A covid vaccine is a game changer

- Despite covid infections spiking across most of the world, the outlook is a little brighter. News of advanced vaccines has buoyed confidence.

- Locally, the impact of previous lockdowns and border closures was not as bad as initially feared. And the housing market is on a tear!

- We remain wary of the economic impact of prolonged border closures. And NZ’s border is unlikely to fully reopen until 2022. But geez, we feel a lot better about the world.

A brighter shade of pale.

The economic outlook is less doom and gloom than initially feared. The IMF has upgraded its 2020 global growth forecast from -5% to -4%. A 1%pt rise is massive on a global scale. And it is a massive change in mindset. Activity indicators are positive. And China is leading the expansion. There’s no denying the hand of policy. Outsized fiscal and monetary support have cushioned the blow. Just like a brand-new memory foam pillow, things are taking shape. Over $12 trillion in fiscal support has been injected globally through business loans, wage support and cash grants. And monetary policy stands to win best supporting actor. Interest rates have been slashed, liquidity injected, and billions of assets purchased. And financial markets have lapped it up.

But let’s not get ahead of ourselves. The global recession is still the deepest since the Great Depression. And the journey to full recovery is still long and arduous. Output is not expected to reach 2019 levels until late in 2021. And there is a growing divergence between advanced and developing countries. Growth forecasts have been upgraded for advanced countries and China. But prospects have worsened in many developing countries where covid cases are rising rapidly. India’s economy, for example, is expected to contract 10% this year, a significant downgrade to earlier forecasts. And no recovery is guaranteed so long as the pandemic continues. To date 64million cases have been confirmed worldwide. The US, India and Brazil currently top the highest number of cases. Social distancing will likely persist until the threat of the virus is eliminated. We expect NZ’s border will only reopen very slowly next year and will not fully reopen until 2022 at the earliest.

95% is still short.

NZ has been held up as an exemplar for strictness in social distancing, the size of policy responses, and the success in keeping covid at bay. And Kiwi export prices have been remarkably resilient this year. Nevertheless, the Kiwi economy is far from unscathed. Until we get hold of a potent vaccine, tourism and education will be without foreigners. So, while we celebrate our return to 95% capacity, we must also consider the starvation of the 5%.

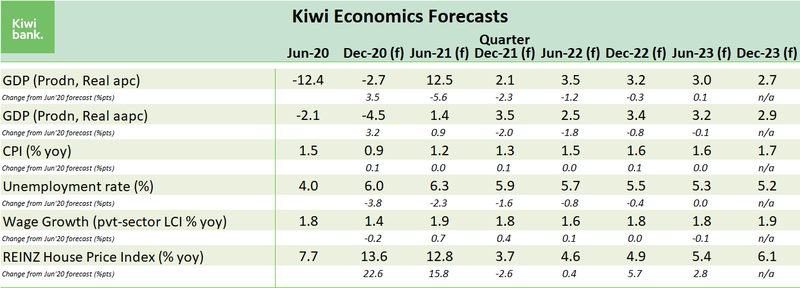

Our lockdowns and closed borders led to significant job losses and business closures. GDP contracted 12.2% in the second quarter. But the economy bounced back and should have recorded a strong rebound in the third quarter (numbers released on December 17). Household spending lead the rebound with consumers unleashing pent-up demand out of lockdown. As seen in Kiwibank’s own electronic card transactions data (see our latest Household Spending Tracker report). And despite the disruption caused by Auckland’s level-3 lockdown in August, we’re likely to see GDP jump 12% in the third quarter.

The Summer months will be challenging though. Closed borders pose both demand and supply disruptions. Foreign tourist and student numbers typically surge in summer. Last winter may have provided a false sense of security for parts of NZ’s tourism sector. Kiwi, unable to travel overseas, flocked to tourist hotspots around Aotearoa in droves. But even a swell of adventurous locals in the coming months won’t be enough to offset the usual hordes of international visitors. We’re still in a demand shock.

The Summer months will be challenging though. Closed borders pose both demand and supply disruptions. Foreign tourist and student numbers typically surge in summer. Last winter may have provided a false sense of security for parts of NZ’s tourism sector. Kiwi, unable to travel overseas, flocked to tourist hotspots around Aotearoa in droves. But even a swell of adventurous locals in the coming months won’t be enough to offset the usual hordes of international visitors. We’re still in a demand shock.

On the supply side, visitor arrivals also supply a valuable source of workers for many industries including tourism itself. Moreover, primary producers are reliant on summer arrivals to help pick and pack produce at the peak of the growing season. The challenge posed by the lack of arrivals will weigh heavily on growth. We are forecasting a modest 0.4% contraction in GDP in the March quarter as a result.

On the supply side, visitor arrivals also supply a valuable source of workers for many industries including tourism itself. Moreover, primary producers are reliant on summer arrivals to help pick and pack produce at the peak of the growing season. The challenge posed by the lack of arrivals will weigh heavily on growth. We are forecasting a modest 0.4% contraction in GDP in the March quarter as a result.

Barring another major outbreak, the economy is expected to recover over 2021. Policy support, such as the Government’s infrastructure programme, and even lower interest rates, will ensure growth will remain above trend next year. News of encouraging vaccine trial results has been warmly welcomed and is a light at the end of the covid tunnel. However, it’s easy to get carried away with vaccine news. The timeframe for regulatory approval, production, and distribution is long. Full coverage from covid in NZ could still be years away. In the meantime, our border will remain closed and won’t fully reopened until 2022 at the earliest in our view. Following a 4.5% contraction in 2020 we are forecasting GDP to rebound 3.5% over 2021. However, despite a rebound next year, Kiwi economic activity is not forecast to reach pre-covid levels until early 2022. And the return to full employment will take even longer.

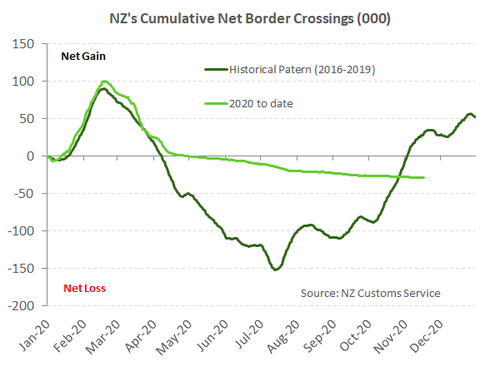

The labour market has mirrored the better-than-expected rebound in economic activity. The unemployment rate did jump in the third quarter to 5.3%. And Q3 is certainly not the peak. We are forecasting a peak of 6.5% in early next year, well below the double digit rate thought possible during the height of the crisis. The challenging summer months being a key reason for the deteriorating labour market.

Growing spare capacity in the labour market will weigh on wage growth. Private sector wage inflation should bottom out early next year. The Government’s plan to lift the minimum wage to $20/hr from next April is expected to cause a temporary boost in wage growth. Beyond that hike, wage inflation is expected to recover as the labour market slowly strengthens but is unlikely return to its pre-covid peak of 2.4%.

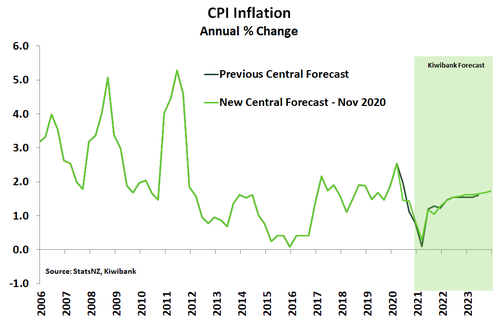

Like wage inflation, general inflation is expected to bottom out next year. We are forecasting CPI inflation to trough at 0.3%yoy at the start of 2021 before gradually recovering. Covid has sucked out any hints of domestic inflation pressure. Non-tradables (or domestic) inflation has already fallen quickly since the March 2020 quarter. A highly uncertain trading environment makes it difficult to pass on any cost increases. The policy response to date, and more expected ahead, should help to push non-tradables inflation back to pre-covid rates by the end of 2023. A strengthening  NZ dollar over the forecast horizon however, will drag on imported, tradables inflation. Overall, CPI inflation is forecast to slowly lift toward the RBNZ’s 2% target midpoint. But it is predicted to be a sluggish rise, only reaching 1.7%yoy by the end of 2023.

NZ dollar over the forecast horizon however, will drag on imported, tradables inflation. Overall, CPI inflation is forecast to slowly lift toward the RBNZ’s 2% target midpoint. But it is predicted to be a sluggish rise, only reaching 1.7%yoy by the end of 2023.

Like a red rag to a raging bull.

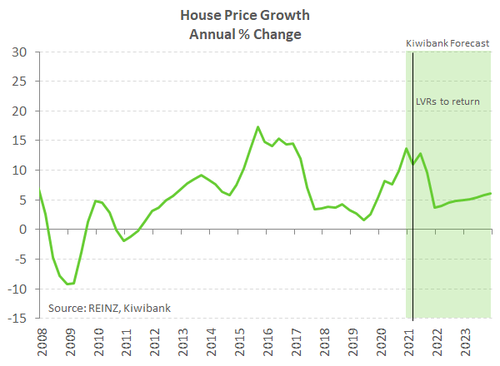

The NZ housing market truly epitomises the astounding year 2020 has been. Even in the face of the sharpest recession in the last 100 years, house prices are surging, and sales activity has hit multi-year highs. Policy stimulus has been a key driver. Record low mortgage rates and the removal of LVR restrictions are notable examples. But NZ carried a significant housing shortage into the crisis too.

We no longer expect house prices to fall this year or next, and double-digit price gains are predicted well into 2021. However, house price growth is expected to slow from around the middle of next year. The RBNZ is to reinstate LVR restrictions in March, and banks will rein in lending from now. LVR restrictions will take the investor-related froth off the top of the market. Moreover, a closed border means population growth is slowing. House price growth should slow to more modest 5-6%yoy pace from the second half of 2021. If not, we’d expect to see harsher LVR restrictions come into play to cool the housing market.

Financial markets end the year higher on vaccine hopes.

Asset prices have been pumped higher. Equity markets have been propelled higher by record low interest rates, primed with quantitative easing, and a step change in fiscal expansion. It seems incredible to see global equity markets smashing through record highs, as the world locks down and the spread of the virus continues. But such is the power of extraordinary fiscal and monetary policy.

In a world of covid lockdowns, NZ looks like the safest of havens. We simply look better than most. And in financial markets, it’s a relative game.

Despite falling 30% over March, the NZX will end 2020 ~10% higher. That’s simply amazing when you consider where we were in March. And a similar story can be told for other assets.

The yield on the Kiwi 2-year swap rate (the rate banks use to hedge 2-year fixed mortgage rates) started 2020 at 1.26%. The 2-year fell to just 0.1% in May, at the height of the pandemic. After stabilising around 0.25% over the middle of the year, the RBNZ upped the ante on negative interest rates. The RBNZ directed market traders to price in negative rates. And the 2-year swap rate traded in negative territory for the first time in history in the third quarter. But then we started to hear of vaccines coming, soon. And we read a letter addressed to the RBNZ from Finance Minister Grant Robertson. The Government was responding to the growing cries for action in the rampantly rising housing market. Traders headed for the exits, and Kiwi rates rose. The 2-year rate looks set to finish the year around cash, at 0.25%. What a ride… Over the year, mortgage rates headed south and never looked like turning back. Over next year, we expect the 2-year swap rate to fall initially, stabilise, and end the year slightly higher. Mortgage rates are likely to remain near record lows into 2022. RBNZ rate rises will remain a fantasy in 2021.

The Kiwi currency was not to be outdone by the volatility in rates markets. The Kiwi currency is not flightless. In fact, the little Kiwi flier is an aerial acrobat, flying more like a pīwakawaka (fantail) in pursuit of insects. The beautifully volatile bird set flight at 67c into 2020. As the world was engulfed by covid panic, the Kiwi nosedived to a low of 54.7c in March, a 20% decline. But that was simply a playful manoeuvre. The bird staged a miraculous recovery, and was fluttering around 67c over the middle of the year. Of course, our forecast for December 2020, made this time last year, was 67c. And never one to adhere to forecasts, the bird looks set to finish the year in the 70s (currently 0.7065). During every global recession, the Kiwi nosedives, and struggles to recover. So it seems fitting that the Kiwi flyer defies history, logic, and economic theory, to end the year materially higher. You have to be completely unhinged to pretend to predict where the Kiwi flyer will go from here. But we’d say higher still next year. Let’s say 75c by December 2021. We have great un-conviction in our forecast. So realistically, the Kiwi could end next year anywhere between 50c and 90c.