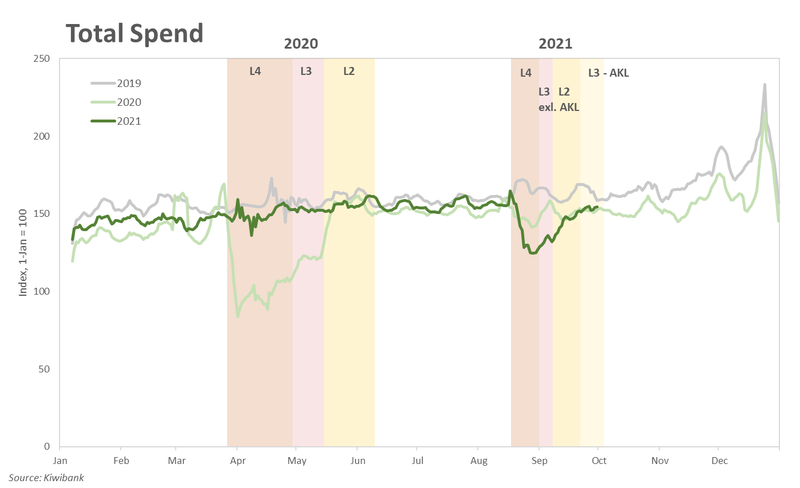

Spending slow to start up

The month of August captured the 2-week nationwide lockdown. Total Kiwibank credit and debit card spend was down almost 8% in the month. Spend picked up in September as restrictions outside of Auckland were gradually relaxed. Contactless service saw a 1.8% rebound in spending on goods. Services spend however is still down 5% in the month, albeit an improvement from the 15% drop in August.

Overall, Kiwibank electronic card spend fell 1.6% in the September quarter. That compares to the 16% rise in spend in the June “lockdown” quarter last year. There are a number of reasons why spend dropped this time around:

- Spending activity has only partially recovered. Because many restrictions remain in place, particularly within Auckland. The June 2020 quarter however not only captured the lockdown but also the move to Level 1 and the rebound in spend.

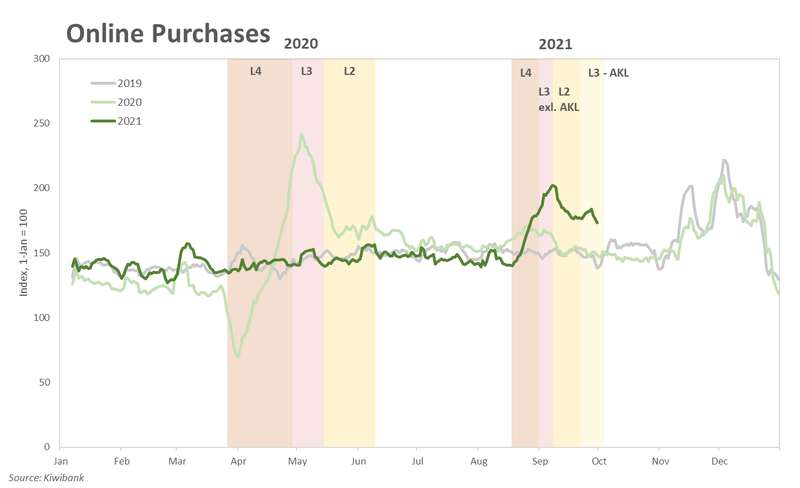

- The drop in spend last year was much deeper. The nationwide 2020 lockdown was considerably longer, totalling 33 days and leading to a 20% monthly drop in spend in April. Starting from a lower base, the subsequent spending spree saw spend rise in the quarter overall. In contrast, online purchases during the 2021 lockdown surged which supported total spending. Households learnt that they need not wait until stores reopen to continue spending. And many businesses were better equipped this time around, having bolstered their online presence over the past 18 months.

- The 2020 spending spree was also much stronger than the current rebound in activity. Sending spiked by 14% in the first week at Level 3 last year. Given the more staggered easing of restrictions this time, spending has been slowly grinding higher. Spending rose 4.3% when the regions outside of Auckland moved to Level 3. Once Auckland sailed out of lockdown, spending was given another kick higher, rising 7% in the first 5 days at Level 3. The rebound is looking less like last year’s Red bull-powered hill sprint, and more like a herbal tea inspired jog uphill.

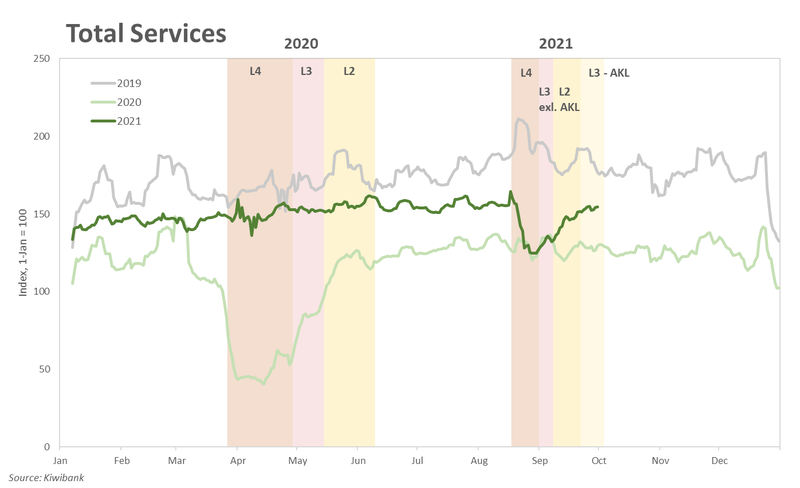

A slow ascent in services spend

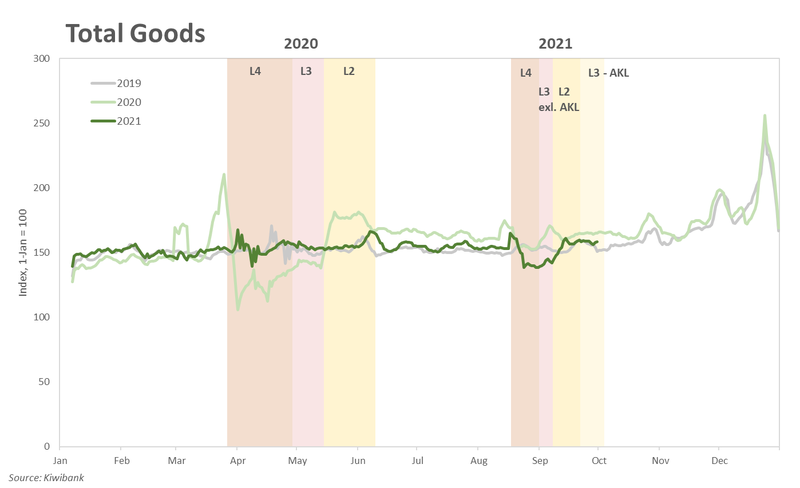

Spend on retail goods was well supported by online shopping throughout the lockdown period. But inflation may also be working behind the scenes here. The September quarter inflation print is expected to be yet another strong one, with the annual rate likely to shoot above 4%. Firms are facing rising costs due to capacity constraints and global supply chain disruptions. The shallower drop in spend may in part be due to higher consumer prices, especially for durable goods.

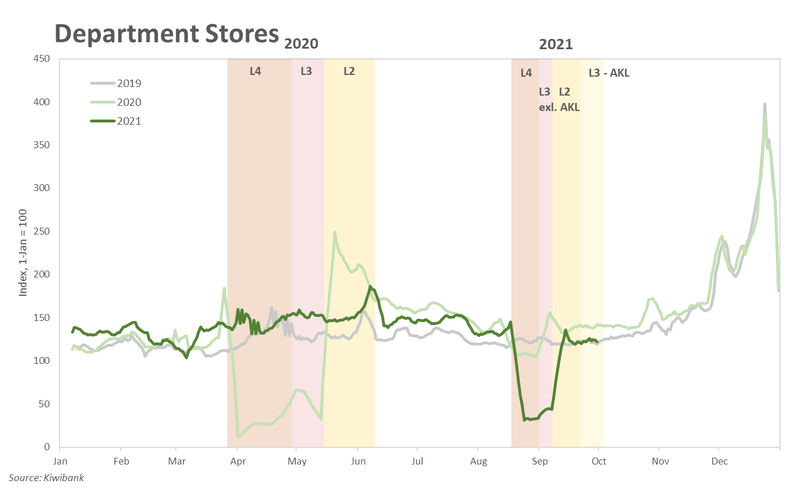

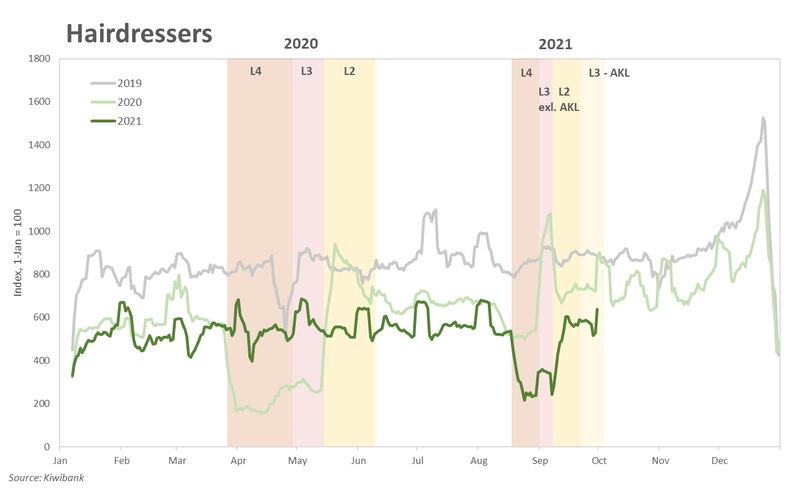

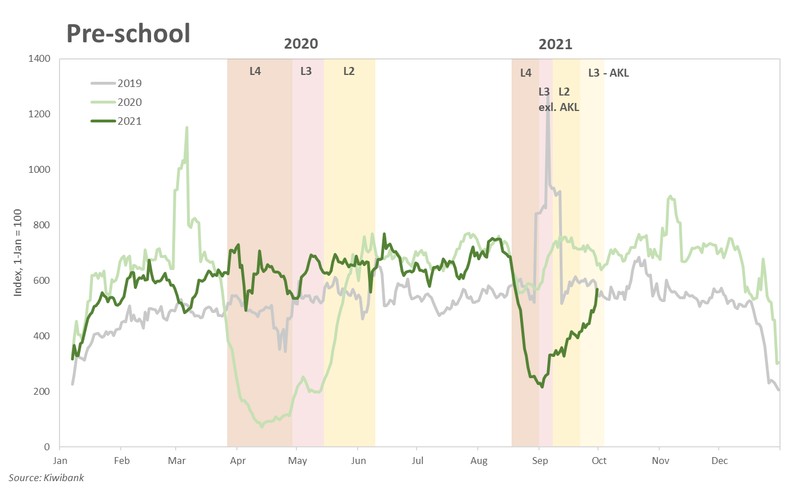

Retail service spend however is showing a slower ascent from the lockdown lows. A recovery in retail requires more lenient restrictions. Spend on services recorded a meaningful lift once contactless service was allowed. But many retailers are still unable to open due to the limitations on people gatherings. Close-contact service also remains closed off. And Auckland is still stuck at Level 3. Retail service spend has been on the rise but is yet to return to pre-lockdown levels. For many in the services sector, Level 4 certainly is the “feels like” temperature in the current business climate.

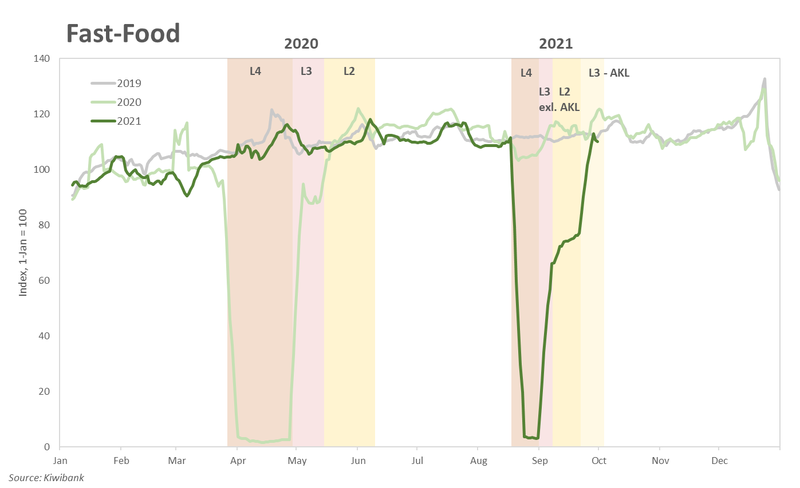

“I'm lovin’ it”

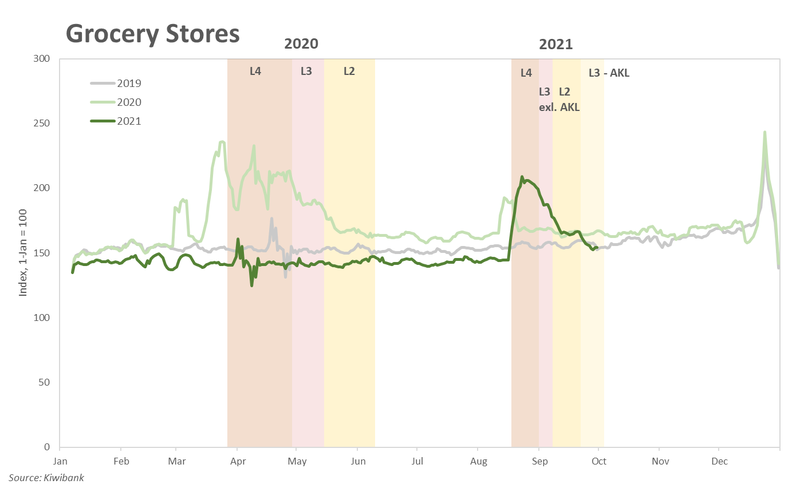

The drop to Level 3 saw an immediate bounce back in quick-service restaurant and café spend. And once Auckland moved to Level 3, fast-food spend was given another leg up. At the same time, spend at grocery stores fell and has since returned to pre-lockdown levels.

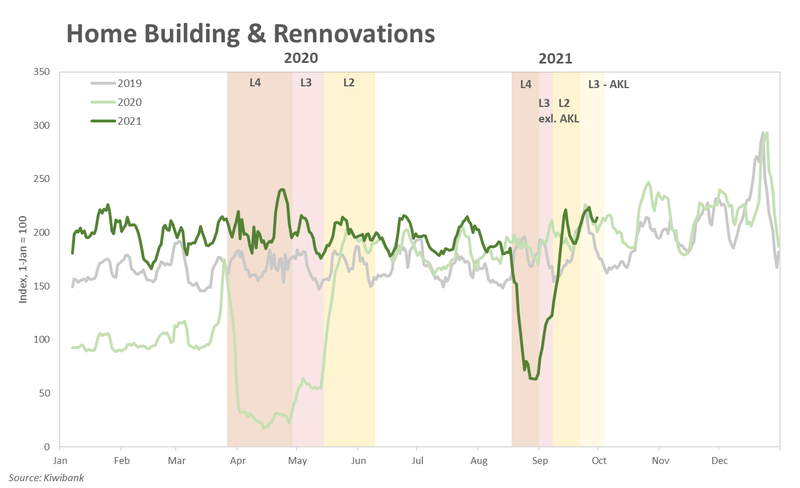

But Level 3 isn’t just ‘Level 4 with takeaways’ but ‘Level 4 with takeaways and Mitre 10’. It wasn’t just under the Golden Arches where queues of cars were spilling onto the streets, but also at hardware stores. The option to click and collect saw many, from tradies to DIYers flock to their local hardware store, waiting bumper-to-bumper.

Sharing the load

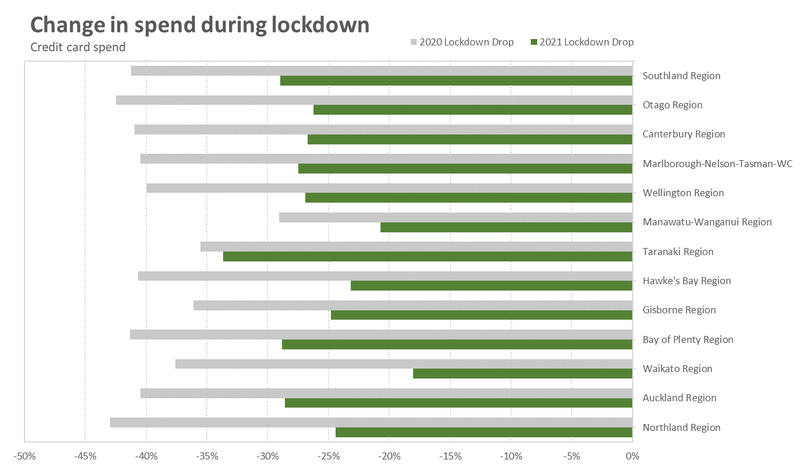

Similar to the overall trend, spend at the regional level recorded a shallower drop than seen in the 2020 lockdown. And once the lockdown was lifted outside of Auckland, the volume of spend in the regions rose. Excluding Auckland, the regions accounted for 67.6% of the total volume of spend in the first 5 days of Level 3, up from 62.8% in the last week of lockdown (Auckland’s share fell to 32.4%).

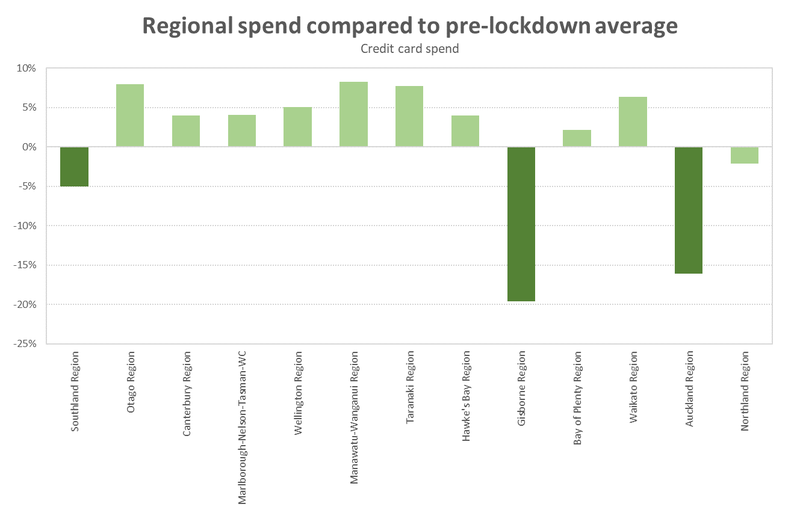

The move to more lenient restrictions however has allowed spend to recover in most regions. Spend levels for many regions have jumped to above pre-Delta lockdown levels. However, restrictions remain in Auckland, and credit card spend is yet to recover.

From Just in Time to Just in Case

Stuck in transit

The roll-out of the wage subsidy scheme has quelled fears around job security, supporting household confidence and in turn consumption. Online spend surged during the lockdown, and there are signs that the rebound in overall spend is taking shape. There’s clearly no lack of demand in the economy. But the ongoing disruptions to global supply chains questions whether there is sufficient supply to meet demand. The struggle to get hold of stock has been well documented. With NZ sitting at the edge of the earth, shipping routes are being severed. Several media report international shipping companies abandoning the relatively remote and marginal trans-Tasman routes in favour of profitable routes between China, Europe and the US. Anecdotally, we’ve heard of retailers limiting their stock to just a handful of brands, and holding onto more inventory than usual. The business model has shifted form Just in Time to Just in Case. So don’t be surprised if you get the same Christmas presents as everyone else this year.

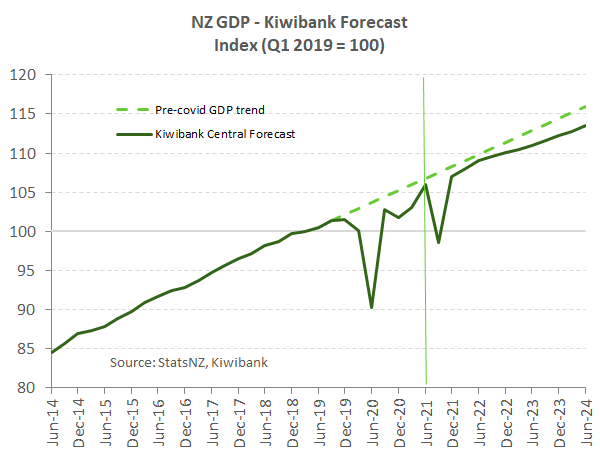

A short, sharp shock to GDP

The Kiwi economy entered the latest lockdown on a firm footing. Supercharged GDP growth of 2.8% was recorded in the June quarter, and the labour market had returned to full employment. But the Delta outbreak has disrupted the recovery. We are expecting a 7% fall in Q3 GDP. A short, sharp fall from lockdown.

The disruption however is expected to be followed by a rebound in the December quarter. Several high-frequency data are showing encouraging signs. NZIER’s latest QSBO showed an anticipated knock to near-term confidence, but the all-important outlook for firms’ own activity and hiring intentions held up surprisingly well. As we’ve learnt from previous lockdowns, demand is deferred not destroyed. Economic activity bounces back once the restrictions are relaxed. We’ve pencilled in a rebound in GDP of 8.5% in Q4. However, with some form of lockdown, especially in Auckland, dragging into the fourth quarter, there’s growing downside risk to our forecast. So long as lockdowns are part of the covid playbook, large swings in economic activity are expected.

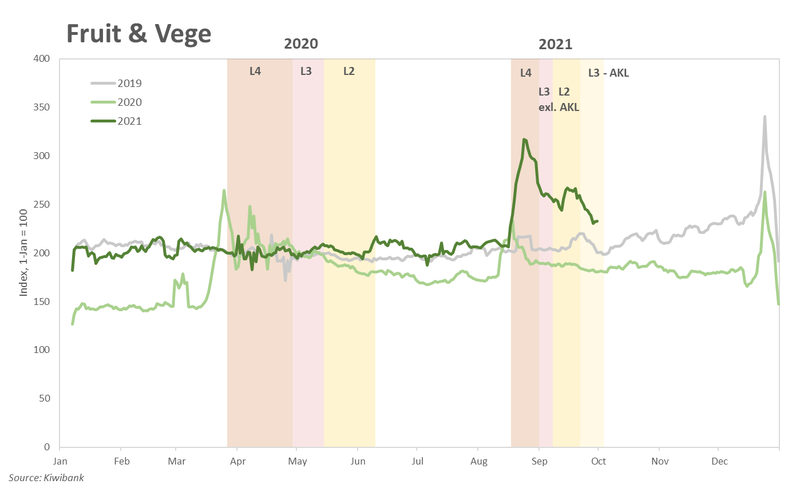

Food Spend

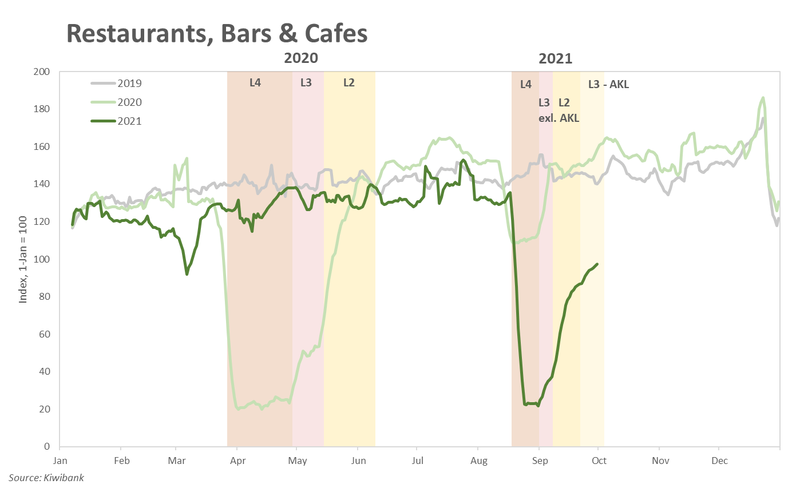

Hospitality Spend

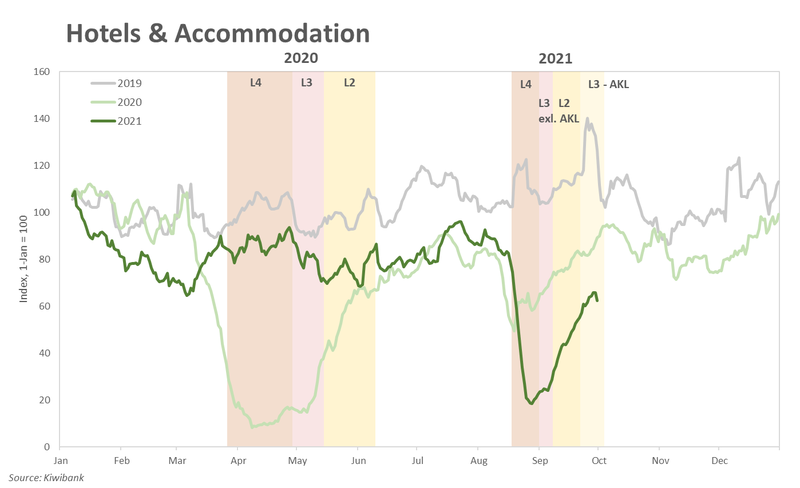

Household Spend

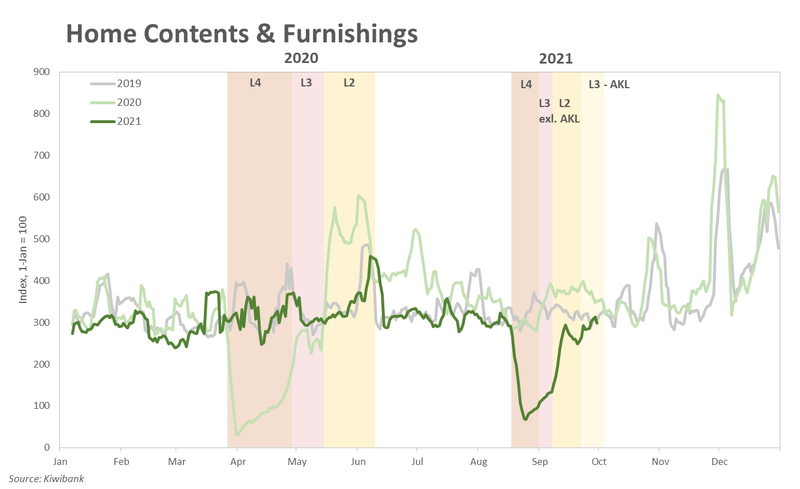

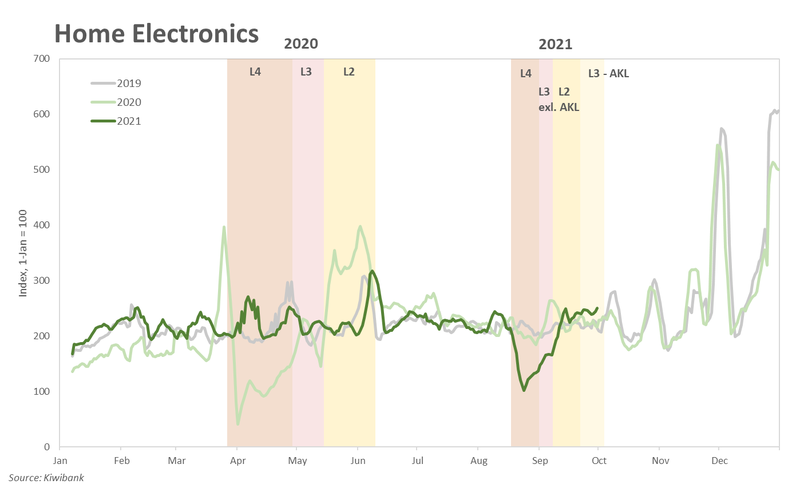

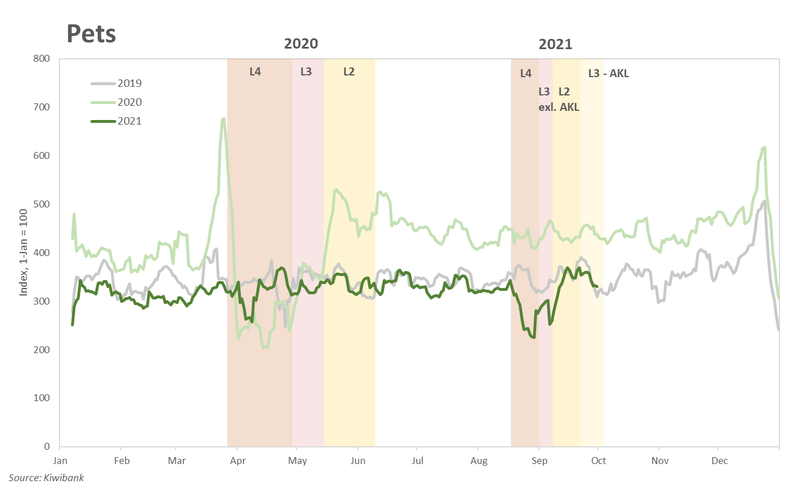

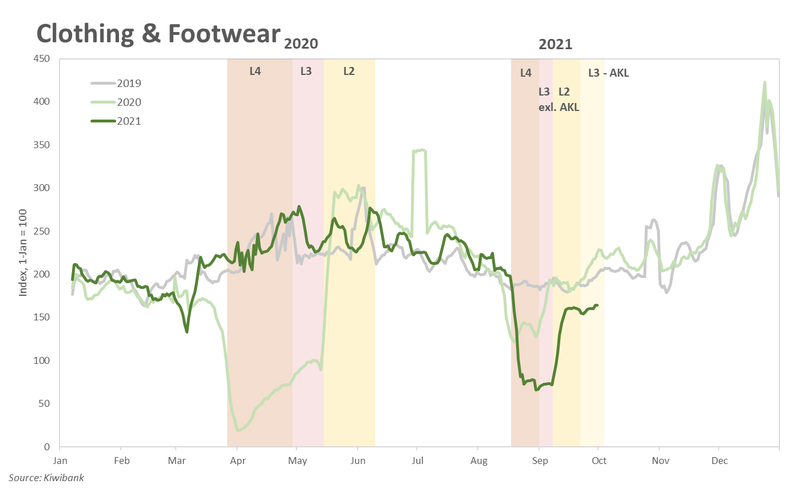

Retail Goods & Services Spend

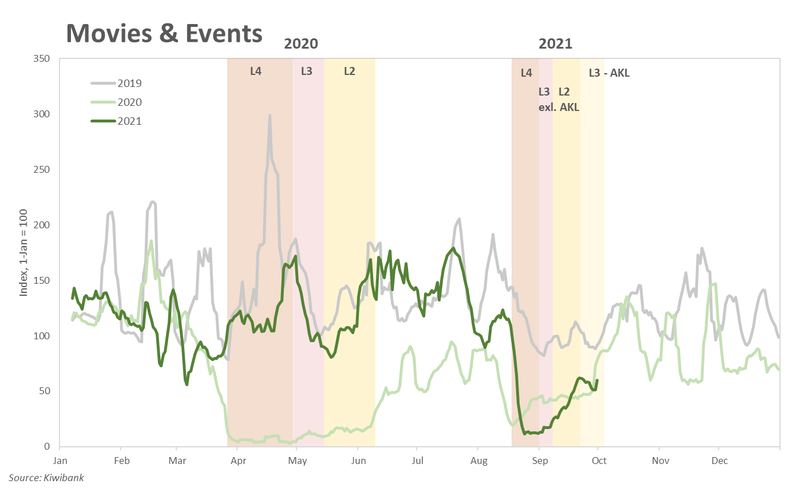

Transport & Travel Spend