Key Points:

- The RBNZ is expected to leave the OCR unchanged at 1.75% at this week’s September OCR Review.

- While there have been a few pieces of interesting data since the August MPS, we expect this week’s review to pass without much impact.

- Political matters – both domestic and international – are more likely to take centre stage this week.

- We expect to see little change in the tone from the RBNZ, with the bulk of the policy statement unchanged.

- We maintain our view that the RBNZ will leave the OCR unchanged until the end of 2018, before gradually hiking interest rates.

Summary

Since the RBNZ’s last Monetary Policy Statement (MPS) in August, net-net there has been little data of note to warrant a shift in our view and we suspect the RBNZ will be of a similar mind-set. In addition, political uncertainty remains and it will take time before a new government is formed and its fiscal policies and the flow-on effects to the economy become clear. Given this environment, we expect the Bank will remain happy to sit on its hands and fully assess the economic outlook at its next MPS on November 9. The change of Governor, as Graeme Wheeler officially steps down on September 26 and Grant Spencer assumes an interim role for six months, is not expected to have an impact on the outlook for monetary policy. We expect it will be business as usual with Spencer already closely aligned with current policy settings and unlikely to want to rock the boat.

As such, we expect the RBNZ to leave the cash rate unchanged on Thursday at 1.75% and maintain a neutral tone in its accompanying statement. We expect that the closely-watched final paragraph of the release will stay the same, suggesting that “Monetary policy will remain accommodative for a considerable period”.

Growth on track

The New Zealand economy continues to tick along at a moderate pace of growth. Economic growth expanded by 2.5% over the year to June 2017 – just marginally lower than the RBNZ’s forecast for growth of 2.6% yoy. What is more important however, is the outlook for GDP growth over coming years. The composition of recent growth has moved away from construction-led, to being driven by strong export commodity prices, a buoyant tourism industry, domestic spending and relatively low interest rates. In addition, no matter whom ends up forming a coalition government in the weeks ahead, the proposed policies from the two major parties are expected to provide a fiscal boost over the next couple of years.

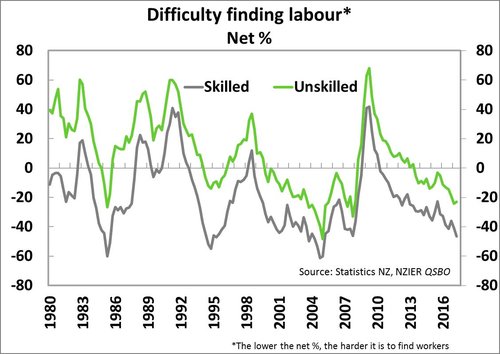

In our view, one of the biggest limiting factors on the economy is coming from capacity constraints rather than a lack of demand. As such, we are starting to question whether potential output will end up being lower in coming years than RBNZ’s estimate of 2.8%. If potential growth is limited by a lack of skilled workers and availability of resources, then this is likely to see domestic inflation pressure build more quickly than in the RBNZ’s central scenario.

Inflation outlook bumpy but trending higher

Inflation is currently running just below the mid-point of the RBNZ’s 1-3% target inflation range, at 1.7% yoy currently. However, inflation isn’t expected to remain there, with the RBNZ forecasting that inflation will pull back to 0.9% yoy at the start of 2018. This is lower than our own forecasts (and the consensus view) which suggest inflation could fall to 1.2% yoy in March 2018 at the lowest. Beyond there we expect to see inflation move back toward 2% in response to growing capacity pressures and a declining NZ dollar.

Global monetary policy tightening, helping ease pressure on the NZD

In recent months we have seen increasing rhetoric from global central banks around the desire for tighter monetary policy settings. In addition, it now appears that the global economy is experiencing a synchronised upswing in activity – although there remains concern around how sustainable this growth is. The OECD revised up its forecasts for economic growth in its interim Economic Outlook released last week. In response to this more positive outlook and gradually increasing inflation rates, we are now seeing several major central banks move toward tightening monetary policy settings.

The Bank of Canada has continued to lift its overnight rate to 1% - up from 0.5% at the start of July. The latest policy decision from the Bank of England (BoE) saw the board vote 5-2 in favour of leaving interest rates unchanged at 0.25%, but the accompanying statement was more upbeat. BoE Governor, Mark Carney, noted that spare capacity in the economy has been used up more quickly than anticipated, which means that some policy withdrawal could be warranted in coming months. US Federal Reserve officials continue to expect another Fed Funds rate hike before the end of this year as well as suggesting three rate hikes over 2018. If delivered, this would take the US policy rate well above the OCR in NZ – which hasn’t been seen since the early 2000’s. Closer to home, the OIS market is now pricing a 60% chance of a rate hike from the Reserve Bank of Australia (RBA) by June 2018 with the median analyst expectation for a 25bp rate hike at the end of 2018.

The Bank of Canada has continued to lift its overnight rate to 1% - up from 0.5% at the start of July. The latest policy decision from the Bank of England (BoE) saw the board vote 5-2 in favour of leaving interest rates unchanged at 0.25%, but the accompanying statement was more upbeat. BoE Governor, Mark Carney, noted that spare capacity in the economy has been used up more quickly than anticipated, which means that some policy withdrawal could be warranted in coming months. US Federal Reserve officials continue to expect another Fed Funds rate hike before the end of this year as well as suggesting three rate hikes over 2018. If delivered, this would take the US policy rate well above the OCR in NZ – which hasn’t been seen since the early 2000’s. Closer to home, the OIS market is now pricing a 60% chance of a rate hike from the Reserve Bank of Australia (RBA) by June 2018 with the median analyst expectation for a 25bp rate hike at the end of 2018.

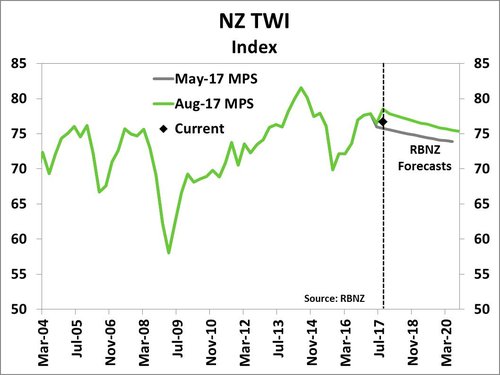

Rising interest rates globally, combined with our expectation that there is limited further upside in terms of our major export commodity prices, should see the NZ TWI gradually decline from current levels. Since the August MPS, the NZ TWI has declined about 1%. Over the September quarter to date, the TWI has averaged about 77.3 –1.5% lower than the RBNZ’s forecast of 78.5 over the quarter. If the NZ dollar continues to ease against our major trading partner countries then that will help boost tradables inflation by more than the RBNZ is currently forecasting.

Big question marks over housing

As the RBNZ highlighted in its August MPS, there remains a lot of uncertainty around whether house price appreciation will remain flat or in some areas continue to decline in coming months. House sales are down over 20% across the country compared to this time last year. However, this reflects a similar pattern to that seen prior to the 2014 election and we expect that sales activity will pick up again in coming months and over the busy summer season. The August REINZ housing market data hinted at a bottoming out in the decline in sales and prices that we have seen in Auckland in the past year. Given Auckland continues to face a supply/demand imbalance and the threat of capital gains tax has at very least been postponed for three years, there is likely to be floor under how much further prices can fall. There is both anecdotal and data-based evidence that first home buyers have been given more opportunities by the RBNZ’s tightening of LVR restrictions for property investors at the end of last year.

On the supply side, construction growth has slowed to a standstill. While funding constraints are certainly having an impact on the development industry, we are also seeing significant capacity constraints, particular in terms of availability of skilled staff. Ensuring we have enough skilled workers will be an area of attention for the incoming government, particularly given both parties plans to boost spending on infrastructure and residential investment.