Key Points

- Headline CPI inflation came in at 0.6%qoq in the June quarter, in line with the RBNZ’s and market consensus forecasts. Meaning annual inflation lifted to 1.7%yoy from 1.5%yoy in March.

- Rising rents, petrol, and food prices drove inflation in the second quarter. These were partly offset by a seasonal fall in domestic airfares, and a fall in the price of used cars.

- Measure of underlying inflation universally strengthened in the middle of 2019.

- The jump in annual inflation in Q2 is likely to be temporary spike, and we expect it to drop to 1.3%yoy next quarter. Petrol prices have already stabilised. More of a concern is the slowdown in forward indicators of economic growth.

- As a result, the RBNZ is likely to look through today’s inflation report, and in our view deliver a cut to the OCR to 1.25% in August. Risks of further cuts have risen in recent weeks.

Summary

Headline CPI inflation came in at 0.6%qoq, bang-on RBNZ and market consensus forecasts. Annual inflation lifted to 1.7%yoy from 1.5%yoy at the start of 2019. The key drivers of higher fuel and housing-related price rises were expected too. There was hardly a whisper from financial markets. As the report didn’t contain enough new information to change anyone’s view, on anything important. New Zealand’s inflation may have risen in the June quarter, even underlying inflation pressure looked stronger, but the key for monetary policy is the outlook. And the outlook for inflation has deteriorated.

The rise in annual inflation is likely to be a temporary spike that will unwind in the September quarter. Petrol prices have already stabilised so are unlikely to feature as prominently in Q3’s figure.

Of more concern for future inflation is the weakness seen in forward indicators of economic growth. The cost pressure firms complain of, is not being passed on to consumers. And that’s a sign of weakness. The RBNZ is likely to look through today’s inflation report. And in our view, the RBNZ will deliver a 25bp cut in the OCR to 1.25% in August. The chance of a further move below 1% is increasing, and is not far from becoming our central forecast.

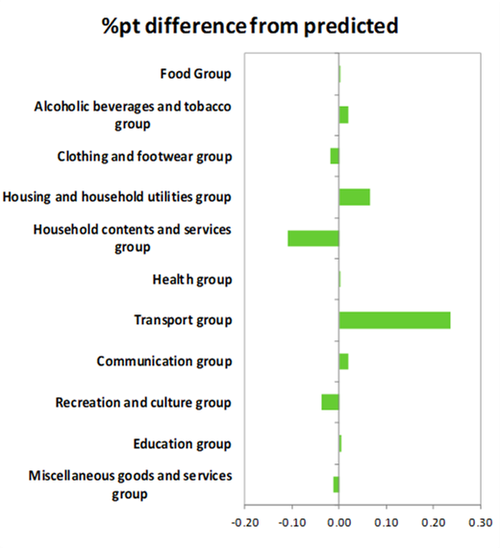

Q2 inflation generated by petrol and housing

As expected, housing and transport related price rises were key drivers of June quarter inflation. Rising food prices also contributed. The surprise for us was the lack of inflation seen in the transport group (see chart below). Petrol prices jumped 5.8%qoq in line with stronger oil prices and lower dollar – not quite as strong as we had expected. There was the usual seasonal fall in domestic airfares to provide a partial offset. But there was also a surprisingly large 3.9%qoq fall in the price of used cars.

Putting aside the volatile movements of petrol prices, there is the continuing pocket of inflation around housing-related goods and services. The squeeze on housing from the recent and rapid rises in NZ’s population are reflected here. Rising rents, the cost of construction, and local government rates are all adding to the housing group. Rents were 1%qoq up, the strongest quarterly rise since early 2008. The rise in rents coincides with a recent change in methodology by StatsNZ. Among the main centres Wellington led the way with a 1.4%qoq increase in rents. It’s easy to see the significance of housing on headline inflation. Headline CPI inflation less housing was only 1.2%yoy higher in the June quarter.

Clash of the titans

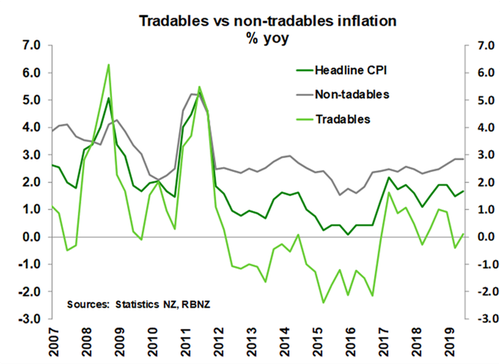

Annual inflation reflects a clash between weak imported inflation and slow moving domestic inflation. Annual inflation lifted to 1.7%yoy, from 1.5%yoy. But we small spike is an optical illusion. Because we expect inflation to fade back down to 1.3% in the September quarter. That’s further away from the RBNZ’s target midpoint of 2%yoy. Major drivers of annual inflation come from rising housing related prices and tobacco excise hikes.

Annual tradables inflation lifted to 0.1% from a -0.4%yoy fall the quarter prior. Higher petrol prices and overseas accommodation were offset by the perennially cheaper telecommunication equipment. Our smartphones continue to get smarter while prices hardly budge - a price fall in the world of inflation statistics. Non-tradables inflation was unchanged at 2.8%yoy, housing-related inflation is the main driver here. While non-tradables inflation is persistent in nature, a slowing economy can easily turn the worm lower.

Annual tradables inflation lifted to 0.1% from a -0.4%yoy fall the quarter prior. Higher petrol prices and overseas accommodation were offset by the perennially cheaper telecommunication equipment. Our smartphones continue to get smarter while prices hardly budge - a price fall in the world of inflation statistics. Non-tradables inflation was unchanged at 2.8%yoy, housing-related inflation is the main driver here. While non-tradables inflation is persistent in nature, a slowing economy can easily turn the worm lower.

Core inflation is universally higher

Measures of core inflation, excluding the volatile stuff, universally strengthened in the June quarter. Core measures lifted towards 2%yoy, close to the RBNZ’s target, but we’re not convinced these measures will hold for long. The RBNZ will also be wary of the potentially temporary lift. We will be looking to see if the RBNZ’s own core measure of inflation for the second quarter echoes StatsNZ’s findings when it’s released at 3pm this afternoon. Stripping out some of the more volatile components, i.e. inflation less food, energy and petrol prices inflation lifted to 1.7%. Moreover, StatsNZ’s trimmed mean measures (a more technical way to strip out volatile price movements) came in above annual headline inflation at between 1.9-2.1%yoy.

Market Reaction

The reaction in financial markets was rather muted. The currency tried to like the report, but there wasn’t enough to get too excited about. The NZD rose following the release, as the underlying inflation rates proved a little stronger than expected. Interest rates were largely unchanged. Wholesale interest rates are still down on yesterday’s close, given the move lower in international interest rates. The muted reaction in markets is justified by the lack of new information, and the deterioration in the outlook. We still expect the RBNZ to cut 25bps to 1.25% in August, and traders agree. The implied pricing for future RBNZ rate decisions, has an 80% chance of a cut in August. We’d agree. And then there’s an additional 22bps of cut priced to 1.03%. That’s the markets way of saying there’s another 90% chance of a cut to 1%. Or as we see it, there’s another 45% chance of a cut to 0.75%. And we agree. In March we changed our call to a 1.25% OCR by August, and we flagged a 40% chance of a further move to 0.75%. The chance of a further move below 1% is increasing, and is not far from becoming our central forecast.