Key Points:- The RBNZ is widely expected to leave the OCR unchanged at 1.75% on May 11. With no change expected in the cash rate, the focus will be on the tone of the accompanying Statement and the Bank’s forward guidance.

- While we still expect the OCR to be on hold for a while yet, there have been several key data developments that have prompted us bring forward our view on the timing for an OCR hike. We now expect to see the RBNZ start lifting the OCR at the end of 2018, as opposed to mid-2019.

- We anticipate that the Bank will also to move forward the timing of predicted interest rate hikes in its OCR track to early 2019, from late 2019 previously. However, OIS market pricing is still too aggressive, with a full 25bp hike priced in by March 2018.

- The extent of the market reaction to the MPS will depend on how far the RBNZ shifts its 90-day track and how many hikes in total are implied.

Summary

The RBNZ is widely expected to leave the OCR unchanged at 1.75% at its May 11 Monetary Policy Statement (MPS). While there have been several key pieces of data out since the RBNZ last completed a full forecast round in February, we expect the general tone to remain cautious while acknowledging a higher starting point for inflation and a lower exchange rate. The global growth outlook has strengthened marginally, but global geo-political tensions remain elevated. While we still expect the RBNZ to leave the OCR on hold in the near-term, we have shifted forward our expectation for the timing of OCR hikes to start in late-2018 (previously mid-2019).

Inflation is now comfortably around the RBNZ’s target at 2.2% yoy. However, a slightly more subdued economic growth profile, combined with tighter financial conditions, mean that we see a minimal risk of inflation running away on the RBNZ. In our view the Bank can afford to sit on its hands and wait until late next year before needing to lift the OCR. We expect the RBNZ to emphasise a similar view in the May MPS.

Softer growth, stronger inflation – where does that leave us?

Since the February MPS we have seen both growth and inflation data which provide the RBNZ with new starting points for its forecasts. The New Zealand economy expanded at a pace of 2.7% yoy over 2016 – weaker than the RBNZ’s forecast for growth of 3.5% yoy in Q4 2016 and also softer than market expectations. This lower growth rate was caused by some one-off factors, such as a slow start to the dairy season, which we expect to see at least partially reversed at the start of 2017. However, with rising capacity constraints in the tourism and construction industries and household spending having pulled back somewhat, we now expect annual growth this year to be closer to 3% rather than the 4% yoy pace the RBNZ was forecasting by mid-2017. We expect a more muted pace of growth to keep domestic inflation pressure well contained – particularly outside of key stress areas such as construction and tourism.

While growth weakened, inflation at the start of 2017 jumped to the highest level seen since 2011. The headline CPI increased by 1.0% qoq in the March quarter, taking annual inflation up to a pace of 2.2% yoy. This was a decent jump up from inflation at 1.3% yoy at the end of 2016 and was significantly higher than the 1.5% yoy pace that the RBNZ was forecasting for March 2017. Similar to the GDP data, there were a couple of one-off factors that drove the results (such as an unusual spike in food prices and an excise tax increase). However, the trimmed mean measures of inflation (which strip out significant one off drivers) were also up around 2% yoy, indicating that there was also some solid underlying price pressure coming through.

The higher starting point gives some upside to the RBNZ’s previous inflation forecasts and we expect these to be shifted slightly higher in the May MPS. In the wake of Cyclone Cook, we expect to see prices for some fresh fruit and vegetable produce remain elevated in the June quarter, keeping inflation at around 2% yoy. Thereafter we anticipate that annual inflation will moderate to just below 2% over the second half of 2017. A key risk to this outlook would be a further sustained decline in the NZ TWI (see below) which could boost tradables prices by more than we currently anticipate. Given the high volatility we have seen in the currency in recent months, we are cautious about baking an appreciably lower NZ TWI into our view.

Domestic developments

Aside from the recent headline growth and inflation numbers, there have been several important pieces of NZ economic data since the RBNZ last ran its full forecasting round in early February. In a speech in March, RBNZ Governor Wheeler highlighted several of the key domestic uncertainties that they were watching, including; commodity prices, net migration, the exchange rate, the housing market and household savings and consumption decisions. Below we examine how some of these variables are faring.

New record highs in net migration: Net migration continues to rise to new highs, increasing to an annual pace of around 72,000 in March 2017. While departures have flattened off at about 57,000 per year, arrivals have continued to increase as more New Zealanders return home and an increasing number of new migrants arrive on work visas to meet skilled labour requirements. The NZ government recently announced changes to residence requirements for skilled migrants, introducing remuneration thresholds and increasing the point requirement for residency applications under the skilled migrant category (SMC). These changes come into effect from mid-August 2017. While this could discourage a few people from coming to NZ as it makes it harder to settle here in the long-term, we don’t expect these changes to have a material impact on the number of arrivals we are seeing.

We expect net migration to remain elevated above 70,000 for the next six months (absent any significant change in government policy) before gradually starting to decline as employment opportunities overseas start to improve. This outlook contrasts with the RBNZ’s view that net migration numbers will decline from here. Stronger migration numbers will add some upside to the demand side to the economy, but also boost the available supply of workers in the economy. This is likely to keep the unemployment rate steady at around 5% as employment growth and the labour force increase at a similar pace. We expect to see some wage inflation pressure emerge as workers demand higher wages in line with rising headline inflation – real wage growth turned negative at the start of the year.

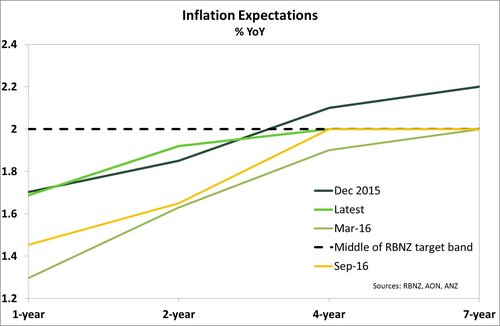

Inflation expectations back on track: At the start of 2016, one of the key catalysts for the RBNZ cutting the OCR again was a sharp drop in inflation expectations. Expectations of future inflation are important for the central bank as they have an impact on businesses price and wage setting behaviours, which in turn gets fed into actual inflation – something of a self-fulfilling prophecy. Evidence has shown that inflation expectations have becoming increasingly driven by actual levels of inflation and hence as headline inflation has improved in recent quarters, we have seen a bounce back in market expectations for future inflation too (see chart below) and are expected to remain around the RBNZ’s target.

Inflation expectations back on track: At the start of 2016, one of the key catalysts for the RBNZ cutting the OCR again was a sharp drop in inflation expectations. Expectations of future inflation are important for the central bank as they have an impact on businesses price and wage setting behaviours, which in turn gets fed into actual inflation – something of a self-fulfilling prophecy. Evidence has shown that inflation expectations have becoming increasingly driven by actual levels of inflation and hence as headline inflation has improved in recent quarters, we have seen a bounce back in market expectations for future inflation too (see chart below) and are expected to remain around the RBNZ’s target.

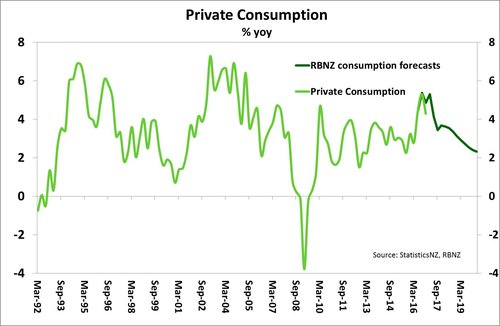

Consumption: Consumption growth pulled back toward the end of 2016 after very strong growth through the middle of last year. The RBNZ’s forecasts had consumption remaining elevated around those levels in response to a range of factors. However, there are some signs that domestic consumption is pulling back earlier than the RBNZ forecast (see chart below) in response to a softening housing market (particularly in Auckland) and rising mortgage rates. If consumption growth is closer to the pace seen over 2012-2015 then this would lower domestic growth and reduce capacity pressure in the economy. All else equal this could delay the timing of OCR hikes and/or reduce the extent of hikes required to keep inflation within the Bank’s target band.

Consumption: Consumption growth pulled back toward the end of 2016 after very strong growth through the middle of last year. The RBNZ’s forecasts had consumption remaining elevated around those levels in response to a range of factors. However, there are some signs that domestic consumption is pulling back earlier than the RBNZ forecast (see chart below) in response to a softening housing market (particularly in Auckland) and rising mortgage rates. If consumption growth is closer to the pace seen over 2012-2015 then this would lower domestic growth and reduce capacity pressure in the economy. All else equal this could delay the timing of OCR hikes and/or reduce the extent of hikes required to keep inflation within the Bank’s target band.

Commodity prices solid: The latest dairy auction showed another decent gain in whole milk powder (WMP) prices to trading above US$3200/mt. This is slightly above the RBNZ’s medium-term assumption which has prices trending at around US$3000/mt. However, we expect the RBNZ’s core view to remain unchanged given increasing dairy supply internationally. In addition, some of the recent strength in local prices was caused by supply concerns following Cyclone Cook and these concerns appear to be largely unfounded, particularly given that we were already near the end of production season. Fonterra’s payout forecast of $6/kgms continues to look reasonable (with possibly some small amount of upside) and a similar opening payout forecast is expected for the 2017/18 season. Outside of the dairy sector we have seen prices for our other major export commodities generally move higher.

Tradables inflation picking up

The main driver behind the upside surprise in the March CPI data was a 0.8% qoq jump in tradables prices, which took annual tradables inflation to 1.6% yoy. Some of the rise in tradables inflation was the result of temporary factors, such as higher food and fuel prices.

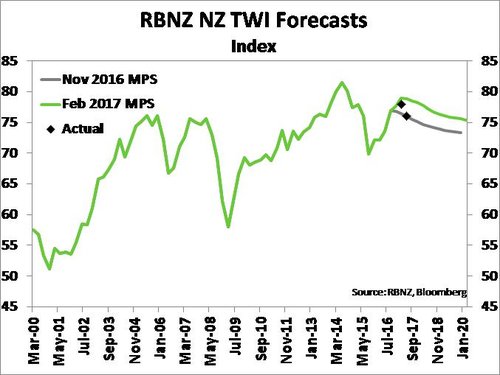

However, the extent to which tradables inflation exceeded the RBNZ’s March quarter forecast of 0.4% yoy can’t be ignored. In addition to a higher starting point, the notably weaker currency (if sustained) is expected to flow through to a higher tradables inflation track over the rest of 2017 something akin to the track presented in the RBNZ’s November MPS when the Bank’s NZ TWI forecasts were more in-line with current levels. However, the exchange rate remains a highly volatile variable and is currently being pushed around by a range of factors, many unrelated to NZ economic fundamentals. As such, we expect the RBNZ to focus on the underlying level of domestic inflation pressure rather than react to swings in the currency caused by portfolio shifts.

A sharp fall in the currency is complicating matters

Over the June quarter to date, the NZ TWI has averaged almost 3.8% below the Bank’s February MPS forecast. Rather than necessarily reflecting deteriorating economic fundamentals, the decline in the NZ TWI has been driven by moves in our major trading partners’ currencies. In recent weeks, it has been mainly political rather than economic events that have weighed on the currency, including:

• A relief rally in the Euro on the back of expectations of Emmanuel Macron winning the French Presidency in the second round vote on May 7.

• Rising geopolitical tensions between the US and North Korea, regarding the North’s desire to continue a nuclear and ballistic missile programme.

• News of a brewing spat between the US and Canada regarding dairy trade in mid-April hit the NZD hard as markets extrapolated the adverse implications of the dispute to other major dairy exporting nations including NZ (despite the fact that NZ dairy exporters already face stiff barriers to entry into the US market).

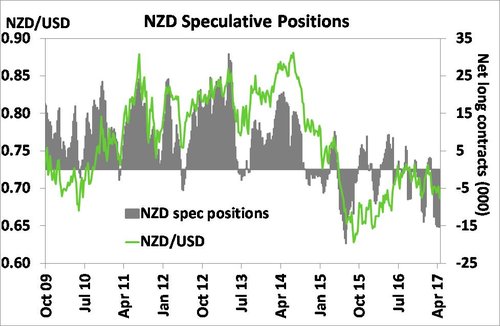

While the impact of the factors above may prove transitory, if a lower NZ TWI is sustained then this has a flow-on effect to the RBNZ’s forecasts. In previous policy statements the RBNZ has suggested that for a 4% higher NZ TWI, the OCR would need to be 125bps lower to offset the impact. If we assume this applies symmetrically when the NZ TWI declines (for portfolio reasons rather than weaker fundamentals), then this implies upside risk to tradables inflation and hence the OCR outlook. For now however, we don’t expect to see a large change in tack from the RBNZ as there is reason to believe that the recent drop in the currency might be short-lived. Speculative short positions of the NZD have built to near record levels (see chart) and any array of domestic or international developments may mean these positions quickly unwind and add upward pressure to the TWI. In fact, we have seen the NZ dollar rally in early May.

While the impact of the factors above may prove transitory, if a lower NZ TWI is sustained then this has a flow-on effect to the RBNZ’s forecasts. In previous policy statements the RBNZ has suggested that for a 4% higher NZ TWI, the OCR would need to be 125bps lower to offset the impact. If we assume this applies symmetrically when the NZ TWI declines (for portfolio reasons rather than weaker fundamentals), then this implies upside risk to tradables inflation and hence the OCR outlook. For now however, we don’t expect to see a large change in tack from the RBNZ as there is reason to believe that the recent drop in the currency might be short-lived. Speculative short positions of the NZD have built to near record levels (see chart) and any array of domestic or international developments may mean these positions quickly unwind and add upward pressure to the TWI. In fact, we have seen the NZ dollar rally in early May.

Housing market calm for now

Over the past six months the housing market in New Zealand has become more geographically diverse, with the market in Auckland cooling considerably in recent months. The RBNZ noted the moderation in the housing market over the past six months, while also being wary about assuming this trend will continue. House prices in Auckland have essentially tracked sideways, in recent months, taking annual price appreciation down to 8.5% yoy. We expect the housing market to remain quiet over the winter and heading into the September 2017 general election. But there remains a fundamental supply/demand imbalance in Auckland which at the current pace of building and migration is unlikely to be remedied in the near term. Hence we see a risk of ongoing price pressure next summer after the general election is out of the way. Outside of Auckland, we have seen many regions now playing catch-up and investors who are still in the market have been looking outside of Auckland for more attractive rental yields in regions such as Napier and Dunedin.

The other factor impacting the housing market at present is tighter financial conditions. Interest rates continue to creep higher in most tenors and the expectation of tightening monetary policy settings internationally is keeping upward pressure on the long end of the local wholesale rate curve. In addition, credit conditions in bank lending have tightened and we have seen annual credit growth slow in recent months to a pace of 8.8% yoy, from 9.1% yoy a few months ago.

Global risk events remain in play

In terms of the global economic outlook, the Bank noted in the March OCR Review that it was encouraged by recent positive economic data coming out of developed economies. But once again, the RBZNZ expressed concern that “…major challenges remain with on-going surplus capacity in the global economy and extensive geo-political uncertainty.” Since March these concerns have remained in play despite some risk factors moving closer to resolution. In France, polls suggest that pro-EU centrist French presidential candidate Emmanuel Macron is the favourite to win in the final voting round on May 7, reducing the risk of a victory from populist candidate Marine Le Pen.

However, other risks factors have arisen, such as aforementioned geopolitical tensions on the Korean peninsula. Moreover, uncertainties surrounding US fiscal and trade policy are still no closer to being resolved. The Trump administration recently released a one-page outline of their proposed tax package, which included a substantial cut to the corporate tax rate from 35% to 15% and streamlining of personal income tax brackets from seven to three. While the current outline is bold and has the potential to lift global growth and inflation, markets are no clearer on some of the key features of Trump’s fiscal policy. Markets remain in the dark about how the administration intends to pay for these cuts. A key outstanding concern for the global economy and NZ is the possibility that the US administration looks to offset lower tax revenue by increasing import tariffs.

Financial markets appear to be under-pricing the risk of political disruption, with the VIX index (a proxy for investor risk aversion) at the lowest levels since the GFC. Credit spreads are also nearing pre-GFC levels in many regions. Given the numerous global events on the horizon, this pricing seems too low in our view. We believe that the RBNZ will maintain a cautious stance to global risk events in the May MPS.

Statement wording market reaction

The market will once again focus on the tone of the statement and the Bank’s OCR track forecasts. We expect the tone to remain relatively evenly balanced, although the Bank should acknowledge a stronger inflation starting point and weaker NZD. These positive factors are still likely to be caveated with downside risks from the uncertain global environment. Weighing up the balance of data releases we have seen in the past couple of months, we also expect the Bank to move forward its forecast for the timing of an OCR hike – from late 2019 toward early 2019. The timing and extent of interest rate hikes forecast is still likely to be much slower than the OIS market currently has priced in, and probably still slightly later than our view for the first rate hike to occur in late 2018. The OIS market is currently pricing the first rate hike to occur by May 2018 with almost an additional 75bps of hikes by mid-2019. Given the disconnect between market pricing and the RBNZ’s view, the market reaction will depend on just how far the Bank shifts its outlook relative to the February MPS.