Key Points:

- This morning’s inflation data printed in line with our expectations at 0.5% qoq, but was higher than the market consensus and the RBNZ’s forecasts.

- Annual inflation rose to 1.9% yoy, up from 1.7% yoy in June. Housing-related costs and higher food prices were key drivers of price pressure.

- We expect that inflation will remain higher than the RBNZ expects in coming quarters as capacity pressure intensify and the NZ dollar softens. We maintain our view that the RBNZ will need to start gradually lifting the OCR from late 2018.

- Despite the upside surprise, there was a minimal reaction in financial markets as traders focus on and await an announcement on the next NZ government.

Summary

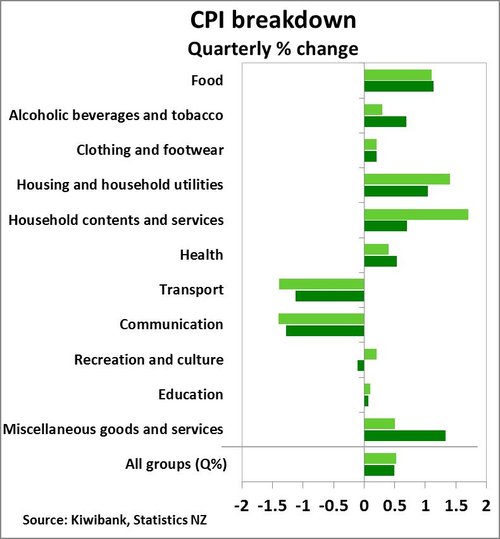

The September quarter CPI data printed above market consensus forecasts (+0.4% qoq) and the RBNZ’s August Monetary Policy Statement (MPS) forecast (+0.2% qoq). However, the 0.5% quarterly rise in consumer prices was in line with our expectations - taking annual inflation up to 1.9% yoy. On an annual basis, higher housing-related costs and food prices (vegetable prices in particular) have been the areas where prices have risen the fastest. On the downside, the communications sector continues to see prices decline on a quality adjusted basis – unsurprising when you think about the latest features of a new iPhone compared with the model from a few years ago.

While the solid annual inflation rate will be a pleasant surprise for the RBNZ, what matters from a monetary policy viewpoint is the extent of core inflation pressure and the outlook for growth and inflation in the next couple of years. In that regard, our view remains that capacity pressures will continue to see domestic inflation increase even as growth eventually starts to cool. If the local exchange rate continues to depreciate (helped further by global central banks tightening monetary policy), then tradables inflation will also move higher in the coming year – adding further upside to the RBNZ’s current inflation outlook.

While the solid annual inflation rate will be a pleasant surprise for the RBNZ, what matters from a monetary policy viewpoint is the extent of core inflation pressure and the outlook for growth and inflation in the next couple of years. In that regard, our view remains that capacity pressures will continue to see domestic inflation increase even as growth eventually starts to cool. If the local exchange rate continues to depreciate (helped further by global central banks tightening monetary policy), then tradables inflation will also move higher in the coming year – adding further upside to the RBNZ’s current inflation outlook.

Combining these factors, we still expect the RBNZ to start gradually lifting the OCR from late 2018. However, there remains a high level of uncertainty around the path of fiscal policy given the lack of clarity around the composition of a new government.

Housing cost increases set to continue

The housing market remains a strong driver of price increases in New Zealand, with the cost of new housing a major driver, but also other housing-related costs experienced some of the biggest price increases. The cost of new housing rose 1.1% qoq, and is now running at an annual rate of 5.4% yoy (6.8% yoy in Auckland). In addition, the cost of property maintenance services also rose 1.1% qoq, to be 3% higher over the past year. Given the reported levels of capacity pressure in the construction industry – particularly around a shortage of skilled tradespeople – we expect prices for new dwellings to continue to rise in coming quarters.

The September quarter is when local authorities set their annual rates and this quarter saw a larger increase in rates than the previous year. Property rates rose 3.5% over the September 2017 quarter as councils responded to rising property prices and operating costs. Adding to the cost for homeowners, we have also seen a sharp increase in dwelling insurance premiums, up 6.1% qoq and 12.1% over the past year. In fact, in the past five years the insurance premiums for residential dwellings have increased over 50%.

After a couple of softer quarters, the household contents and services group saw a bit of a rebound over the September quarter (+0.7% qoq). Furniture and furnishings saw prices increase 1.8% qoq and household appliances also rose – although the costs of these items remains lower than seen a year ago. With home sales almost 30% lower compared with last year, fewer properties changing hands has generally seen less demand for new furniture and appliances.

Our view is for house sales to pick up again in coming months once we have confirmation of a government and the summer-selling season kicks off. There remains a supply shortage of residential property (especially in Auckland) that is likely to see demand for housing remain strong. One missing part of the puzzle in Auckland has been the lack of rent increases. Rents across NZ increased 0.6% qoq, and by a more moderate 0.5% qoq in Auckland. Over the past year, rents nationwide have risen 2.2%. We expect rents will start to rise more rapidly as property investors start passing on the higher costs of maintenance, insurance and rates – and eventually higher mortgage repayment costs as interest rates rise.

Expensive fare

A notable contributor to September quarter inflation came from a lift in food prices, rising 1.1% qoq and contributing 0.2%pts to headline inflation. Higher prices for vegetables, particularly tomatoes (up a whopping 34% qoq), were the main driver. Adverse growing conditions through 2017, as a result of above average rainfall in key growing regions, have disrupted supply and pushed prices higher. While weather-related disruptions to fresh produce production are usually temporary in nature, the price impact from the most recent episode looks likely to linger for a little longer. For instance, potato growers have recently expressed concern regarding the quality of current crop – struggling in waterlogged soil. In addition to fresh produce prices, grocery food prices also lifted in the quarter. An earlier recovery in commodity prices, including dairy prices, has fed into higher prices of some consumer staples – the eye watering $5+ price for a block of butter has been grabbing headlines recently. On an annual basis, food prices were 2.8% yoy higher and again propped up by a jump in vegetable prices (+9% yoy).

Cheaper petrol and phone calls weighed on inflation

The largest price falls in the September quarter were recorded in the transport and communication groups. The 1.1% qoq fall in transport prices was in part due to lower petrol prices. Petrol prices fell 1.7% qoq, with StatsNZ recording the average price of 91 octane petrol over the quarter at $1.83 being 3 cents cheaper than the June quarter. Looking ahead, the fall in petrol prices look to be short lived. The NZ dollar has depreciated over the last few months and has helped to push prices up at the pump. Lower petrol was not the only drag on the transport group in the September quarter. International airfares were down 5.5% qoq and vehicle relicensing fees dropped 8% qoq as a result of another annual adjustment to the ACC levy component.

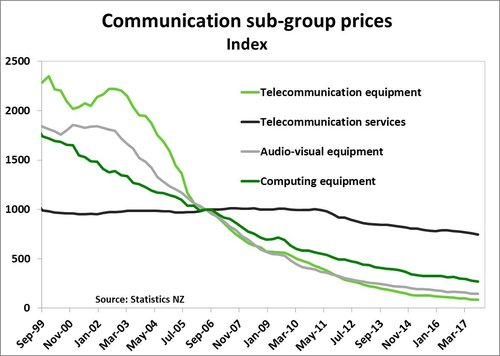

The communication group continued its long-term structural fall in prices, declining 1.3% qoq. Highlighting the structural decline in prices, the communication group weighed on annual inflation falling 5.3% yoy – a stronger decline than the 4.6% yoy fall in the previous quarter. Statistics NZ noted that the quarterly fall in communication prices reflected better-value telecommunication services. Also at play here is the sustained fall in the price of telecommunication equipment. Similar to home computers, telecommunication equipment such as the smartphone is constantly experiencing improvements in capability – such as faster processing speed – while maintaining certain price points. These improvements in product quality are reflected in the CPI as a fall in price.

The communication group continued its long-term structural fall in prices, declining 1.3% qoq. Highlighting the structural decline in prices, the communication group weighed on annual inflation falling 5.3% yoy – a stronger decline than the 4.6% yoy fall in the previous quarter. Statistics NZ noted that the quarterly fall in communication prices reflected better-value telecommunication services. Also at play here is the sustained fall in the price of telecommunication equipment. Similar to home computers, telecommunication equipment such as the smartphone is constantly experiencing improvements in capability – such as faster processing speed – while maintaining certain price points. These improvements in product quality are reflected in the CPI as a fall in price.

Policy implications & core inflation measures

For the RBNZ, it is probably a nice turnaround to see inflation numbers surprising on the upside rather than the downside – as had been the case for the past few years. Some of the upside surprise was likely caused by a turnaround in fuel prices near the end of the September quarter, with tradables inflation coming in at 1% yoy versus the RBNZ’s forecast of 0.4% yoy. But non-tradables inflation was also stronger than the bank anticipated – at 2.6% yoy versus the Bank’s forecast of 2.4% yoy. Given the capacity pressures emerging in several areas of the economy, we expect that domestic inflation will remain solid around current levels while a softer NZD should boost tradables inflation in coming quarters. Over the September quarter, the NZ TWI averaged 1.7% lower than the RBNZ's forecasts for the quarter and has also started the December quarter at a weaker level. The impact from a lower NZD typically takes about 1-2 quarters to be fully reflected in higher prices for tradable goods and services.

The trimmed mean measures of inflation (which adjust for extreme price movements) also painted a solid picture of underlying price pressure. The trimmed mean measures all showed a quarterly price increase of 0.5% qoq with the annual figures ranging from 1.9% to 2.1% yoy. In addition, headline inflation (less food, household energy and vehicle fuels) also increased 0.5% qoq – suggesting that there is still underlying price pressure once some of the more volatile components are removed. We suspect that the RBNZ’s sectoral inflation model (due out at 3pm this afternoon) will show a small increase in core inflation pressure, up from the 1.4% yoy sectoral inflation rate in June.

In isolation, today's data doesn't necessarily threaten the RBNZ's projection for the OCR to remain on hold until at least mid-2019. In our view however, inflation will also continue to print above the RBNZ's August MPS inflation forecasts for the next few quarters. In August, the RBNZ forecast inflation to pull back to a rate of 0.7% yoy in the March 2018 quarter before starting to rise again. But based on the capacity pressures we are seeing, combined with a softer NZ dollar, we only see inflation pulling back to a rate of around 1.4% yoy in March 2018 – and then rising back to around 2% in the second half of 2018. Hitting the magic 2% inflation rate isn't as important as the underlying trend and measures of core inflation - but today's data indicates that these are also showing signs of remaining higher.