- Today’s Budget showed the Minister of Finance in an enviable position. Providing a large boost in spending and lowering the debt projections at the same time.

- The headline announcement was a $3.3bn lift in social welfare benefits. Other items included a hike in health spending and investment in climate change mitigation.

- An upgraded set of economic forecasts by the Treasury means the Government is expected to run smaller fiscal deficits over the forecast horizon. Even with conservative revenue projections

- Net debt is expected to peak at a lower 48% of GDP in 2023. But excluding the Funding for Lending Programme net debt hits only 41%. The Government has ample fiscal room to do more and address our housing and infrastructure deficits.

- Despite the stronger fiscal outlook, NZDM’s planned bond issuance programme was lowered by a smaller than expected $10bn over the next four years.

The 2021 Budget put the Minister of Finance in the dream position. A surprisingly resilient economy following the shock of covid-19 has allowed the Government to hike spending and lower the debt projection at the same time.

In terms of budget announcements, the biggest surprise was a $3.3bn boost to benefit payments. From 1 April next year main benefit rates will rise between $32 and $55 per week. The Government earmarked an additional $4.7bn hike in health spending. Another key spending item was around climate change mitigation. Greater investment toward low-carbon technology and innovation within the climate change space was especially encouraging, and a continued step in the right direction. The $300mil injection into NZ Green Investment Finance supports the transition to a low-emission economy. Because cleaner, greener and more efficient technology is needed to make the transition. There was however a lack of further spending on housing, the big-ticket item being the $3.8bn already announced to accelerate councils into action on housing-related infrastructure.

An upgrade to the Treasury’s economic outlook helped to produce smaller deficits compared to forecasts produced in December. Even with conservative revenue projections, the Government is expected to run shrinking fiscal deficits and be within striking distance of a surplus by the end of the forecast period. We believe the forecasts are cautious and will set the Government up for more positive surprises down the track. Net debt as a share of the size of the economy is projected to peak at 41%, excluding the Funding for Lending Programme (FLP), which should be excluded. The Government could easily have done more to address some of our longer-term issues, borrowing more and rating agencies would have hardly batted an eyelid.

The improved fiscal position means the Debt Management Office (NZDM) has lowered its planned debt issuance over the next four years by $10bn. The $10bn reduction was smaller than we expected, and a result of cautious revenue projections. In a move that should be applauded, the NZDO is planning to issue a 30yr bond before the end of 2021. It makes perfect sense to borrow longer-term and take advantage of the current low interest rate environment. Especially when there is a desperate need for further infrastructure investment that will deliver economic payoffs well into the future.

Adjusting the outlook brightness

The Treasury’s HYEFU forecasts were deemed on the pessimistic side at the time they were published in December. It’s unsurprising then that following better than expected data since, large upgrades were on the cards.

Forecasts for economic growth over 2021 has been appropriately revised upward from 1.9% to 2.9%, and average a strong 3.4% over the forecast horizon. Underpinning the resilience in economic activity has been the adaptability of Kiwi business and the surprising strength of domestic demand. Indeed, the relatively swift economic recovery suggests that the covid shock will leave less of a mark. The Treasury see a reduction in expected scarring from Covid-19, with potential output left at pre-pandemic levels. Nominal GDP too is higher over the forecast period compared to the HYEFU forecasts. Improved nominal GDP outlook feeds through to higher forecasts of tax revenue and an improved fiscal position (see below).

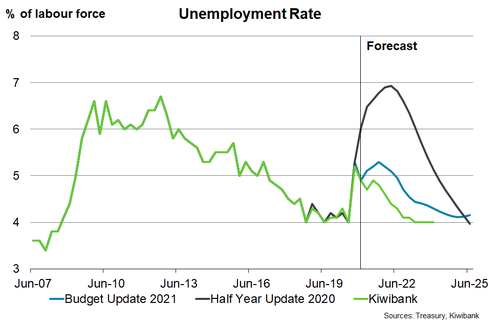

NZ labour market has shown remarkable resilience to last year’s Covid disruption, the unemployment rate falling to 4.7%. Fiscal support – chiefly, the wage subsidy – was instrumental in safeguarding employees. Accordingly, the Treasury’s new forecasts are relatively more upbeat than their last print. The Dec HYEFU’s 6.8% peak in the unemployment rate has been twinked-out and written over with a 5.2% peak by the middle of the year. The rate is expected to slowly decline to 4.5% by 2023. We also expect the unemployment rate to flirt around current levels (4.7%) in the near-term. But in our view, Q3’s 5.2% represents the peak in the current cycle, and won’t be repeated (see below).

The Treasury too see a short-term rise inflation to 2.4% in the June quarter of this year. A combination of base effects, strong domestic demand and supply chain disruptions is in the mix. But as is general consensus, some of the drivers of rising inflation in the near-term can be ruled as temporary. A sub-2% reading is forecast in 2022 as capacity constrains in construction ease and supply chain issues are resolved. Over the next few years, persistent spare capacity continues to weigh on the inflation trajectory. The Treasury don’t expect inflation to reach and remain above 2% until 2024.

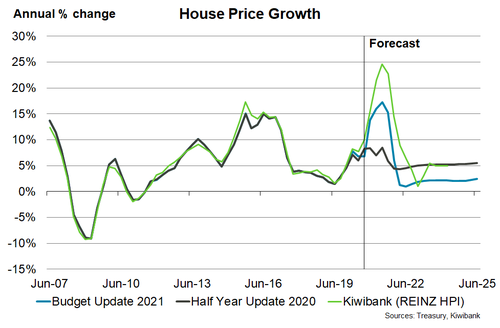

The unbelievable performance of the housing market since lockdown continues to hog the headlines as housing affordability worsens. The Treasury is forecasting annual house price growth to come in at 17.3% in the June 2021 quarter. A steep decline to 0.9%yoy growth is forecast by June 2022 as the Government’s recent tweaks to housing tax policy and the RBNZ’s tightened lending restrictions kick in, kicking out investors. We think the peak in house price growth is too light and expect a figure closer to 25%. We also forecast a relatively more steady decline in the growth rate over the coming  year, with a drop to around 1%yoy closer to the end of next year.

year, with a drop to around 1%yoy closer to the end of next year.

The Treasury incorporated revised assumptions around the economic impact of covid alert levels. The NZ economy has proven to be far more resilient to social distancing than previously estimated. If we find ourselves in the unfortunate position of tightening covid alert levels, the assumed hit to the economy is less severe.

The economy’s resilience shows through the books

The Budget presents the Government’s books in far better shape than thought possible a year ago amid the uncertainty of the pandemic. Much like the state of the economy. The position the Government finds its books in has allowed it to lift spending over and above what had been previously signalled. And show forecasts of a smaller deficit and debt load. We question the logic of the urgency of getting back to surplus giving the ongoing significant infrastructure and housing deficits. Moreover, these challenges are occurring at a time when borrowing rates are still at historically low levels.

The brighter economic outlook has once again seen tax revenue revised higher. The country’s tax base, nominal GDP, was revised a cumulative $100bn higher by the Treasury over the forecast period. However, not all of the increase in nominal GDP forecasts have flown through to tax revenue. Since HYEFU StatsNZ revised nominal GDP significantly higher, meaning the Treasury had been working with a lower tax base than was actually the case. Nevertheless, the brighter economic outlook translates into a larger tax take out to 2025.

The stronger economic outlook and financial position meat that the Government was able to lift planned spending. Operating allowances for future budgets were tweaked higher to $2.7bn. The capital allowance envelope was also lifted. But why not do more? On housing, there was little new over and above the $3.8bn Housing Acceleration Fund already announced. Back in March the Government released its housing policy, tackling both demand and supply, but not doing enough to help increase the latter (see a drop in a leaky bucket).

Even with the boost in planned spending, the Crown’s operating balance (OBEGAL) is expected, in general, to show deficits falling faster than previously expected. OBEGAL deficit is forecast in the current year to June to come in at $15.1bn. A deficit that’s down almost $8bn from last year’s and $6.5bn less than had previously been forecast. Some planned spending has been pushed out, leading to a higher fiscal deficit in the 2022 fiscal year. But deficits shrink rapidly to be within touching distance of a surplus in 2025.

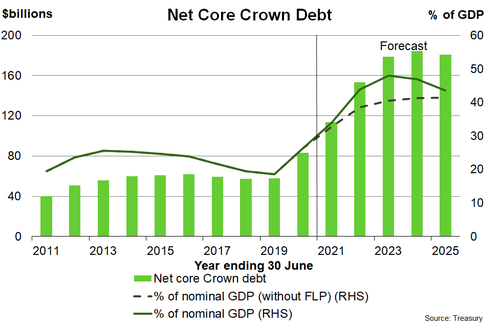

Net core Crown debt is now forecast to peak at exactly $10bn lower at $184.2 in the 2024 fiscal year. As a share of the economy, net debt peaks in 2023 at 48% of GDP, down from 52.6% at HYEFU. However, as the Treasury points out headline debt figures are inflated by the RBNZ’s FLP. The FLP programme is providing banks with cheap 3-year funding to lend to Kiwi households and businesses. Excluding FLP from the net debt calculation reveals a peak of 41.4% of GDP. Importantly, the FLP is time constrained and runs to the end of next year. As FLP funding matures, banks will need to pay it back – i.e. replace it with other forms of funding – taking it off the Government’s balance sheet. So, in fact the Government debt load is much smaller than fist advertised. The Government could easily have done more to address some of our longer-term issues, and rating agencies would hardly have batted an eyelid.

A fiscal shot in the arm

Just like Kiwi with the covid vaccine, the economy is forecast to get a fiscal shot in the arm over the coming fiscal year. Treasury’s fiscal impulse analysis showed after the surprise fall in deficit in the current fiscal year, the shift in spending to next year will deliver an almost 2% boost (as a share of GDP) in the 2022 fiscal year. Looking at how the economy has been cushioned by covid-19 policy stimulus, the need for larger stimulus is perhaps less pressing.

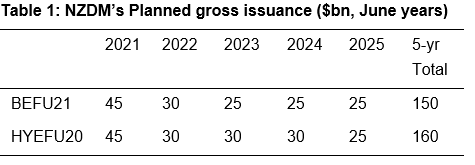

NZDM lowers its planned debt issuance again.

Following on from the Government’s stronger financial position NZDMO’s planned bond issuance has been lowered. However, gross issuance was lowered by just $5bn in both 2023 and 2025 fiscal years – less than many had expected.

Encouragingly NZDM is looking to issue a new 30yr government bond before the end of the year. A 30yr tenor would be the longest issued by NZDM. Strategically, a 30yr bond is a great move! Enabling the Government to take advantage of the current low interest rate environment. Locking in cheap funding rates and use the debt for long-term projects.