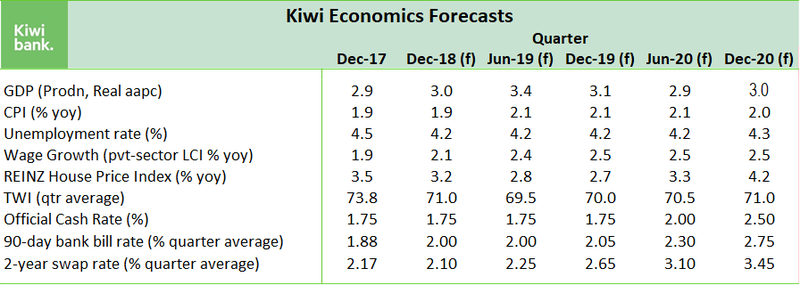

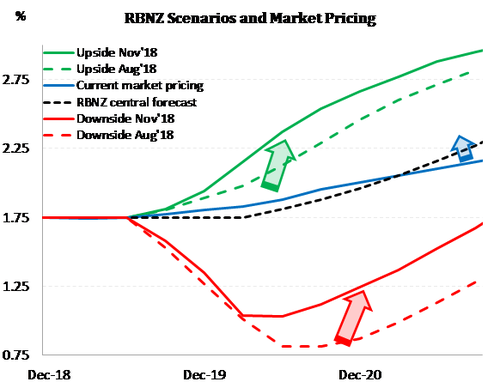

The RBNZ reduced the downside risks, and heightened the upside risks. Risks remain, and the central (message) track is the same.

Pigeon risks prevail – they’re all around, not just down

- The RBNZ are on hold into 2020. The central track and message is still one of stability.

- The balance of risk has changed. The asymmetric downside risks presented in August have been evened up. There’s still a slight downside slant near-term, but a larger upside slant long-term.

- The explicit mention of the next move being “up or down”, was replaced with “data dependent”. The RBNZ has acknowledged the uplifting data of late.

- But “[RBNZ] will keep the OCR at an expansionary level for a considerable period to contribute to maximising sustainable employment, and maintaining low and stable inflation.” Don’t fear rampantly rising rates.

“We are very data dependent. The risks remain.” Governor Adrian Orr

The RBNZ have shifted. After surprising the market with a “blatantly dovish, shock and orr” commentary just 3 months ago, the central bank has re-centred its risk assessment. The RB’s risk assessment has shifted back to a pigeon-like, look out for everything up and down. The shift is a welcome move from the very dovish, more risks to the downside, commentary in August. But we must note, the bank is far from hawkish, as the risks from above need time to play out.

Our first chart shows the positive shift in the bank’s perceived risks since the August statement. The central track is unchanged. The cash rate is expected to remain unchanged until late in 2020. The message to Kiwi businesses and households is simply: don’t fear rampantly rising interest rates, and fear less a sharp decline led by bad outcomes. The RB is cognisant of the weakness in both business and household confidence. And risks to the outlook clearly remain.

When asked why the RB hasn’t lifted the central OCR track, Orr noted: “Core inflation is still below the mid-point of our target band… so why would we remove the optionality of cutting rates? We wouldn’t”. Orr also flagged “Huge policy uncertainty” across what the central bank itself might, or might not do, and especially around Government policy – including Brightline tests and capital gains tax.

The Governor noted the currency has been “well behaved”, and it will do what it does. The movements in the currency over the last 6 months has reflected relative developments. The Kiwi dollar has popped to the highest level seen since the RBNZ’s “shock and orr” statement in August. Having broken through 65c, the bird has been well bid back up towards 68c. The lion’s share of the move took place yesterday, following the stellar labour market report which finished a “great Kiwi economic trifecta”.

The Kiwi interest rate market has also lifted with diminishing downside risks, and thoughts of (potentially) earlier cash rate hikes. The 2-year swap rate has jumped 13bps to 2.15% this week. Again, all of the move took place yesterday. Today’s RBNZ statement merely met recently adjusted market expectations.

The main message in today’s statement is that the downside risks to the outlook have receded. But the risks have not disappeared, they never do. Our forecast of a May 2020 RBNZ rate hike remains, and remains 6 month ahead of the RBNZ’s own track. We hope the risks develop in such a way that a late 2019 rate hike is put on the table. That would mean we have seen a solid year of growth in the year ahead – bettering our existing forecasts. That’s the way we see the risks. The glass being more full, than half empty.

The Bank is still worried about growth over the medium term

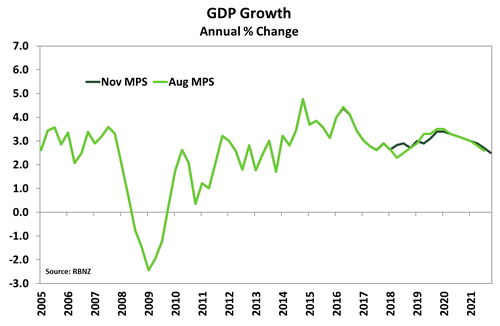

What remains clear is that despite recent developments, the RBNZ is still concerned about the risks to growth over the medium term. Business confidence, and more importantly firms’ expectation of their own activity, remain depressed and the Bank is not taking any chances – policy settings are stimulatory and will remain so for some time. The RBNZ dismissed the June quarter’s stronger-than-expected GDP growth by noting that much of the 1% qoq rate of growth was driven by temporary factors. Overall, the Bank’s GDP forecasts are largely unchanged. The concern around business confidence was reinforced by the RBNZ’s downside scenario.

The Bank’s inflation outlook is much higher than what was presented three months ago. The stronger inflation seen since the August MPS can’t be ignored. Like us they see CPI inflation average 2.1% yoy over the first half of 2019. Surprisingly, inflation is expected to peak at 2.3% yoy Q3 2021 (quite far above the target midpoint). In the MPS the Bank focussed on the steady march higher in petrol prices. The RBNZ included a concise analytical box (Box B: Recent petrol price increases and monetary policy). The RBNZ will look through the first-round impact of higher prices at the pump. What is more concerning would be the second and third-round responses to higher fuel prices, such as a fall in household spending as budgets take a hit. Petrol prices have eased in recent weeks on the back of easing global oil prices, but the trend has been for rising oil prices over the last 18-month – the trend is certainly not ones’ friend.

The Bank’s inflation outlook is much higher than what was presented three months ago. The stronger inflation seen since the August MPS can’t be ignored. Like us they see CPI inflation average 2.1% yoy over the first half of 2019. Surprisingly, inflation is expected to peak at 2.3% yoy Q3 2021 (quite far above the target midpoint). In the MPS the Bank focussed on the steady march higher in petrol prices. The RBNZ included a concise analytical box (Box B: Recent petrol price increases and monetary policy). The RBNZ will look through the first-round impact of higher prices at the pump. What is more concerning would be the second and third-round responses to higher fuel prices, such as a fall in household spending as budgets take a hit. Petrol prices have eased in recent weeks on the back of easing global oil prices, but the trend has been for rising oil prices over the last 18-month – the trend is certainly not ones’ friend.

The RBNZ may already be behind the eight-ball on domestic inflation pressure, however. Yesterday’s shock drop in the unemployment rate to 3.9% suggests the labour market is much tighter than the Bank had in mind when formulating the November MPS. Wage growth may rise faster than expected, adding to firms’ cost pressures and inflation. We may be above the maximum sustainable level of employment. However, it should be mentioned that it’s not unusual for labour market data to jump around from time-to-time. We could easily see a partial reversal in yesterday’s stellar results in the December quarter. Nevertheless, people who are looking for work are finding work. Net migration is falling making it easier for the labour market to absorb a growing potential workforce. Rising household income growth could easily offset the pressure coming down on budgets from petrol prices.

International uncertainty is still a dominant risk.

Global growth is strong and is expected to remain decent. However, heightened global uncertainty, in particular for worsening trade tensions between the US and China, does highlight that risks to global growth is to the downside.

Market Reaction.

There was relatively little market reaction to the November MPS. Yesterday was the day for market traders to react. Following developments of the last few days OCR pricing has moved take a rate cut as the next move off the table. The market is fully pricing a rate hike by September 2020. And there is now around a 70% chance that the RBNZ will hike in May 2020, when we expect this to happen.