Key Points:

- We expect the RBNZ to leave the official cash rate unchanged at its November Monetary Policy Statement, but the tone and forecasts in the statement itself will be the key focus.

- Data since the RBNZ’s August MPS has generally been on the positive side and we expect to see a slightly more optimistic tone coming through in the statement.

- Financial market pricing for rate hikes has been pushed back and we think there is room for an upside surprise on Thursday.

- We continue to expect the RBNZ to start lifting the OCR from late 2018 in response to rising inflation pressure in the economy.

Summary

We expect the RBNZ to leave the Official Cash rate (OCR) unchanged at 1.75% this week – in line with market expectations. However, given the various data points and some clarity around fiscal policy, the focus will be on the RBNZ’s growth, inflation and OCR forecasts. On the growth front, we expect to see the Bank’s forecasts as largely unchanged once all the components have been weighed up. There is evidence in certain sectors that spare capacity has been depleted, and this adds to the story of rising domestic inflation pressures in years ahead. In addition, the lower exchange rate will start feeding through to tradables inflation in coming quarters – further lifting headline inflation.

We maintain our view that OCR hikes will be required from toward the end of 2018 and expect the Bank to start hiking from its November 2018 MPS. Given the various data (and political) components we have seen since the RBNZ’s last full forecasting round in August, we expect the Bank to pull forward the timing of signalled OCR hikes by three to six months – from kicking off in Q3 2019 previously. At present, financial markets appear to be under-pricing the risk of a more upbeat RBNZ MPS. OIS market pricing has fallen back to a first 25bp rate hike now priced in by February 2019 – compared with November 2018 previously. In addition, both local swap rates and the exchange rate have moved lower. We expect the RBNZ will be cautious about removing its long-held commentary suggesting that “a lower New Zealand dollar is needed”, but will have to acknowledge the sharp decline in the exchange rate as helpful in getting inflation back to target.

While we note that there are many moving parts at present (change in Governor, review of the RBNZ act, further details on fiscal policy, international monetary and political policies), the underlying data in NZ is robust enough to warrant a more optimistic tone from the RBNZ this week. While these positives are likely to remain couched with uncertainty, we do expect to see the RBNZ’s OCR forecasts pulled forward in response to recent data developments – in particular the lower exchange rate.

Key developments

Since the RBNZ completed its last full forecasting round in August, we have seen several pieces of information that, in our view, support a more optimistic outlook for inflation compared with the Bank’s previous forecasts. We discuss some of the key developments below.

New government/fiscal policy: The biggest uncertainty heading into this week’s MPS is how the RBNZ will account for proposed changes in fiscal policy under a new government. The Bank had included National’s income tax changes and family package in its last set of forecasts, adding a boost to growth from increased fiscal stimulus. Our expectation is that Labour’s policies will be more fiscally stimulatory than National’s tax reforms, although the exact details remain light. So how does the RBNZ update their view? We expect them to include the Families Package (which replaces National’s tax changes) and minimum wage increases, plus take into consideration changes in migration policy and the plans to build 100,000 home over the next ten years. Labour’s Families Package alone is worth less than National’s proposed changes, but the expectation is that the additional savings will be spent directly on housing, health and education. Direct spending tends to be more stimulatory for the economy (because for tax cuts – especially a higher income levels – people to tend to save a percentage of it rather than it all getting spent). Overall, we expect to see more fiscal stimulus pass through to the economy over the next few years.

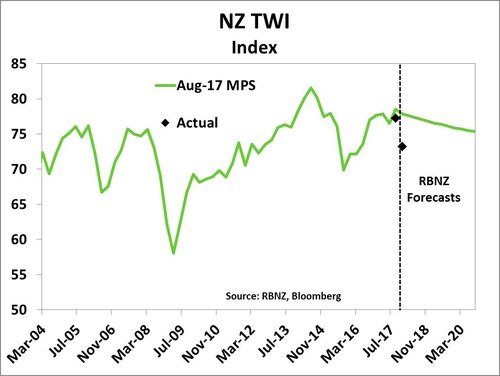

Lower exchange rate: The significant decline in the NZ dollar against most its major trading partners has seen the NZ trade-weighted index (TWI) decline to around 73.50 – 4.5% lower than the RBNZ’s forecasts for the December quarter (see chart above). This drop has been in part been driven by markets response to election outcome uncertainty and then the announcement of a Labour-led government. In addition, the prospect of a dual mandate for the RBNZ seems to have caused some expectation of a longer period of accommodative monetary policy. If the currency remains at around current levels (or falls further) this will feed through to a lower cost of imported goods. We have already seen petrol prices move higher in response to the declining currency, but it typically takes 3-6 months for importers to adjust their selling prices. Hence the lower currency should start to feed through into higher tradables inflation toward the end of 2017/beginning of 2018. In addition, a lower currency makes our exports more attractive in international markets – which should provide a boost to local incomes from higher export demand and revenues.

Lower exchange rate: The significant decline in the NZ dollar against most its major trading partners has seen the NZ trade-weighted index (TWI) decline to around 73.50 – 4.5% lower than the RBNZ’s forecasts for the December quarter (see chart above). This drop has been in part been driven by markets response to election outcome uncertainty and then the announcement of a Labour-led government. In addition, the prospect of a dual mandate for the RBNZ seems to have caused some expectation of a longer period of accommodative monetary policy. If the currency remains at around current levels (or falls further) this will feed through to a lower cost of imported goods. We have already seen petrol prices move higher in response to the declining currency, but it typically takes 3-6 months for importers to adjust their selling prices. Hence the lower currency should start to feed through into higher tradables inflation toward the end of 2017/beginning of 2018. In addition, a lower currency makes our exports more attractive in international markets – which should provide a boost to local incomes from higher export demand and revenues.

Growth outlook: In the August MPS, the RBNZ was expecting domestic growth to rise to a pace of 3.8% yoy at the start of 2018, but this looks doubtful based on our projections. The Bank hinted at a softer growth outlook in its September OCR Review, noting that “growth is projected to maintain its current pace going forward, supported by accommodative monetary policy, population growth, elevated terms of trade, and fiscal stimulus”. We expect growth of around 3-3.5% yoy over year ahead. There are signs of significant capacity pressures (see below) that are limiting the construction sector from growing at a faster pace, despite a strong pipeline of demand. The RBNZ included a scenario where residential investment is restricted by funding constraints and remains flat over the projection period. Given the sizeable amount of government housing investment planned, we doubt that this scenario will end up eventuating, but there are risks that with limited capacity, that government spending replaces private investment rather than significantly adding to the overall volume of work. The dynamics of how this plays out in the next few years is a key risk to our view.

Domestic capacity pressure: There are signs of significant capacity pressures in certain industries in New Zealand – the construction and tourism industries in particular are feeling the pinch. With supply of materials, and workers constrained, we expect to see prices in these sectors continue to move higher in the year ahead - particularly once additional government residential investment and infrastructure projects are added into the mix. For the domestic inflation outlook, a lack of spare capacity and growth above its potential rate are expected to see non-tradables inflation continue to rise from its current pace of 2.6% yoy.

CPI inflation: September quarter CPI data showed that inflation was stronger than the RBNZ had anticipated, rising at a pace of 1.9% yoy compared with the Bank’s 1.7% yoy forecast. The underlying numbers showed that a great deal of this pressure remains concentrated in housing-related sectors but it gives higher starting point for the Bank to feed into its forecasts. Looking at the split shows that a greater contribution to overall inflation came from domestic (non-tradable) price increases (which are the RBNZ primary focus) over the past year than from tradables inflation. In addition, the sharp decline in the NZ dollar is expected to boost the price of tradables goods in coming quarters. The RBNZ had previously forecast the CPI inflation would drop down to 0.7% yoy in March 2018; based on our forecasts we see inflation pulling back to around 1.4% yoy and hence the risk that inflation expectations are pulled lower has been reduced.

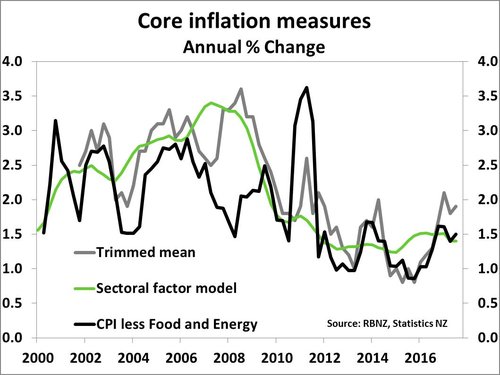

Core inflation: Recent research and commentary from the RBNZ has placed increasing importance on measures of core inflation as a true indicator of inflation pressure in the economy. The RBNZ’s sectoral measure of inflation remains relatively subdued at 1.4% yoy, while CPI inflation (less food, household energy and vehicle fuel) is tracking at 1.5% yoy. The trimmed mean measure of inflation from Statistics NZ has ticked up over the past quarter.

Core inflation: Recent research and commentary from the RBNZ has placed increasing importance on measures of core inflation as a true indicator of inflation pressure in the economy. The RBNZ’s sectoral measure of inflation remains relatively subdued at 1.4% yoy, while CPI inflation (less food, household energy and vehicle fuel) is tracking at 1.5% yoy. The trimmed mean measure of inflation from Statistics NZ has ticked up over the past quarter.

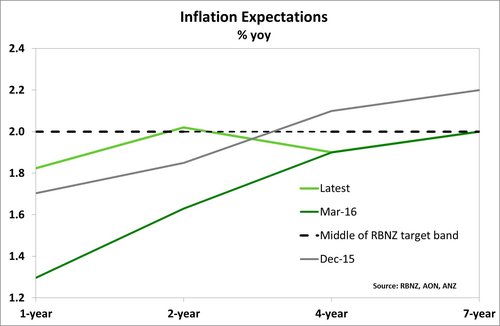

Inflation expectations: The RBNZ recently released a note discussing how past inflation outturns are having a greater impact on businesses price setting intentions. With headline CPI now up at 1.9% yoy, this should help steady inflation expectations at around 2%. In addition, we suspect that the RBNZ was quite concerned that if inflation dropped down below 1% again (as they had forecast for the March 2018 quarter) then inflation expectations would shift lower again. As discussed above however, we expect inflation to hold up at a much higher level through the start of next year, and hence the risk that expectations shift from around 2% has been reduced. Short-term inflation expectations have now moved higher than they were prior to the RBNZ’s final round of OCR cuts that started following a sharp decline in expectations between late 2015 and early 2016 (see chart below), while long-term expectations remain comfortably anchored at around 2% yoy.

Business confidence: Business confidence has taken a political hit in recent months. The ANZ Business confidence index for October showed that a net 10% of businesses expect economic conditions to worsen in the year ahead. However, a net 22% of firms still felt positive about their own prospects. Most of the survey results were submitted before the make-up of the new government was announced and hence that uncertainty was likely to be casting a shadow on the outlook. As there becomes increasing clarity around the new government’s policies, we expect to see headline business confidence improve again.

Labour market tightening/wage pressure: In the September quarter, the unemployment rate dropped to the lowest level since the end of 2008 at 4.6%. This new low was reached despite a sharp lift in the participation rate – to a new record high of 71.1% - as the number of people in employment increased 4.3% over the past year. The NZ labour market has continued to easily absorb the strong population growth we have seen in NZ. The tightening in the labour market indicates that the RBNZ’s labour utilisation composite index (LUCI) should have increased further – signalling reduced spare capacity in the economy and rising domestic inflation pressure. While wage growth has been a missing component of the generally positive labour market story, we expect that the new government’s decision to raise the minimum wage will spill over into more general wage (and price) inflation in coming years. In addition, a reduction in net migration (see below) could firms competing for a smaller pool of available workers which in turn would also lift wages.

Net migration: The latest set of migration data shows that net migration between NZ and Australia has turned into a small net outflow as the labour market in Australia has improved recently. With the new government, looking at tightening up on student visa requirements, we expect to see a reduction in students entering the country and work visas as a share of overall arrivals increase. This tends to be more stimulatory from an inflationary viewpoint as an older long-term arrival tends to consumer more. Overall, the new government is looking at reducing net migration numbers from the current rate of 71,000 toward 40,000-50,000. The pace and way in which they do so will have an impact on the NZ economy. The RBNZ already had migration forecast to pullback over the next few years anyway and we expect to see net migration remain relatively elevated in coming years – adding to demand in the economy.

Solid global growth/tightening in monetary policy: Since the August MPS, both the IMF and OECD have slightly revised up their outlooks for global economic growth over the next couple of years, and inflation outturns have proved solid in the US and UK and stable in Europe. The RBNZ noted in its August MPS that a slow recovery in global inflation was one of the key underlying assumptions of its forecasts. If global inflation turns out stronger than the Bank forecast, then it noted an additional 75bps worth of rate hikes would be required over the next few years in response to a lower NZ TWI, rising import costs and tighter global monetary policy. The US Federal reserve is widely expected (almost 95% priced) to lift the Fed Funds rate again in November, taking its policy rate range to 1.25-1.50% - further narrowing the interest rate differential between NZ and the US. If the Fed delivers on its current policy projections over 2018, then the Fed policy rate will be higher than the official cash rate by mid-2018. This is likely to put further downwards pressure on the NZD/USD and lift tradables inflation and boost exports. However, our neighbours across the ditch are not faring quite as well, with the expectation that monetary policy will remain on hold with the cash rate at 1.50% until at least the end of 2018.

Pulling all of the above together, we remain comfortable with our view that the RBNZ is likely to start lifting the cash rate from late 2018. However, we suspect that it is a little bit too early for the RBNZ to signal that view; there remains some uncertainty around the implementation and execution of various government policies in particular. The key risks to our view in the near-term are around the sustainability of the upswing in the global environment.

A few words on housing

The New Zealand housing market has continued to cool, with sales 26% lower in September compared with a year prior. Prices have shown some tentative signs of stabilisation in the past couple of months. In Auckland, prices are now essentially flat on a year-on-year basis, while inventory levels are elevated. However, there remains an underlying shortage of houses in our biggest city that we expect to stop prices experiencing a sharp decline in the near future (see our recent special housing market piece here for more details).

Statement wording and market reaction

We expect to see the wording in the opening paragraph remain relatively similar to the September OCR Review statement in terms of commentary on global growth, the domestic economy and inflation. In addition, we expect the Bank to leave its closely scrutinised final paragraph unchanged, stating that “Monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly.”

The main change in the one-page statement is expected to be around the commentary relating to the exchange rate. Given the large decline in the past couple of months, we expect the Bank to acknowledge that the lower currency will help rebalance the economy, but that any rebound could pose a risk to the Bank’s outlook for the economy.

Market positioning

In the wake of the announcement of the new Labour-led government, the OIS market has actually pushed back the expected timing for a rate hike from the RBNZ – from November 2018 back to February 2019. Given some of the policy announcements we have seen to date, and the nascent inflation pressure in the economy, we think this is counter-intuitive. In addition, the NZ TWI has fallen substantially in recent months due to domestic uncertainty and more positive sentiment in major trading-partner economies. We expect to see a small rebound in the NZ dollar if the RBNZ releases a statement in-line with our expectations.