Key Points:

- Headline business confidence fell to a net 7% of firms optimistic about the general economy over the next six months from a net 17% in June.

- The fall is in part due to pre-election uncertainty, given the range of policies on the table and the closeness of the polls.

- However, the fall looks temporary in nature with firms’ outlook for their own domestic trading activity (DTA) lifting to a 27% of firms expecting a busier quarter ahead.

- In another encouraging sign firms are still looking to hire and invest.

- Today's survey has little impact on the outlook for monetary policy. The RBNZ will be looking for clearer fiscal policy direction heading into the November Monetary Policy Statement (MPS).

Summary

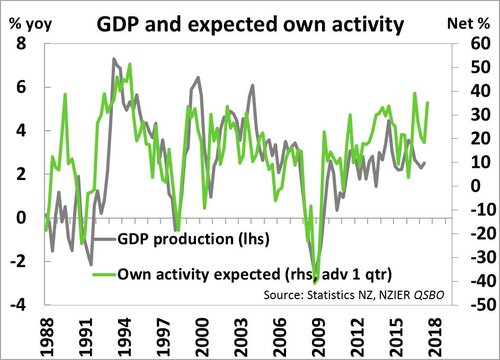

This morning’s NZIER Quarterly Survey of Business Opinion (QSBO) for the September quarter showed a slump in general confidence among firms. A net 7% of firms expect the economic outlook to improve, down from a net 17% in June. The drop in confidence was expected, given similar declines seen in other business sentiment surveys, and is at least partly related to uncertainty heading into the general election. The theme of pre-election jitters was reinforced by the fact that confidence eased in almost all regions of NZ. We expect to see confidence rebound in the December quarter, assuming a smooth and quick period of negotiations and formation of a new government. Firms’ domestic trading activity (DTA) over the past quarter fell by a much more modest 4%pts to a net 13% of firms experiencing a lift in activity. More importantly, firms' outlook for their domestic trading activity actually lifted to a net 27% of business expecting a rise in activity in the coming quarter - up from 24% in June. This is supportive of growth of around 3% yoy over the year ahead (see chart below). Despite the latest hit to business confidence, firms still look to be in a mood to hire and invest – adding to the argument that the more downbeat view is only skin deep.

This morning’s NZIER Quarterly Survey of Business Opinion (QSBO) for the September quarter showed a slump in general confidence among firms. A net 7% of firms expect the economic outlook to improve, down from a net 17% in June. The drop in confidence was expected, given similar declines seen in other business sentiment surveys, and is at least partly related to uncertainty heading into the general election. The theme of pre-election jitters was reinforced by the fact that confidence eased in almost all regions of NZ. We expect to see confidence rebound in the December quarter, assuming a smooth and quick period of negotiations and formation of a new government. Firms’ domestic trading activity (DTA) over the past quarter fell by a much more modest 4%pts to a net 13% of firms experiencing a lift in activity. More importantly, firms' outlook for their domestic trading activity actually lifted to a net 27% of business expecting a rise in activity in the coming quarter - up from 24% in June. This is supportive of growth of around 3% yoy over the year ahead (see chart below). Despite the latest hit to business confidence, firms still look to be in a mood to hire and invest – adding to the argument that the more downbeat view is only skin deep.

We expect the QSBO data to have minimal impact on the RBNZ’s view given the distortions resulting from pre-election uncertainty. We expect the RBNZ will want to wait for clarity on the make-up of the government and future fiscal policy – heading to the November MPS. Today’s QSBO doesn’t change our view that the RBNZ will keep the OCR unchanged at 1.75% until late 2018.

Hiring and investment intentions solid

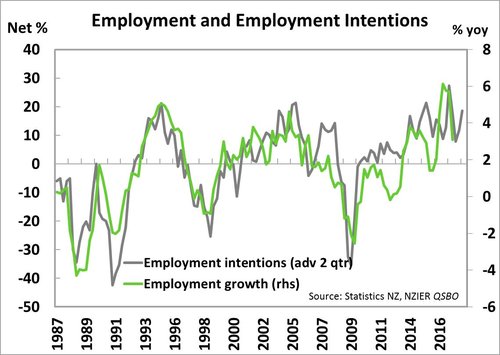

Despite the drop in headline confidence figures, firms have continued to recruit new staff and invest in recent months. A net 14% of firms hired staff over the September quarter – in line with June’s numbers. In addition, another 19% expect to hire in the coming quarter which points towards employment growth remaining solid around the current pace of 3% yoy (see chart below). By sector, the services and manufacturing industries both look to be key areas of employment growth in the quarter ahead. However, firms appear to be finding it increasingly hard to find skilled labour which may start limiting the pace at which they can hire and expand.

Despite the drop in headline confidence figures, firms have continued to recruit new staff and invest in recent months. A net 14% of firms hired staff over the September quarter – in line with June’s numbers. In addition, another 19% expect to hire in the coming quarter which points towards employment growth remaining solid around the current pace of 3% yoy (see chart below). By sector, the services and manufacturing industries both look to be key areas of employment growth in the quarter ahead. However, firms appear to be finding it increasingly hard to find skilled labour which may start limiting the pace at which they can hire and expand.

Investment intentions also both remained robust according to the NZIER survey. There was a rebound in plans to invest in buildings (with a net 18% of firms expecting to increase spending, up from 3% in June) while plant and machinery intentions held up at a net 17%. The fact that firms remain comfortable investing in fixed assets adds to the view that the current dip in headline confidence is likely to be temporary.

Capacity constraints ease but remain elevated

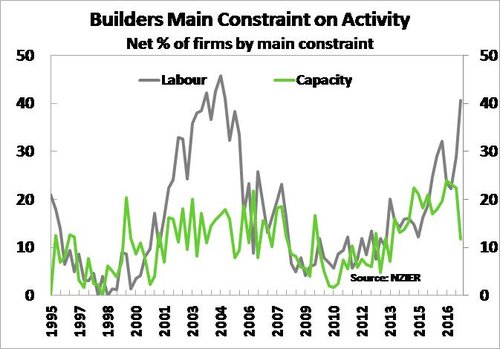

Capacity constraints generally eased further over the September quarter. Nevertheless, these measures remain elevated and capacity is a notable limiting factor for business. Capacity utilisation fell to a net 91.3% of business facing or expecting increased capacity utilisation, compared to a reading of 93.5% at the start of the year, but remains above the survey average of 89.3%. Capacity is still coming through as a key limiting factor to turnover, with 14.5% of firms noting it as an issue, although this is down from 15.6% in the June quarter. Difficulty finding skilled labour was essentially unchanged in the quarter, while unskilled labour became more difficult to find. Labour as a capacity constraint in the building sector remains elevated, with a net 41% of firms noting labour as the largest limiting constraint - the highest level since 2004 when we were in the midst of the last building boom.

While some QSBO measures are showing elevated capacity constraints, firms’ pricing intentions have not responded anywhere near the same degree. A net 24% of firms expect to increase prices in the coming quarter, on par with the previous quarter, but behind the survey average of a net 31%. Nevertheless, cost increases faced by businesses look to be intensifying, given a net 30% of firms noted rising costs, up from a net 26% in the previous quarter. All told, this suggests firms are experiencing margin compression and at some point are likely to pass this through to prices.

Builders’ confidence takes a hit

The building industry experienced a hit to confidence in the last three months – hinting that construction growth will remain subdued in the September quarter. New orders taken slumped to a net 0% in September from a net 38% last quarter. However, the net share of firms that expect to see a rise in new orders in the coming quarter remained at an elevated level – signalling a bit of a post-election rebound. Architects' expectations, another forward indicator of future construction activity, held up pretty well. Planned government work expectations lifted to a net 36% of architects expecting more work over the year ahead, although the level of expected housing work pulled back after a very strong read in June. It remains to be seen how much of the current fall in confidence is in response to the downturn seen in the housing market. Once the uncertainty from the current election is out of the way, we are expecting a pick-up in activity in the housing market.

The building industry experienced a hit to confidence in the last three months – hinting that construction growth will remain subdued in the September quarter. New orders taken slumped to a net 0% in September from a net 38% last quarter. However, the net share of firms that expect to see a rise in new orders in the coming quarter remained at an elevated level – signalling a bit of a post-election rebound. Architects' expectations, another forward indicator of future construction activity, held up pretty well. Planned government work expectations lifted to a net 36% of architects expecting more work over the year ahead, although the level of expected housing work pulled back after a very strong read in June. It remains to be seen how much of the current fall in confidence is in response to the downturn seen in the housing market. Once the uncertainty from the current election is out of the way, we are expecting a pick-up in activity in the housing market.