- The RBNZ hiked the cash rate 50bps to 3.5%, for the fifth consecutive meeting. The decision was in line with our view and that of the markets’. The cash rate has been pushed well through neutral (2%) and into truly restrictive territory. The RBNZ reiterated its resolve to break inflation back down to 2%.

- The statement was punchy and hawkish, and highlighted the need to demand destruct inflation back to target. We still expect the RBNZ to hike to 4%, and pause. Global demand is easing with probable recession risks in the northern hemisphere.

- There was a see-saw reaction in financial markets. Wholesale interest rates markets saw a spike and then a decline. The Kiwi dollar lifted sharply, and then fell back down. The statement was initially seen as much more hawkish. But then traders had second thoughts.

The RBNZ maintained a determined and resolute policy stance. Inflation needs to fall, and by quite a bit. The statement was punchy and hawkish, and highlighted the need to demand destruct inflation back to target. The committee actually contemplated hiking the cash rate by 75bps. “The Committee considered whether to increase the OCR by 50 or 75 basis points at this meeting. Some members highlighted that a larger increase in the OCR now would reduce the likelihood of a higher peak in the OCR being required. Other members emphasised the degree of policy tightening delivered to date.” (RBNZ October MPR).

More rate rises are required for mandates to be met. We have at least another 50bps of tightening to come.

“Committee members agreed that monetary conditions needed to continue to tighten until they are confident there is sufficient restraint on spending to bring inflation back within its 1-3 percent per annum target range.” (RBNZ October MPR)

We continue to forecast a peak in this cycle of 4.0%. Although the risk is clearly tilted towards even more policy tightening to 4.5%. We believe the RBNZ is getting significant traction from its rate hikes to date. The forward-looking indicators are showing a significant slowdown in growth. Both business and consumer confidence has been hit, hard, and the housing market is in full retreat. We are becoming increasingly wary of the consequences such tightening will bring. Most outstanding mortgages roll onto much higher rates in the next 6 months – over spring and summer - the busy period for housing activity.

The cost of home ownership is increasing, fast. Mortgage interest rates were around 2-2.5% early last year. Mortgage rates are now around 5.5-6%. They have more than doubled. For example, the extra 3% (300bps) on a mortgage of $800,000 equates to an increase in interest repayments of $24,000 per year. So total interest repayments in this example have gone from $20,000 per year to $44,000. There will be a profound impact on discretionary spending – by RBNZ design. Unfortunately, the RBNZ needs to see this pain in households before they are confident they’ll beat inflation back down to 2%.

We also put a larger weight on international forces. The swift and sizable increases in global interest rates are likely to cause a recession in parts, with the risk of a larger, global recession. Highly probable recessions in the UK and Europe, alongside a possible recession in the US will have a profound impact on Asian growth. And China is already struggling. The outlook for our trading partners has weakened. And we will feel it directly from China (our largest trading partner) and indirectly from Australia (or second largest trading partner).

Half of the inflation seen over the last year was generated offshore. The sharp slowdown in global growth will bring weaker commodity prices. And global shipping costs are already falling (click here). Tradables (imported) inflation is set to decline quite quickly into 2023. Although the recent decline in the Kiwi currency will frustrate the move lower, at least near term.

“Recent indicators suggest the global growth outlook has weakened, in part due to tighter global financial conditions.” (RBNZ October MPR)

Job’s not done

Inflation may have peaked at 7.3%. But the RBNZ expects a slow descent from here. Inflation is set to remain above the 1-3% target band until the middle of 2024 – that’s three quarters longer than previously forecast.

It is the acceleration in wages that would worry the RBNZ about second round effects of inflation.

The lift in domestic inflation and wage growth forecasts support the RBNZ’s hiking campaign. Inflation expectations may have fallen, recently, but they remain too high. The RBNZ would want to see actual inflation clearly and firmly heading south before they consider slowing the pace of tightening.

The more the RBNZ tightens monetary conditions, however, the dimmer the economic outlook. Consumer confidence has fallen to recessionary levels. Households are operating in an increasingly expensive environment. High interest rates and high living costs are eating into discretionary spend. And a weaker wealth effect from falling house prices will also weigh on household consumption in the coming months. Businesses too are feeling downbeat. The ongoing supply-side issues continue to plague the outlook on domestic trading activity, with the labour shortage a major constraint. Rising costs for labour and materials are also sapping profitability. But most concerning is the deterioration in investment intentions. That businesses are unwilling to invest in their future is a worrying sign for future economic activity.

We are wary of the growing risks of a recession, both locally and globally. However, the tightness in the labour market may (hopefully) see the Kiwi economy avert a recession, for now.

Nonetheless, demand has outstripped the economy’s productive capacity, and balance needs to be restored. Though signs of slowing demand are emerging, unfortunately it’s not yet enough to prompt a pivot in policy stance. Until there’s a meaningful drop in inflation, the RBNZ’s expected to maintain a hiking bias. We see a further 50bps increase at the November MPS to end the year with a 4% cash rate. But from there, we expect the RBNZ to hold. By November, the cash rate would have been lifted a total of 375bps in just 13 months. We believe the economic pain of such aggressive monetary tightening should be enough to tame the domestic inflation beast. But the risk is clearly tilted to even more tightening if the inflation beast refuses to retreat.

Market reaction was mixed

There was a see-saw reaction in financial markets. Wholesale interest rates markets saw a spike and then a decline. The Kiwi dollar lifted sharply, and then fell back down. The statement was initially seen as much more hawkish. But then traders had second thoughts.

Kiwi swap rates jumped ~5bps immediately following the announcement, only to end up down by around 10bps for a 15bp range.

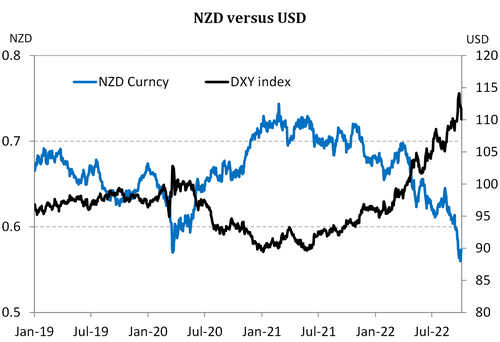

On currencies, mention of “75bps” in the statement hit the NOS button on the NZD. The Kiwi flyer rocketed ~70pts to a high of  58.03c by 2.30pm, The Kiwi has since retreated and lost much of the wind beneath its wings. Against the Aussie dollar, the

58.03c by 2.30pm, The Kiwi has since retreated and lost much of the wind beneath its wings. Against the Aussie dollar, the

Kiwi is looking even stronger. Since the RBA’s surprise 25bps move yesterday, the Kiwi-Aussie cross has been on the rise. And following the RBNZ’s 2pm update, NZDAUD spiked to 88.89c, and remains elevated. Coupling a RBA-slowdown and a committed-RBNZ, we may just have seen the low in the NZDAUD cross. The NZDUSD though…

In recent times, the Kiwi flyer has struggled to gain some airtime. Because with an exceptionally aggressive US Fed and growing recession risks, the Greenback is a gale force wind blowing against the Kiwi dollar (and other commodity currencies). But today’s continued assurance that the RBNZ’s not yet done, helped the NZD climb. But beyond today, risk sentiment and the USD will continue to drive the Kiwi currency.

Global financial markets are highly sensitive to central bank moves. Bears, not bulls, rule equity markets. And bond markets have been savaged by rapidly rising interest rates. For many portfolios, there has been no place to hide. Well, there is one

have been savaged by rapidly rising interest rates. For many portfolios, there has been no place to hide. Well, there is one

place, and that’s the US dollar. The US dollar is a safe haven for many in uncertain times. And as US interest rates rise at a faster pace compared to most other countries (esp. Europe and Japan), money is flooding into US dollar assets. The US Federal reserve is simply more hawkish than most. Other central banks are reacting with rapid fire rate rises. If they don’t, their currencies suffer even more as a result. And that’s inflationary.

RBNZ Statement

The Committee agreed it remains appropriate to continue to tighten monetary conditions at pace to maintain price stability and contribute to maximum sustainable employment. Core consumer price inflation is too high and labour resources are scarce.

Global consumer price pressures remain heightened. The global demand for goods and services is exceeding supply capacity, putting upward pressure on prices. Food and energy prices are being particularly exacerbated by the war in Ukraine.

A recent decline in oil prices and an easing in some supply-chain constraints have seen headline inflation measures fall in some countries. However, core measures of inflation have risen and persist. Central banks are tightening monetary conditions, implying a weaker growth outlook for New Zealand’s trading partners.

In New Zealand, the level of domestic spending has remained resilient to date, in the face of slowing global growth and higher domestic interest rates. Employment levels are high, and household balance sheets remain resilient despite the fall in house prices.

New Zealand’s productive capacity is still being constrained by labour shortages and wage pressures are heightened. Overall, spending continues to outstrip the capacity to supply goods and services, with a range of indicators continuing to highlight broad-based pricing pressures.

Committee members agreed that monetary conditions needed to continue to tighten until they are confident there is sufficient restraint on spending to bring inflation back within its 1-3 percent per annum target range. The Committee remains resolute in achieving the Monetary Policy Remit.