The NZIER Quarterly Survey of Business Opinion (QSBO) showed firms were a little less downbeat at the end of 2018. But profitability remains a concern.

Key Points

- Firms were less pessimistic at the end of 2018, helped by strengthening demand.

- A lift on trading activity meant that firms were more open to hiring and investing, and growth looks like it will lift through 2019.

- However, weak profitability remains a key concern for businesses, costs are rising but firms are still reluctant to pass them on.

- Today’s QSBO was encouraging for growth as we headed into 2019. But 2019 has started on an ominous note, with heightened concerns on the global economy. We still expect the RBNZ to keep the OCR unchanged this year, before gradually hiking well into 2020.

Summary

Firms were feeling just a little less pessimistic in the final quarter of 2018 than they did in the third quarter according to today’s NZIER’s Quarterly Survey of Business Opinion (QSBO). A net 18% of firms expect a deterioration in general economic conditions. The lift in confidence echoes movements seen in ANZ’s monthly Business Outlook survey. We have seen in recent business confidence surveys somewhat of a protest vote among firms over the uncertainty generated by Government policy. The lift in confidence suggests that firms have a little more certainty from government, with a number of policies now falling into place. On housing of instance, the ban on foreign purchasing of land has come into effect, and Kiwibuild has got off to a slow start.

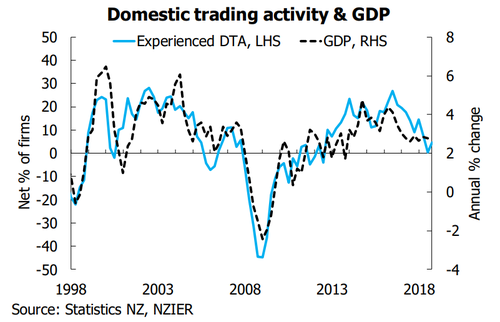

More importantly as an indicator of GDP growth, firms experienced and expected domestic trading activity (DTA) also lifted in the quarter. A net 4% of firms experienced increased demand, up from 0% in the third quarter. This reading is still below the survey average reading of 11% but was a move in the right direction. More encouraging though was a jump in firms’ expectations for domestic trading activity. A net 17% of businesses see a lift in DTA at the beginning of 2019. That is now back above the survey average reading of 15% and shows an encouraging sign that growth will strengthen over 2019 as we expect. NZIER noted experienced DTA in the December quarter was consistent with GDP growth of 2% yoy (see chart below). This feels too weak in our view and we would see growth remaining around trend at the end of 2018 before lifting as we move through 2019.

We didn’t write the economy off when pessimism among firms hit a nadir back in the September quarter. Yes, risks to economic growth were elevated, but this seemed to be driven by displeasure toward government policy rather than more fundamental weakness. Based on today’s QSBO results our view was justified. However, an acceleration in growth this year is far from guaranteed. The world has entered 2019 with somewhat chaotic financial markets. China’s economy is looking a bit shakier, not helped by ongoing trade dispute with the US. In the US a partial shutdown of the Federal Government is starting to weigh on growth and concern markets. At home, the RBNZ is looking to banks to raise their capital levels. This will make the banking sector more resilient to an economic shock but is likely to constrain credit growth and potentially growth at the same time.

On the inflation front, today’s QSBO showed that cost pressures continue to build. But there remains a lack of enthusiasm among firms to pass this on to customers. In our view, rising cost pressures will feed into underlying measures of inflation.

Businesses are back in a mood to hire and invest

The lift in actual and expected demand in the final quarter of 2018 translated into a lift in both hiring and investment intentions. An increased share of firms is looking to invest in plant and machinery, but there is less desire to invest in building, particularly commercial buildings. This is a part of the building industry that has faced well publicised difficulties of late. It appears that hiring was stronger in Q4, with a net 5% of firms adding to headcount. Firms are still looking to increase staff numbers in the coming quarter too. It’s still hard to find suitable labour however. A net 53% of businesses found it difficult to source skilled workers – that was up from a net 44% in the previous quarter and the highest reading since early 2005.

Weak profitability remains a concern for businesses

Still a major concern for firms is profitability. A net 22% of firms experienced a deterioration in profitability in the December quarter, this is despite the pickup in demand at the end of 2018. If this continues, it could threaten future employment and investment activity. One thing weighting on profitability is rising costs. Cost pressures are still evident and there was a net 48% if firms reporting rising costs – we haven’t seen a reading this high in over a decade. We know labour costs are becoming more expensive, which is likely to continue. As mentioned above, it is becoming increasingly difficult to find staff, firms will have to pay up to get workers. In addition, the Government announced just before Christmas that the minimum wage will jump $1.20/hr from 1 April to $17.70/hr as the Government reaches for their target of a $20.hr minimum wage by April 2021.

The regions are more buoyant than Auckland

As we found in our regional economic note last year, there is a divergence in fortunes between Auckland and the regions. Today, NZIER noted that businesses in Nelson and Wellington were the most upbeat, while Auckland experienced a deterioration in confidence. And it is also Auckland where labour shortages continue to hold the super city back. Auckland is also a major manufacturing hub, and manufacturing was also the most pessimistic industry in the fourth quarter. This divergence is more of a story of catch-up in the regions – a development that played out in the housing market throughout 2018. In contrast. Auckland is experiencing the discomfort of past rapid population growth, that it’s still scrambling to accommodate.