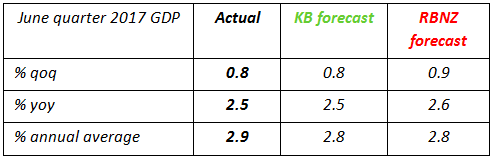

Key Points: - Over the June quarter, the NZ economy expanded by 0.8% - in line with our forecast and consensus expectations. This leaves annual GDP growth at a pace of 2.5% yoy.

- The key drivers of growth over the quarter were the tourism industry, a rebound in food manufacturing and underlying demand for professional services.

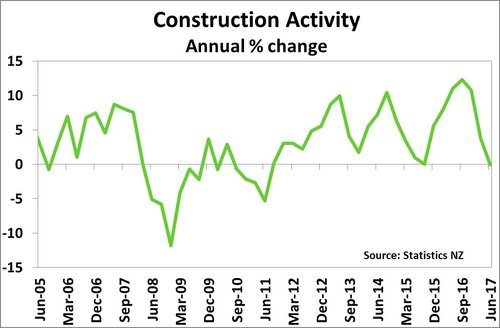

- The construction industry is running up against capacity constraints, which given the pipeline of work forecast in coming years, we expect will start resulting in rising costs in the industry.

- We continue to expect that the RBNZ will leave the OCR on hold until the end of 2018.

Summary

This morning’s Q2 GDP data was bang in line with our forecast with the economy expanding by 0.8% qoq, leaving annual growth at 2.5% yoy. This was slightly weaker than the RBNZ’s forecast for a 0.9% qoq expansion over the quarter, but we don’t see this as having an impact on the RBNZ’s view. In addition, Q1 growth was revised up slightly to 0.6% qoq, from 0.5% qoq previously. While headline growth remains just below estimates of potential growth in economy, we are seeing a shift in the composition of growth - away from the significant boost from the construction industry seen just six months ago and toward more general widespread demand. We expect to see growth remain robust in the year ahead, but there are increasing issues around capacity in some sectors.

These capacity constraints could mean that the potential growth in the

economy in the years ahead ends up being lower than current estimates (2.7-3%

yoy). That could particularly be the case if we see lower net migration and/or

a decline in workforce participation. This would mean that as economic growth

strengthens heading into next year, actual growth could exceed potential growth

sooner than expected by the RBNZ. This provides support to our view that

domestic inflation pressures will lift from current levels as competition

increases for a limited set of resources. The extent of the economic expansion

may also in part depend on how much fiscal spending we see following the

general election, and where that spending is focused.

Underlying activity is respectable

Despite some temporary factors influencing headline GDP growth in the June quarter (see below for details) domestic demand continues to record respectable growth. On the expenditure side of GDP, private consumption activity expanded 0.9% qoq, as households continue to open their wallets, helping to see expenditure GDP expand by 1.1% in the quarter. On an annual basis, private consumption expanded 4% yoy down from 5.3% in the March quarter, but still holding up strongly. Consumers increased spending on both durables and services in the quarter. Measures of consumer confidence over the September to date suggest that households remain in a mood to spend over the current quarter.

Solid export growth also looks to be supporting underlying activity. In addition, commodity prices for a number of key export commodities such as dairy strengthened over the period. Whole milk powder prices have traded over US$3,000/mt on the Global Dairy Trade auction for most of 2017 to date and are expected to remain strong. Exports were also driven by a jump in tourism-related services, which was enhanced by international sporting events over the quarter. However, stripping out these temporary factors suggests that tourism activity remains elevated, contributing to underlying activity. Subtracting a conservative estimate of visitor arrivals due to these temporary sporting events, points to a respectable annual increase in remaining number of visitor arrivals in the June quarter.

It’s easy to see why underlying activity is holding up, with

migration-led population growth remaining elevated, strong commodity prices

supporting primary exporters, and tourism activity buoyant. However, the

economy continues to exhibit growing pains, particularly in relation to the

construction sector. On an annual basis construction activity remained largely

flat. However, we believe that recent softness in construction activity has

been dominated by supply side constrains, rather than demand side factors. The

construction sector looks to have come up against capacity constraints, with

widespread anecdotes of acute skill shortages and tighter funding conditions in

the sector. In addition, the softness in construction over the first half of

2017 follows a period of double digit growth through much of 2016 that is not

sustainable.

Temporary factors give a boost

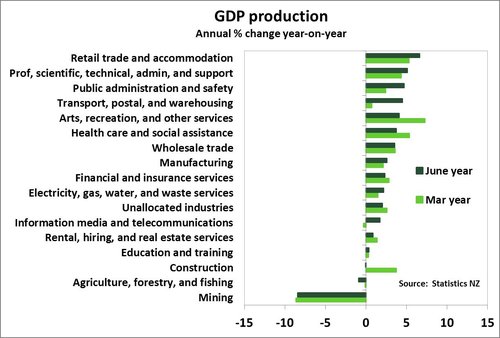

Over the June quarter there were a few areas of the economy that experienced a boost due to temporary factors. One of these was the tourism industry, which received a significant boost from two major events, namely the World Masters Games and the British and Lion’s rugby tour. Over the June quarter, tourist arrivals from the UK almost doubled – providing a significant increase to visitor spending. This showed up in both the production data – with the ‘retail trade and accommodation’ sector expanding 2.8% over the June quarter – and also in expenditure GDP through an increase in export services (tourism-related services get measured as an export). As highlighted above, we have seen tourism continue to see experience robust underlying demand with annual growth in the sector of 6.6% yoy. Given that the Lion’s tour finished in July, we expect the September quarter GDP numbers to continue to be underpinned by strong tourist spending.

Furthermore, the underlying appeal of NZ as a tourist destination shows no signs of letting up. But similar to the construction industry, we are seeing rising capacity constraints impacting the pace at which the sector can keep expanding. Occupancy rates have increased across all the typical accommodation providers (hotels, motels, backpackers etc) and that is even taking to account the emergence of property-sharing accommodation options such as AirBnB – which now has over 20,000 listings in NZ. Infometrics has estimated that AirBnB accounted for almost 1 million guest nights over the year to March 2017. While AirBnB remains a small part of the commercial market – which totalled 38.5 million guest nights over the same period – there is evidence that there is strong demand (with international guest nights increasing over 8% in the year to June) for accommodation services that warrant increasing supply.

Outside of the tourism industry, there was a solid rebound in food

manufacturing in the June quarter. This followed two quarters of declines in

volumes due largely to the weak start to last year’s dairy season. In addition,

on the expenditure side, there was evidence of strong demand for dairy exports

– which rose 19% in the June quarter – as well of exports of meat and forestry

products. This meant that exports posted an impressive 5.2% qoq expansion in

the second quarter, the largest quarterly increase since late 2014. Forestry

products also experienced a notable rebound in exports over the quarter.

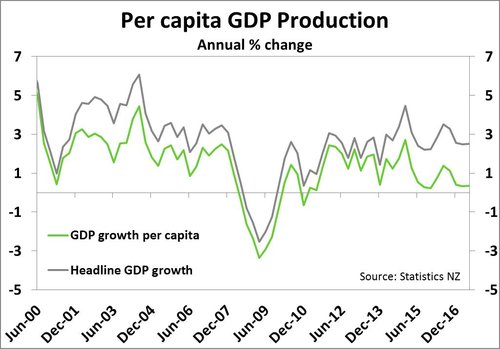

Purchasing power and per capita GDP gradually catching up

On a per capita basis, GDP growth has

improved marginally, from an annual pace of 0.3% yoy in March up to 0.4% yoy in

June. While headline growth in the economy has always exceeded GDP per capita,

the gap appears to have widened in recent years (see chart below). We suspect this growing gap is somewhat due

to population growth being the strongest we have seen since the 1970s (partly

due to record high net migration numbers) as well as an aging population and

soft productivity growth.

Real gross national disposable income (RGNDI) – which is essentially a measure of NZ’s purchasing power – rose 1.4% over the June quarter in part due to a rising terms of trade. On a per capita basis the gain in disposable income was slower - rising 0.9% qoq, to be up 1.8% yoy. However this is still is a relatively positive result that shows the country has experienced an increase in purchasing power above and beyond population growth – essentially improving the relative wealth of NZ.

Policy implications

From the RBNZ’s viewpoint, today’s data suggests that the economy continues to expand largely in-line with the August Monetary Policy Statement (MPS) forecasts. However we are seeing rising capacity constraints in the construction and tourism industries – areas which until recently had been providing a strong back-bone for economic growth. This means that we need to see other sectors step-up to the plate in order to keep the economy growing. We are already seeing some signs of that, with professional services growing, and the impact of a larger population increasing demand for healthcare and education. Despite the recent slowdown in the housing market, consumer confidence remains upbeat and that’s feeding into decent consumption spending. In addition, firms generally remain upbeat and employment intentions are strong.

With growing capacity pressures in some areas and the broader economy expected to remain robust, we expect to see rising domestic inflation pressure in coming years. As such, we have maintained our view for the RBNZ to hike interest rates from the end of 2018 (we will release a preview note on the RBNZ’s September OCR Review on Monday).

In addition, the global economic outlook has improved somewhat in the past few months (geo-political risks aside) and the OECD has slightly revised up its outlook for the global economy relative to its June forecasts. At the same time we have seen global central banks show an increased appetite for tighter monetary policy – including the US Federal Reserve, the Bank of England, the Bank of Canada and the European Central Bank. While this is yet to have a significant impact on the NZ dollar, rising global interest rates while the RBNZ remains on hold are expected to result in a lower NZ TWI over time. In addition, a stronger global economy will also help boost demand for our export products.

Domestically it’s all eyes on the general election this weekend. Based

on latest polling no one party is likely to gain enough votes to govern alone

and so it may take some time before a coalition government is formed. From an

economic viewpoint, the key question marks are over policies regarding net

migration, housing and the central bank, with some of the minority parties

having more extreme views compared to the two majors. Which policies end up

being non-negotiable for each minority party remains to be seen and could add

to the uncertainty in the coming weeks.

Market reaction

It has been a busy 24 hours for the NZ dollar. The latest Colmar Brunton poll showed that National had taken the lead again, rising 6 points to 46% of the vote, with Labour down to 37%. Financial markets reacted positively to the National lead in the polls, with the NZD/USD rallying about 60 points to $0.7370. However, the US Federal Reserve’s policy meeting announcement then saw some of those gains retraced early this morning. There was hardly any reaction in financial markets to the GDP data release, although the NZD/USD has been grinding lower to trading around $0.7330.

We have seen global yields lift in the past week and this has put upward

pressure on our local interest rate curve. The benchmark 2-year swap rate has

moved from a year-low of 2.13% in early September up to trading around 2.27% currently.

The OIS market has now moved to pricing in a rate hike from the RBNZ in

September 2018, from November a week ago.