Key Points

- The labour market tightened further in the September quarter, with the unemployment rate falling to 4.6%.

- A fall in the unemployment rate was helped by a 2.2% qoq surge in employment.

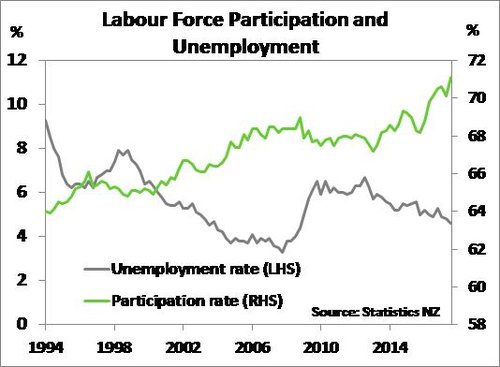

- A jump in the participation rate to a new all-time high of 71.1% stopped the unemployment rate from falling further.

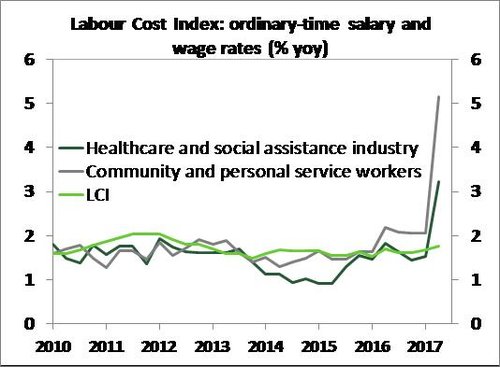

- While wage growth picked up, in large part due to the pay-equity deal for care and support workers, underlying wage growth remained modest.

- Nevertheless, we see wage growth rising as the labour market continues to tighten and government policy changes such as increases to the minimum wage come into effect.

- Today’s labour market report supports our view that inflation is likely to rise faster than the RBNZ is forecasting. We maintain our view that the RBNZ will begin OCR hikes in late 2018 – almost a year earlier than the RBNZ has signalled.

Summary

Today’s September quarter labour market report (which includes the Household Labour Force Survey (HLFS), Quarterly Employment Survey, and the Labour Cost Index (LCI)) showed a labour market that continues to tighten. The unemployment rate fell to 4.6%, the lowest in 9 years and slightly lower than the 4.7% we and the market had expected. A lower unemployment rate was driven by a 56,000 or 2.2% qoq jump in employment, compared to a 0.1% qoq drop in June. On an annual basis employment was 4.3% yoy higher and up impressively from a 3.1% yoy recorded in the June quarter. The data showed that despite the growing uncertainty over the third quarter, as we headed toward a general election, firms continued to hire regardless. This backs-up recent surveys of business confidence that have shown that despite firms being more pessimistic regarding the outlook for the general economy, they are getting on with business. Keeping the unemployment rate from falling further was a surprisingly strong rebound in the participation rate to a new all-time high of 71.1%.

As expected, wage growth lifted in the third quarter, in large part due to the well-publicised pay-equity deal for care and support workers, that came into effect on 1 July. However, excluding the pay deal the underlying Labour Cost Index (LCI) continued to grow at a similar modest pace – 1.6% yoy. Nevertheless, there is growing evidence that wage inflation will pick up over the year ahead as the labour market continues to tighten.

Today’s data adds to other indicators that suggest inflation will pick-up faster than the RBNZ had been expecting. For instance, the trade-weighted exchange rate is averaging around 4% below the RBNZ’s August Monetary Policy Statement (MPS) forecast over Q4 to date – adding to future tradables inflation. In addition domestic capacity constraints, further helped by the ongoing tightening labour market, remain elevated. As a result we maintain our view that the RBNZ will begin hiking interest rates from late 2018 – almost a year earlier than the RBNZ has signalled. At next week’s November MPS we expect to see the RBNZ bring forward its OCR projections to imply gradual OCR rate hikes from early 2019 compared to mid-2019 previously.

The unemployment rate falls as employment surges

There was a larger-than-expected drop in the unemployment rate to 4.6% in the September quarter, which continued the persistent decline seen since late 2012 (see chart below). A 2.2% surge in employment, or an addition 56,000 people in employment, was a key reason for the fall in the unemployment rate. The unemployment rate could have fallen further if it wasn’t for a 1% point jump in the labour force participation rate to a new all-time high of 71.1%. We had expected a strong rise in the participation rate, partly due to pay back from a surprise fall seen in June and given recent solid net migration numbers adding new eager workers to NZ's labour force.

The large jump in employment in the HLFS was at odds with the QES measure, which showed that over the quarter full-time equivalent employees and total filled jobs increased by much more modest 0.8% qoq and 0.2% qoq respectively. Statistics NZ noted that the difference in coverage between the HLFS and QES can produce these discrepancies, with certain industries (such as agriculture) being excluded from the QES. The QES still looked respectable however, as shown by the 0.8% qoq rise in average weekly paid hours - a loose proxy for GDP growth over the quarter - to take the annual rise in paid hours to 3%.

Pay deal behind rise in wage growth

A key feature of September quarter labour market figures was a jump in wage growth. The Labour Cost Index (LCI), our preferred measure of pure wage inflation, increased to 1.9% yoy. As had been expected, the rise in wage growth was largely the result of the widely publicised pay settlement for around 55,000 aged and disability care workers that came into effect on 1 July. This was evident in the data, as the rise in wages was felt in the private sector where the majority of the pay-equity deal recipients are captured. Private sector LCI (excluding overtime) was 1.9% yoy higher, up from 1.6% yoy in June, and compares to a 1.5% yoy increase in the public sector LCI. At an industry and occupational level we saw solid wage increases in the healthcare sector (+3.2% yoy) and personal service workers (+5.1% yoy) (see chart below). The QES measure of wage growth, average hourly earnings, also experienced a notable rise in the September quarter, up 1.2% qoq – the highest quarterly rise in three years.

Without the pay deal, Statistics NZ noted that the headline LCI would have increased by 1.6% yoy – which is around rates of growth seen in recent quarters. Underlying wage growth has remained fairly muted for a number of quarters now, but there are growing signs that underlying wage growth is set to rise. While the aged and disability care workers pay deal is at this stage a one-off development for wage growth, there is the possibility that on the back of this deal other workers in similar industries will look to negotiate for higher pay. In addition, the new Government has revealed its intention to lift the minimum wage to $16.50/hr by next April and then steadily to $20/hr by April 2021. The steady rise in the minimum wage over the coming years is expected to add to wage growth. Finally, a tightening labour market will add to wage inflation as firms find it increasing difficult to fill roles and offer higher wages to attract staff.

Policy implications

Today’s robust set of labour market figures add to other recent drivers of inflation pressure in the NZ economy. For instance, the currency has steadily declined since the September general election with the TWI now averaging around 4% below the RBNZ's August MPS forecast over fourth quarter to date. In addition, domestic capacity constraints remain elevated, and the ongoing tightening of the labour market will only contribute to this. We see the combination of a weaker TWI track and ongoing domestic capacity constraints indicating that inflation will steadily rise over 2018 and necessitate eventual OCR hikes from late 2018.

Based on recent developments, we expect that the RBNZ will revise up its inflation forecast at next week’s November MPS. Moreover, we see the RBNZ bringing forward its OCR projections to imply OCR hikes from early 2019 compared to mid-2019 previously. More detail on our view will be provided in our MPS preview released early next week.

Market reaction

There was an immediate market response to this morning's labour market report. The NZ dollar initially spiked 50 points to $0.6890, and has since settled around the $0.6900 mark. Wholesale interest rates also perked up, with the 2-year swap rate up a few basis points on yesterday's close to 2.17%. Similarly the 5-year swap rate rose a few points following the release to 2.64%.