Image source: Henry Hustava

Key points

- As expected, the RBNZ cut the cash rate to 1.5%. And we don’t think they will stop there.

- The RBNZ’s OCR trajectory shows a move to 1.36%. That’s the bank’s way of saying there’s over a 50% chance of another move to 1.25%.

- The RBNZ will monitor how much of the 25bp cut is passed onto borrowers and savers. If not all of the 25bps are passed on, the chance of another cut increases.

- The key takeaway for financial markets is interest rates will likely fall further and hold in an even lower for longer range. And we continue to expect a volatile descent in the Kiwi dollar.

The RBNZ delivered

As we expected, the RBNZ delivered a 25bp cut in the OCR to 1.5%. We had first flagged the move in March, immediately following the RBNZ’s OCR statement. See Blood, Sugar, Brex-Magik: markets high on risk. We don’t believe the RBNZ is finished either. Once the dust settles, the amount of the flow through to mortgagees and savers will be important. So too will be the reaction in financial markets.

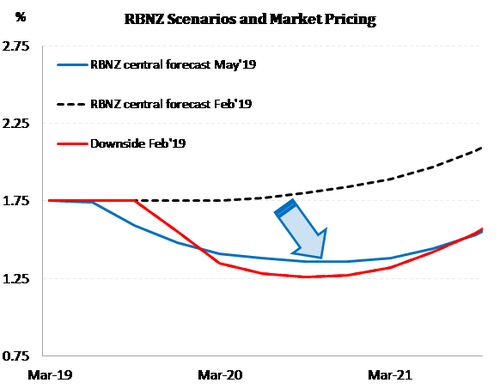

The RBNZ has moved down the “downside” trajectory delivered in the February MPS, see our first chart. Unfortunately, the RBNZ has not delivered risk scenarios around the central trajectory today. The lack of scenarios has limited to markets ability to price future perceived risks.

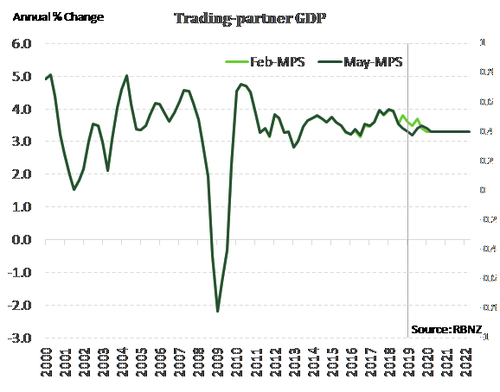

The justification for the Bank’s move is in their forecasts. The fall in GDP growth has fallen faster than was anticipated only six weeks ago at Feb-MPS. Today’s cut, along with a big pick-up in government spending (perhaps hopeful) is expected to contribute to a higher peak in growth well above NZ’s potential mid-next year. This is expected to see inflation only slowly return to the 2% target midpoint by mid-2021 around 6-months later than the Feb-MPS.

The reaction in financial markets was swift. Kiwi interest rates had lifted a little leading into today’s announcement. Because the RBA held their cash rate yesterday, muddying the outlook for the RBNZ today. Those short positions in rates were immediately flushed out with the RBNZ’s decision to cut. The pivotal point of the Kiwi curve, the 2-year swap rate, dropped from 1.64% to 1.55% (-9bps). Bank’s use these wholesale rates to offer fixed-term mortgage rates. Competition for fixed rate mortgages is likely to heat up following today’s cut.

The Kiwi dollar has fallen, but not that far. The Kiwi dropped to $0.6527 after the announcement, from $0.6608, but has rebounded to $0.6576 at time of writing.

Cut needed to lift GDP growth and get inflation back on target

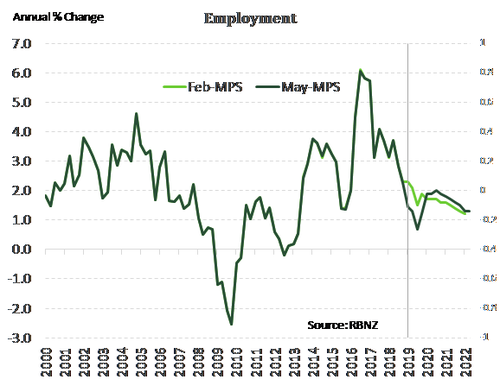

The justification for the Bank’s move is found in their forecasts. GDP growth, inflation and employment growth have all fallen faster than was anticipated only six weeks ago at the Feb-MPS. This has raised the stakes for the RBNZ, with increased risks that the Bank will miss its target on the downside. Inflation is below the 2% target mid-point, and has been there for years, local firms remain downbeat and the global outlook has generally deteriorated since the start of the year (see chart below).

Something was needed. Today’s cut is expected to support spending in the economy and contribute to a higher peak in growth well above NZ’s potential mid-next year – peaking at 3.3%yoy. As the members discussed during the meeting: “The members acknowledged the importance of additional spending from households, businesses, and the government, to meet their inflation and employment targets.” Will only one cut lift domestic spending in any meaningful way? Probably not. As noted above we strongly believe that more stimulus will be needed for the RBNZ to realise these forecasts – one cut will barely touch the sides.

Something was needed. Today’s cut is expected to support spending in the economy and contribute to a higher peak in growth well above NZ’s potential mid-next year – peaking at 3.3%yoy. As the members discussed during the meeting: “The members acknowledged the importance of additional spending from households, businesses, and the government, to meet their inflation and employment targets.” Will only one cut lift domestic spending in any meaningful way? Probably not. As noted above we strongly believe that more stimulus will be needed for the RBNZ to realise these forecasts – one cut will barely touch the sides.

Also, the bank is hoping fiscal policy to play a big part here. To date, fiscal stimulus has been patchy and may continue to be. Transfer payments associated with the Government’s Families Package have supported consumer spending. But government investment has been hampered in part by a capacity constrained construction sector – and a self-imposed fiscal straight jacket. We’ll have a clearer idea of additional fiscal stimulus at the end of the month with the Government’s Budget on 30 May.

The slowdown seen in GDP growth from late 2018 is forecast to see employment growth continue to slow from the surprisingly weak March quarter outturn. The MPC has judged that a cut was in part needed to ensure maintenance of its maximum sustainable employment objective.

During the press conference, the Governor fielded a number of questions around diminishing returns to cutting from here, and alternative measures.

We’d put a 40% chance of move in the OCR to 0.75% in 2020, if conditions worsen, materially from here. Beyond there, the RBNZ could cut to 50bps, and would entertain the use of QE, currency intervention, and firing up Government investment. The RBNZ’s QE could buy Govt bonds with the understanding the Govt ramps up fiscal investment. And the RB can easily print and sell the currency. But we’re still quite some way away from entertaining QE. The point here is, we have plenty of ammunition if needed.

Currencies will attract volatility. The Kiwi flyer (currency) could hold up well in a world muddling through. But the Kiwi will drop like a stone in a disorderly world. Our currency will do what we need it to do, when we need it most. If not, the RBNZ will intervene.

We forecast a volatile descent for the bird this year. The Kiwi should drop into the low 60s by year end. RBNZ rate cuts will accelerate the Kiwi’s decline. At 66c today, the risk is asymmetrically lower, in our opinion. Threats of recession offshore, could see the bird drop into the 50s.

The Kiwi/Kangaroo cross is key

The RBA left the cash rate unchanged yesterday. The accompanying statement was more dovish. And we see the RBA’s decision to hold as just a matter of timing, not direction. The RBA is still likely to cut in coming months, after the Australian Election.

The RBA had to acknowledge the “noticeably lower than expected” inflation. And the RBA’s final paragraph suggested the central bank may still cut the cash rate in coming months.

“The Board judged that it was appropriate to hold the stance of policy unchanged at this meeting. In doing so, it recognised that there was still spare capacity in the economy and that a further improvement in the labour market was likely to be needed for inflation to be consistent with the target. Given this assessment, the Board will be paying close attention to developments in the labour market at its upcoming meetings.” (RBA May’19)

Why does a Kiwi bank care about an Aussie central bank? Well, Australia is our second largest trading partner. And our economies face similar global forces. The RBA is dealing with an Australian economy in a worse position. There has been a shock to credit creation, with the Aussie banks tightening the purse strings following the Royal Commission. House prices are falling. Household consumption is weakening. Growth has disappointed. And inflation is weaker than expected. The labour market has remained tight, with a low unemployment rate, but wages growth remains subdued. Sound familiar? New Zealand also has a tight labour market, but weak wages growth. It’s a global phenomenon.

Australia and New Zealand are very similar, but different. Australians support the canary yellow jersey, we support the black jersey. We bowl overarm, they bowl underarm. But we do tend to move together with the global economic cycle. And the outlook for global demand has deteriorated. We’re both commodity producers. Australia is known has a “hard” commodity nation, exporting shiny stuff like iron ore, coal, gold, silver, pink diamonds and hard rock like AC/DC. Australia will soon become the largest exporter of LNG also. Whereas New Zealand is a “soft” commodity nation, exporting agricultural product and soft rock like Crowded House. Although we do produce the hardest commodity known to mankind, the All Black jersey. But much of our manufactured exports go to Australia. If Australia’s economy is weakening, then there is likely to be a slowdown in demand. Support via a weaker Kiwi dollar will help.

The Kiwi/Aussie currency cross is important to our exporters. The RBA’s decision to hold the cash rate has allowed the NZD/AUD currency cross to fall from ~$0.9440 to $0.9400. The RBNZ’s decision today was perfect in timing. The NZD/AUD cross has fallen to $0.9380. That’s good for Kiwi exporters.

The Kiwi flyer is headed south for the winter

The Kiwi flyer is headed south for the winter

We continue to call a volatile decline in the Kiwi. This time last year, when the NZD was around 75c, we called a decline to 67c, and we’re there. See “What drives the most beautifully volatile currency in the developed world?” We updated our view in August last year to 63c in 2019, and we’ll get there. See “Bye not Buy Birdie: the Kiwi dollar is on the endangered currency list…”

Last month, we continued to highlight the likely move in the bird into the lows 60s. See Blood, Sugar, Brex-Magik: markets high on risk. Our call on the currency has been consistently lower. And we expect further declines. The trajectory is important for importers (goods getting more expensive) and exporters (your goods getting cheaper) alike.

Let’s say the RBNZ cuts another 25bps to 1.25%, and leaves the door open to more if required. Then the flying Kiwi descents, and should end the year close to 60c.

If you’re an exporter, stop smiling, it hasn’t happened yet.

If you’re an importer, hedging exposures to a declining currency can assist.

The Kiwi dollar is on a glidepath

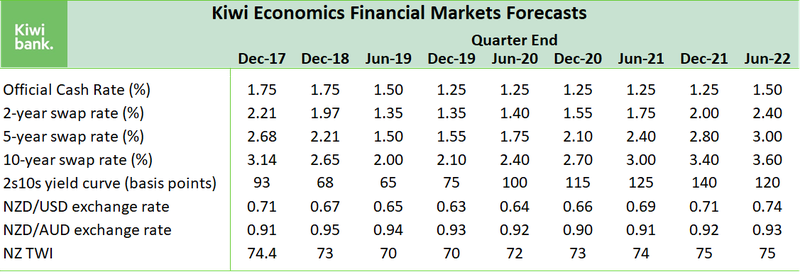

Table 1: Kiwibank’s key financial market forecasts