound is expected in the December quarter. Nevertheless, weaker exports highlight the ongoing damage that is being caused by the pandemic. While NZ has been fortunate to have eliminated community transmission of covid. Cases are rising once again in several of our key trading partners. The global economy is suffering and will likely weigh on the demand for NZ exports.

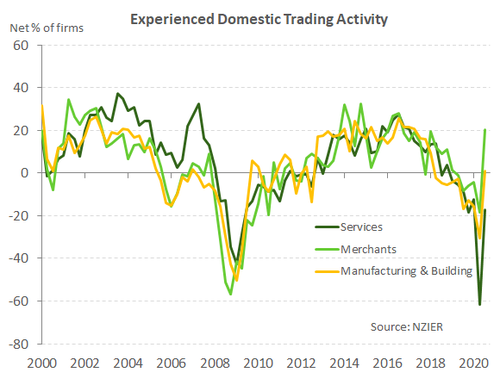

Services is now the most pessimistic industry. A net 17% of service sector firms experienced a contraction in activity up sharply from a net 61%. But the service sector is the only industry that experienced a contraction in activity, and is forecasting less output ahead. Service sector pessimism is hardly surprising. NZ’s closed borders will continue to weigh on firms reliant on foreign visitor arrivals. The upcoming summer tourist season will be a test for the tourism sector with an absence of international visitors.