“Don't look so worried you know, There ain't no hurry, 'Cause life's supposed to ebb and flow” Shihad

- Financial markets, globally, have been pacified by copious amounts of QE. And fiscal policy has joined the fray. Few do it better than NZ.

- Extraordinary measures are designed to boost asset values, including equities. But the risks remain heavily titled to the downside.

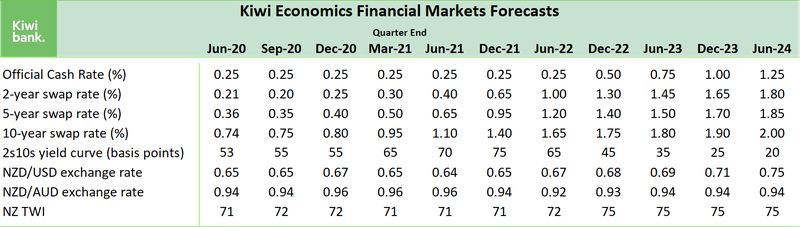

- We lower our interest rate forecasts and tweak our currency call. We expect the RBNZ to eventually double their QE program. And term lending to banks is the next (best) policy off the shelf.

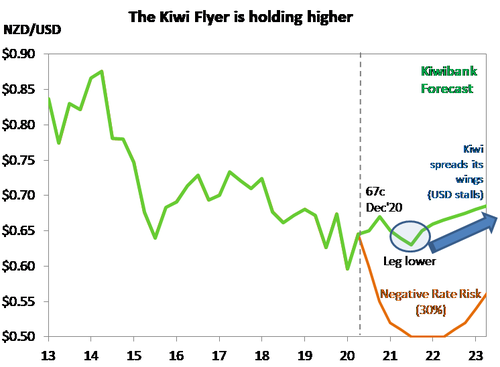

The pandemic is accelerating offshore. The economic cost of the covid crisis is climbing. And New Zealand is a small, seemingly pristine, Oasis of elimination. Although our nation remains vulnerable to imported cases. Our relative success, and resurgence in activity out of lockdown enabled us to upgrade our economic forecasts – see “Icy Climb”. Our current forecast of 67c for the NZD by year-end, remains unchanged. And we suspect the Kiwi flyer will have another bumpy ride over 2021. Interest rates are likely to remain at, or below, record lows into 2022. The ‘whatever it takes’ monetary policy mantra, and growing fiscal urgency, are powerful backstops for businesses and markets.

As economists we’re forced to make some pretty big assumptions. We’re assuming our bubble of 5 million remains Covid-free. We’re also assuming our borders remain closed until the middle of next year. Both assumptions are optimistic. Under our baseline assumptions the RBNZ will keep the cash rate unchanged well into 2022, as the local and global economy takes time to heel, and eventually recover. The risks to our assumptions are simply to the downside.

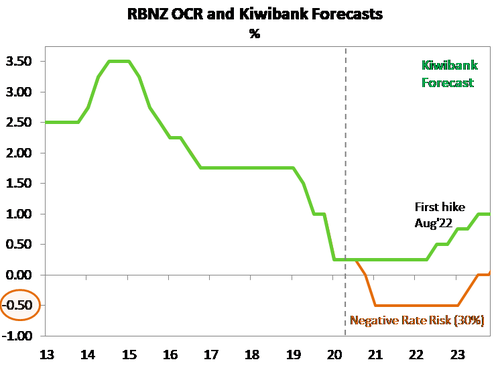

The downward skew in risks will keep our policymakers on the front foot. The ~$18b in unallocated Government recovery funds will be allocated. And the RBNZ has plenty of work left to do, with both inflation and employment mandates unmet. The $60b LSAP program will run out in May 2021. Stopping the LSAP program will cause an effective tightening in monetary conditions. Tightening policy is a discussion for another year, perhaps 2022, maybe 2023. The LSAP program will be extended, and doubled into 2022, in our view. If the RBNZ wants to drive retail lending and deposit rates lower, a term lending facility to the banks would have immediate effect. Term lending facilities have worked offshore, and would work in slashing retail rates in NZ. We believe the introduction of a term lending facility is probable.

The downward skew in risks will keep our policymakers on the front foot. The ~$18b in unallocated Government recovery funds will be allocated. And the RBNZ has plenty of work left to do, with both inflation and employment mandates unmet. The $60b LSAP program will run out in May 2021. Stopping the LSAP program will cause an effective tightening in monetary conditions. Tightening policy is a discussion for another year, perhaps 2022, maybe 2023. The LSAP program will be extended, and doubled into 2022, in our view. If the RBNZ wants to drive retail lending and deposit rates lower, a term lending facility to the banks would have immediate effect. Term lending facilities have worked offshore, and would work in slashing retail rates in NZ. We believe the introduction of a term lending facility is probable.

The message for businesses facing interest rate and currency risk is expect volatility in the currency, but much lower for much longer interest rates. Cash available for debt servicing is important in determining a businesses’ ability to leverage. The sharp decline in interest rates in recent years (and decades) has significantly reduced debt servicing costs for business and households. The RBNZ will keep it that way.

My Mandate’s Sedate: QEIII

“You gotta deal with it” Shihad

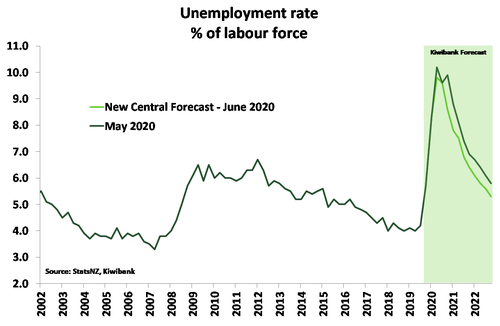

The RBNZ’s mandate is to “maintain stability in the general level of prices over the medium-term, and support maximum sustainable employment.” Based on our forecasts, the return to full employment and stable inflation (around 2%) will take at least two years to achieve. And that’s without any further shocks. As a consequence of the damage caused by the lockdown, and prolonged closure of the borders, the housing market is likely to correct by ~9% as well. The nature of the global shock means a swift full recovery is highly unlikely. There’s still a very long and bumpy road ahead, with plenty of risks from offshore – including a return of the virus itself, weaker trading partner growth, trade disputes, and the fact our borders will remain closed well into 2021. With both mandates unlikely to be met in the next two years, the RBNZ has more work to do to ensure the recovery is sustained.

Extending the QE program, call it QEIII, is inevitable. QEI was the initial $30b (actually make it $33b) commitment, in March. QEI was swiftly followed by QEII in May, doubling the program to $60b over 12 months to May 2021. QEIII, to be announced in August, will likely push the limit towards $100b, over a longer time frame into 2022. The program could then be extended to $120b into 2023. Extending QE in both duration and size is the (inevitable) next step for the RBNZ.

The expansion will enable the RBNZ to take down ~50% of (existing and incoming) Government debt issuance. LSAPs are limited to 50% of the total NZGBs on issue, with $139b total in 2021, $179bn in 2022, $198b in 2023, and $213b in 2024. The RBNZ could front load incoming issuance, but would need to expand the pool of assets purchased in our view. The RBNZ will continue to purchase LFGA debt and may consider buying other council (namely Auckland) and Housing NZ debt also. There’s still plenty of ammunition in the most preferred tool. But, beyond the $120bn to 2023, the program becomes more limited without a further increase in Government bonds. Therefore, if required, any further moves would involve the RBNZ pushing out the risk spectrum themselves, into all council, then corporate and bank bonds.

So, what about the other measures?

Term Lending to banks would be instant.

The next best policy tool would be a term funding facility for banks. Cheap term funding will lower all bank rates (deposit and lending) immediately. We’ve seen a sharp decline in wholesale and retail rates already. A term lending facility would provide even cheaper, term funding to banks. Such a facility would reduce bank dependence on both retail and wholesale markets. All borrowing and lending rates would fall as a result. The spreads between the cash rate (OIS strip), swap rates, and all lending and deposit rates would naturally compress as banks tap the RBNZ, not the market, for cheap funding. The RBA provides a facility to the Australian banks. And lending and deposit rates are significantly lower across the ditch. It’s an effective, and proven, tool.

FX intervention is useful, but success may be limited.

The RBNZ can sell unlimited, freshy minted, Kiwi dollars. The currency must be deemed “exceptionally high” and “unjustified” by economic fundamentals. Action must be “consistent with the PTA” (not hard), and at an “opportune” time to allow “a reasonable chance of success” (very hard). The first 3 criteria can be easy to meet. But the ‘opportune’ time for success is difficult. If global investors are piling into Kiwi dollars, because the rest of the world looks a lot worse, it’s difficult to stop. The Swiss tried a peg (trench warfare), but ultimately stepped away on 15th Jan 2015 (causing havoc). The RBNZ would have to engage in Guerrilla warfare. But it could be done. The RB could at least clean out a few positions and open up the market to downside risks.

Negative rates are debatable at best.

If New Zealand enters a dreaded double dip recession, or W shaped disaster, then negative rates may go from being possible to probable. But negative interest rates are still up for debate. And we are far from convinced. Evidence shows negative rates cause a perverse increase in savings and lowers inflation expectations. We believe the drastic step is a last resort, and the last tool to be used. But there is a growing call for negative rates, and rates that are well below the negative rates seen in some parts of the world. Our work on the demographic influence on interest rates suggests New Zealand’s ageing population may push interest rates negative – as seen offshore. 75% of the decline in global interest rates can be attributed to ageing populations (increased savings and decreased investment). And negative rates may come to be seen as intergenerational wealth transfer… Talk of negative interest rates, however, has caused financial markets to persistently price in the risk, and the currency has traded lower (at times) as a result. Continued “jawboning” may help push the currency lower, and keep downward pressure on rates. But we don’t expect a negative OCR in this cycle. Although negative rates cannot be ruled out. Policy makers will do whatever they deem necessary in a recession.

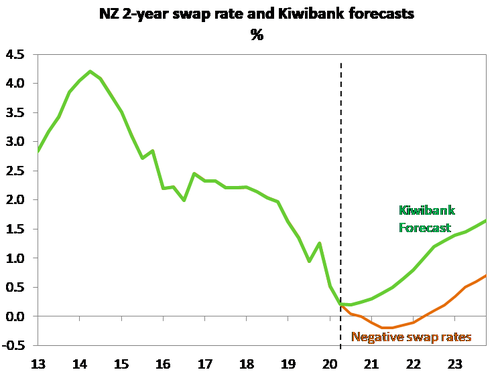

In terms of wholesale swap rate forecasts, we have the 2-year swap rate holding here cash (0.25%) over 2021, as the RBNZ’s on-hold guidance likely extends into 2022. The main risk to our central view is a shock (community transmission induced lockdown) that causes the RBNZ to embark on a path below zero. A negative OCR would most likely mean a 75bp cut to -50bps. In such a scenario, the Government bond curve, out to 10-years at least, would trade negative. All NZGB investors, including local superannuation funds, asset managers, insurance providers, banks and foreign investors would pay the Government for the right to buy their bonds. It’s a bit like the Government receiving $100 cash for a bond (IOU), and only paying back $98 in a few years time.

In terms of wholesale swap rate forecasts, we have the 2-year swap rate holding here cash (0.25%) over 2021, as the RBNZ’s on-hold guidance likely extends into 2022. The main risk to our central view is a shock (community transmission induced lockdown) that causes the RBNZ to embark on a path below zero. A negative OCR would most likely mean a 75bp cut to -50bps. In such a scenario, the Government bond curve, out to 10-years at least, would trade negative. All NZGB investors, including local superannuation funds, asset managers, insurance providers, banks and foreign investors would pay the Government for the right to buy their bonds. It’s a bit like the Government receiving $100 cash for a bond (IOU), and only paying back $98 in a few years time.

Sitting at a spread above the NZGBs, wholesale swap rates would also delve into the negative, just not as much. We would expect to see the 2-year swap rate trade down towards -25bps if the OCR hit -50bps, for example. Given 2-year fixed mortgages rates are hedged off the 2-year swap rate, such a move would cause a large downshift in mortgage and business lending rates. Deposit rates would follow suit.

Then the complication begins. The decline in retail deposit rates towards (but not through) zero, is likely to induce a higher level of savings – as experienced offshore. Because savers realise they need to save at a harder and faster rate to achieve their goals, or maintain the same standard of living (if retired). The removal of interest on Government bonds also adds stress to all the forced local fixed income investors. Added stress to the financial system at a time when policymakers are trying to rebuild, is a risk not taken lightly.

The outlook for rates in 2021 is either ‘on hold, at record low levels’, or ‘going negative, to record breaking levels’. Interest rate risk to the upside, is a risk for another year. From 2022, we see a very gradual lift in rates as the recovery continues and the RBNZ potentially moves to a tightening bias. We have pencilled in a gradual normalisation of policy from August 2022, all going well. We believe the normalisation process would include a long pause in QE (holding the RBNZ’s balance sheet unchanged) followed by an eventual evaporation of QE (or QT, Quantitative Tightening), allowing the curve to lift and bear steepen. The RBNZ would also embark on a very light lifting of the OCR back towards 2%, but no more, by 2026. That’s a very protracted ‘normalisation’ of policy. Even in our optimistic scenario, we struggle to see a sharp increase in interest rates over the medium term.

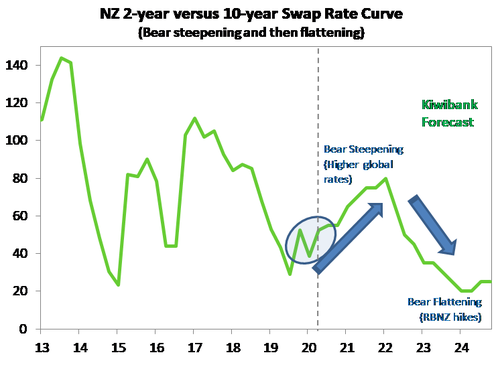

As our chart demonstrates, longer dated bond yields are likely to lift first, steepening the curve. Indeed, we forecast a ‘bear steepening’ of Kiwi rate curves into 2022, assisted (hopefully) by rising yields globally. The curve only begins to flatten (if and) when the RBNZ starts lifting the OCR.

As our chart demonstrates, longer dated bond yields are likely to lift first, steepening the curve. Indeed, we forecast a ‘bear steepening’ of Kiwi rate curves into 2022, assisted (hopefully) by rising yields globally. The curve only begins to flatten (if and) when the RBNZ starts lifting the OCR.

Low and flat interest rates over 2021, should mean the action will (again) be in currencies. And the Kiwi is the most volatile of the world’s top traded currencies. Hold onto your seats. Unlike the beauty of interest rates, that can all fall together, currencies are a different beast. Currencies are a relative price, and can’t all fall together. In the Covid world, the Kiwi is relatively attractive. Our pretty bird looks gorgeous compared to the dodos offshore. And investors are piling in.

Home again: the Kiwi flyer pushes higher as Kiwis return.

“So sit and wait. And bend and break. You rise and fall. Just you, that's all. I'm here, you're there. It don't mean I don't care” Shihad

Success in eliminating the virus and moving out of lockdown earlier, makes New Zealand the envy of the world. Kiwis are flying home in droves. It’s the place to be, if you can get here. And the sharp bounce in spending and activity out of lockdown, has us growing in confidence. Our currency is reflecting the relative optimism, and has risen sharply towards 66c. The recent low of 55c seems like a lifetime ago.

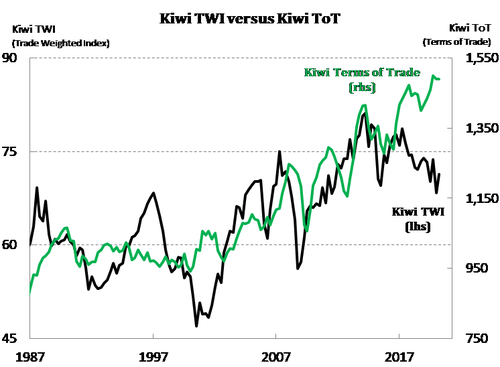

The strength of the Kiwi flyer has been supported by a strong terms of trade (for now). Our export prices have held up relatively well, and our imported prices (including oil) have eased. The elevated terms of trade is supportive during our time of need, especially on the export side. But the rising currency can quickly undermine the terms of trade boost.

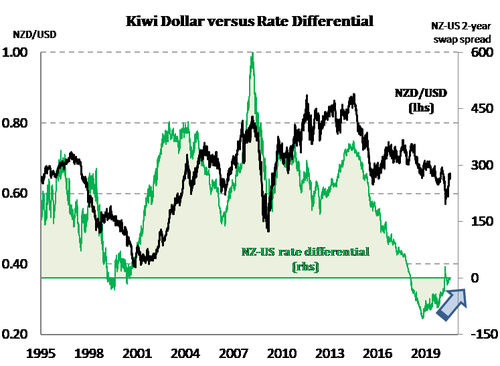

The other major driver of the Kiwi flyer is interest rate differentials. The Kiwi currency is also being supported by more advantageous interest rate differentials. We talk of RBNZ action, but other central banks are forced to do more.

We forecast the Kiwi flyer to end the year higher. Our NZD/USD forecasts have barely changed from early in the year, but the complexities around the forecasts have changed substantially. The Kiwi should remain relatively well bid into year end. But we suspect a drop back into the low 60s in 2021. Further policy action from the RBNZ will assist the Kiwi’s decline. At 66c today, the risk is asymmetrically lower. Our year end forecast of 67c offers little in the way of upside. As the world eventually (hopefully) recovers into 2022, we expect the Kiwi to outperform once again. ,Risk assets will gather momentum. And with a rise in risk appetite, the Kiwi flyer surges higher.

If you’re an exporter, hedging exposures to a rising currency can assist. You will hopefully get your turn to play in the low 60s.

If you’re an importer, 67c is within sight, and there may be a push towards 70c temporarily. Beware of negative press, central bank jawboning and downside scenarios.