Key points:

- The RBNZ’s November 2017 Financial Stability Report (FSR) included an early Christmas present for property hunters, with the RBNZ announcing the loosening of its loan-to-value ratio (LVR) restrictions on mortgage lending from 1 January 2018.

- The Bank is loosening the restrictions for both residential owner-occupier and property investor loans. The RBNZ’s move was motivated by increased confidence that housing market pressures have abated.

- Changes to LVRs are expected to support a gradual recovery in the housing market as we move through the busy summer season.

- The November FSR has limited implications for monetary policy, and we maintain our view that the RBNZ will begin gradually raising the OCR by late 2018.

Summary

Today’s Financial Stability Report (FSR) was highly anticipated following comments by acting RBNZ Governor Grant Spencer at the recent November Monetary Policy Statement (MPS) – and it did not disappoint. The Bank announced that it will loosen loan-to-value ratio (LVR) restrictions on mortgage lending from 1 January 2018. The changes include:

- Banks will be able to lend up to 15% (previously 10%) of all mortgage lending to those with less than a 20% deposit for owner occupied properties.

- For residential property investment loans, banks will be able to lend up to 5% of all lending to those with less than a 35% deposit (previous threshold was a 40% deposit).

We were surprised to see the RBNZ announce these changes so soon. We had thought that the Bank would wait and see how the housing market would develop through the typically busy summer period before loosening these tools. Nevertheless, as we had expected the Bank has chosen to take a prudent approach and loosen LVR’s only gradually. In today’s FSR the RBNZ expressed a high degree of confidence in the current resilience in the financial sector, which has enabled it to loosen macro-prudential policy. In particular, the Bank noted that pressures in the NZ housing market have moderated due to a combination of earlier tightening of LVRs, tighter credit conditions, and a gradual increase in mortgage rates. In addition, there is an expectation that the Government’s housing policy will further reduce pressure in the housing market.

Today’s FSR has limited implications for monetary policy, and adds to our view of a gradual pick-up in the housing market at the start of 2018 as the recent election disruption dissipates. We maintain our view that the RBNZ will hike the OCR late next year as broad inflation pressures pick up quickly due to capacity pressures, a lower exchange rate and higher wage inflation.

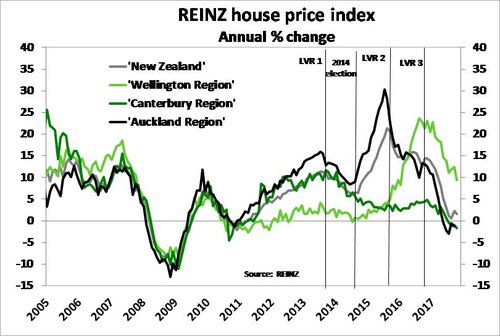

Pressures in the housing market have eased

The main focus of today’s FSR was on the housing market and in particular the announcement of the aforementioned LVR changes. The housing market has cooled quickly since late 2016 and in part due to last year’s tightening of LVR’s on investor-related lending. However, there have been numerous additional factors that have played a role in reducing housing market activity, such as affordability constraints faced by some in the market, a tightening in lending standards by banks, gradually rising mortgage rates, and the uncertainty associated with the September general election. House price appreciation has dropped as a result and, according to REINZ, nationwide house prices were 1.6% yoy higher in October - down from almost 16% yoy in mid-2016. The Auckland market has been a key contributor to this pullback, but other regions are also now following suit. For the RBNZ the slowdown in the housing market has helped to cool credit growth in the banking sector.

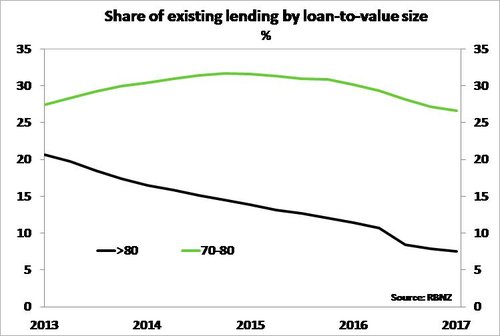

In addition to slowing credit growth, the RBNZ noted a solid improvement in banks’ balance sheets with regard to housing market exposure – improving the resilience in case of a downturn. Since the introduction of LVR’s in late 2013, the share of existing bank lending held by those with less than 20% equity has declined from just over 20% to currently less than 10%. In addition, recent results from banks’ stress tests have shown that the five largest NZ banks are now better positioned to absorb loses in the event of the severe shock to the economy. Finally, the RBNZ noted that the banking sector has tightened lending standards which further helps reduce system risks.

In addition to slowing credit growth, the RBNZ noted a solid improvement in banks’ balance sheets with regard to housing market exposure – improving the resilience in case of a downturn. Since the introduction of LVR’s in late 2013, the share of existing bank lending held by those with less than 20% equity has declined from just over 20% to currently less than 10%. In addition, recent results from banks’ stress tests have shown that the five largest NZ banks are now better positioned to absorb loses in the event of the severe shock to the economy. Finally, the RBNZ noted that the banking sector has tightened lending standards which further helps reduce system risks.

We are expecting the housing market to gradually pick up through the busy summer period, as the disruption from the recent election and change in government dissipates. Today’s announced LVR changes are expected to support our housing market view, but only at the margin given these changes are tweaks to existing policy. The changes to LVRs are expected to have a greater impact on the owner-occupied part of the market, particularly for first home buyers – as the first purchase of a home is often the time when borrowers are most indebted. The loosening around investor LVRs is not expected to have much of an impact on activity in this segment of the market. We expect that policy changes from the Government will likely swamp any support delivered by investor-related LVR changes. Government policy of note includes:

- A change to the bright-line test from 2 to 5 years, over which capital gains can be taxed on sales of investment properties;

- Removal of investors ability to use rental losses created by high levels of borrowing to offset tax liabilities on other income (aka negative gearing);

- and restricting foreign purchases from the existing housing stocks.

The RBNZ noted that it intends to take a cautious approach to further loosening in macro-prudential policy as total household debt remains historically elevated compared to incomes.

Dairy sector indebtedness remains a concern

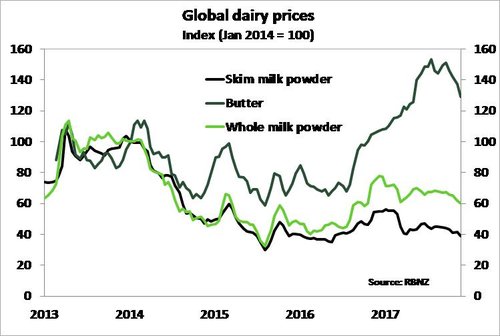

The RBNZ sounded relatively comfortable with recent developments in the dairy sector. Prices have recovered from the lows seen a couple of years ago and there are fewer poorly performing loans. Banks have subsequently reduced provisioning for potential bad debt in the sector. However, the dairy sector remains burdened with elevated levels of debt which makes the sector vulnerable to a sharp downturn. The RBNZ also noted the recent decline in dairy prices in Global Dairy Trade (GDT) auctions (see chart below) could be a risk to the current season.

The RBNZ sounded relatively comfortable with recent developments in the dairy sector. Prices have recovered from the lows seen a couple of years ago and there are fewer poorly performing loans. Banks have subsequently reduced provisioning for potential bad debt in the sector. However, the dairy sector remains burdened with elevated levels of debt which makes the sector vulnerable to a sharp downturn. The RBNZ also noted the recent decline in dairy prices in Global Dairy Trade (GDT) auctions (see chart below) could be a risk to the current season.

Global monetary policy tightening another risk

The RBNZ reiterated its comments from the November MPS, noting that the global economic outlook has improved. However, given local banks’ ongoing reliance on offshore markets as a source of funding, the Bank is always on the lookout for offshore risks. In today’s FSR the RBNZ noted potential threats stemming from the global tightening of monetary policy, tightening of credit in China, and Australia’s significant level of household debt.

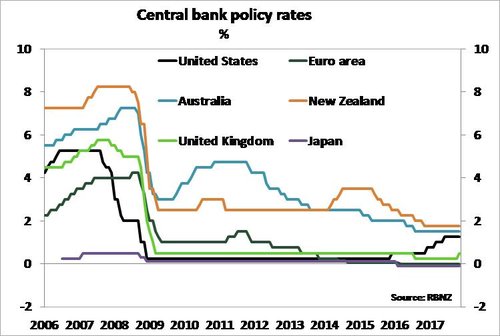

Following the GFC of 2008/09 central banks around the world adopted unorthodox policy stimulus, such as quantitative easing, forward guidance and even negative interest rates in order to simulate activity and boost inflation. A consequent of ultra-accommodative policy has been sustained increases in the value of many asset classes such as property, shares and high-yielding bonds. A number of major central banks, such as the US Federal Reserve, European Central Bank (ECB), Bank of England (BoE) and the Bank of Canada (BoC) are starting to tighten policy by raising interest rates (see chart below) and winding down their asset purchase programmes. Policy tightening is expected to be gradual, but an outside risk could be a correction in international financial markets from policy withdrawal leading to another global recession.

Following the GFC of 2008/09 central banks around the world adopted unorthodox policy stimulus, such as quantitative easing, forward guidance and even negative interest rates in order to simulate activity and boost inflation. A consequent of ultra-accommodative policy has been sustained increases in the value of many asset classes such as property, shares and high-yielding bonds. A number of major central banks, such as the US Federal Reserve, European Central Bank (ECB), Bank of England (BoE) and the Bank of Canada (BoC) are starting to tighten policy by raising interest rates (see chart below) and winding down their asset purchase programmes. Policy tightening is expected to be gradual, but an outside risk could be a correction in international financial markets from policy withdrawal leading to another global recession.

Policy Implications

The FSR's commentary around the housing market ties in with the RBNZ's view highlighted in the November MPS, although implied a greater degree of comfort around the risk of the housing market resurging in months ahead. We don't see any major implications for monetary policy from the changes to LVR settings that were announced today or other commentary contained in the FSR. We maintain our view that the OCR is likely to increase from November 2018 as both non-tradable and tradable inflation pressure increase.

The RBNZ highlighted that it still thinks a debt-to-income limit tool would be a useful addition to the RBNZ's policy toolkit and noted that with its completed consultation on this policy, it is looking to discuss this tool as part of a wider macro-prudential policy review in early 2018. Work on the RBNZ's capital adequacy review for banks (which kicked off earlier this year) continues and is expected to land later next year.