Key Points

- It’s no surprise that the 5.5%qoq (20%yoy) spike in petrol prices contributed 40% of the annual gain.

- Excluding petrol, prices rose a solid 0.7%qoq.

- Non-tradables inflation, domestically generated, was slightly stronger. The RBNZ is on hold.

Summary

There was a punchy lift in September quarter CPI inflation, expanding 0.9%qoq (above consensus of 0.7%qoq) to take annual inflation to 1.9%yoy – a touch below to the RBNZ’s 2% target mid-point. As expected a jump in transport and further strengthening in housing-related prices were the main elements of third quarter inflation.

September quarter inflation result was a significant step higher than the RBNZ’s August Monetary Policy Statement (MPS) forecast of just 1.4%yoy. The RBNZ is starting to be backed into an awkward position, with its view that inflation will gradually rise to the target mid-point increasingly untenable. For now at least, the RBNZ can still claim that much of the recent rise in inflation pressure is coming from cost-push inflation factors that can be looked through. These cost-push factors include higher world oil prices, a weaker currency and Government induced price hikes (such as petrol taxes and a chunky minimum wage hike). What the Bank is likely to remain focused on is the underlying engine of inflation, GDP growth. With business confidence still casting a shadow over the economy there remains the risk that internally generated inflation peters out. However, as the Bank has drummed home, price setting behaviour is being more driven by actual inflation. With headline inflation on the charge, momentum is likely to build in the figures. In addition, we see GDP growth picking up above trend into 2019, and inflation is likely to accelerate. We believe that ultimately the RBNZ will be forced to begin gradually hiking the OCR sooner than is currently signalled. We believe the RBNZ will be able to hike by May 2020, 6 months ahead of their schedule.

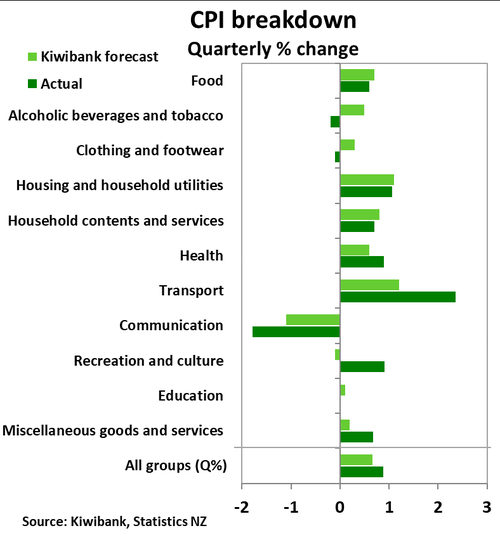

Transport and housing is more expensive

As expected, the dominant drivers of September quarter inflation came from transport and housing-related price rises. For transport higher fuel prices were the primary reason. Petrol prices have risen 19% since the September quarter last year according to SatsNZ. That’s hard to argue with when filling up at the petrol station. Global oil prices have steadily increased this year and combined with the recent fall in the dollar led to a 5.5% qoq fall. Also captured in higher fuel prices was the introduction of the Auckland regional fuel tax (10 cents/litre). Domestic air-fares increased 8.1% qoq, and shows that the steady rise in fuel prices is feeding into general transport costs, which looks set to continue in the December quarter. The CPI’s housing group experienced a 1.1% qoq rise. Local council rates, which usually play a decent role in the September quarter, were 5.5% qoq. However, ongoing rents and construction costs were once again a feature of housing-related inflation.

Both tradables and non-tradables prices made similar contributions to headline inflation. But stronger transport prices meant tradables inflation came in at 0.9%qoq, the highest quarterly rise since 2015.

Underlying inflation just edging higher

Underlying measures of inflation were broadly stronger in the third quarter also putting the RBNZ in a difficult position. However, it was easy to see the impact that higher fuel prices had on inflation in the quarter. Headline annual CPI inflation excluding vehicle fuels came in at 1.1%yoy for the third consecutive time. Nevertheless, inflation excluding food and energy prices (closely followed by the RBNZ) did manage to lift a touch to 1.2%yoy, that’s up from 1.1%yoy in the June quarter, and 0.9%yoy at the start of the year. Trimmed means measures of inflation, which excludes volatile price movements, were between 1.8%-1.9%yoy.

This afternoon at 3pm, the RBNZ will releases its latest update of the sectoral factor model of core inflation. In the June quarter, there was a surprising lift in this measure to 1.7%yoy, so expect wide market interest in this figure.

Market reaction

The reaction in financial markets was swift. The Kiwi dollar jumped around 40pts (~0.7%). The all-too-important 2-year swap rate lifted from 2.02% to 2.045%, with most of the reaction in rates occurring a little further out. For example, the 7-year swap rate rose 5bps to 2.67%. It’s a good news story, and one that demands a lift in pricing.