Key Points

- New RBNZ Governor Adrian Orr is expected to play a straight bat at his first MPS, and keep the OCR unchanged at 1.75%.

- We see the RBNZ maintaining the same OCR track and tightening bias. But there is a risk the Bank may postpone the expected tightening cycle.

- We are not anticipating much market reaction to the May MPS, with the RBNZ expected to deliver a fairly neutral statement.

- We maintain our view that policy tightening from the RBNZ is still at least a year away.

Summary

We expect the RBNZ to once more keep the Official Cash Rate (OCR) unchanged at 1.75% on Thursday. The monetary policy statement’s (MPS) updated forecasts are likely to reflect a Bank that is comfortable to sit tight until inflation is well on its way to the doggedly determined 2% midpoint. Given the May MPS is Governor Orr’s first as head of the Bank, he is likely to play a straight bat. Economic developments haven’t changed enough since February to demand too much change. We are still at least 9-12 months away from hitting the RBNZ’s 2% inflation midpoint target.

The May MPS is also the first undertaken in light of the new Policy Targets Agreement (PTA) that includes the dual mandate of price stability and maximum sustainable employment. On its labour market mandate, the RBNZ should be satisfied that it is meeting the spirit of its target. The March quarter Labour market report showed solid employment growth and the unemployment rate fell further to a 9-year low of 4.4%. But although underemployment is moving in the right direction, there is still some slack in the labour force. Wage inflation remains benign. And headline inflation is hugging the bottom of the Bank’s 1-3% yoy target band. The RBNZ saw this coming, as 1.1% yoy inflation is in line with the RBNZ’s February forecast. There is still enough evidence, such as ongoing capacity constraints and tightening labour market, to suggest inflation will return to the 2% midpoint over the medium term, just not the short term. In our view this means that the RBNZ is likely to keep the OCR unchanged for at least another year, and start gradually hiking interest rates from mid-2019.

We expect the RBNZ to recognise that developments since the February MPS have tilted a little towards the downside. As a result, there is the possibility the RBNZ chooses to push out the timing of future OCR hikes by one quarter – from June to September 2019. If this is the case, we would expect a solid market reaction, with both the NZ dollar and short-term wholesale interest rates falling.

Key Developments

There have been a number of notable developments since the RBNZ’s February MPS. But in aggregate, they are unlikely to move the Bank to substantially alter its outlook. The main developments include:

Inflation remains muted for now: Inflation landed near the bottom of the Bank’s target band at 1.1% yoy in the March quarter. But this is unlikely to faze the RBNZ as it was consistent with the February MPS forecast. And there is enough in the data to suggest inflation will increase from here. More recent developments suggest some near-term upside to inflation, particularly for tradables inflation which was particularly soft in Q1. For instance, world oil prices have risen to levels last seen in 2014, with the Dubai spot price currently above US$70/barrel. This has stoked a rise in local petrol prices, but has wider implications for tradables inflation. More recently, the NZD has depreciated, with the trade-weighted index currently down around 1.7% from the RBNZ’s February forecast of 75.0 – although much less as an average over the June quarter to date. If the currency maintains its recent decline, as we believe it will, then there is an added source of upside pressure on imported prices (tradables).

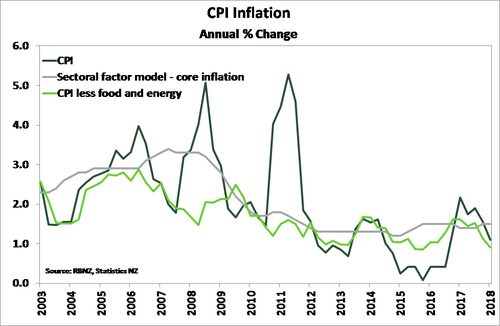

The RBNZ is likely to be more focussed on underlying inflation pressures, however. Inflation expectations remain well anchored, while March quarter data pointed to ongoing subdued underlying inflation pressure – particularly outside of housing-related prices. CPI less food and energy prices fell to 0.9% yoy. The Bank’s own measure of core inflation (the sectoral factor model) came in at 1.5%, still a fair distance from the target midpoint (see chart below). The March quarter private sector labour cost index (LCI) surprisingly printed a paltry 0.3% qoq. As a result the Bank is likely to maintain a cautious outlook. With wages expected to lift over 2018 and capacity pressures becoming more widespread, we expect RBNZ to maintain a similar medium-term inflation track, which shows a slow grind higher toward 2% yoy over the coming few years.

GDP growth still expected to rise: Similar to what was seen in the lead up to the February MPS, the latest release of the GDP fell short of the Bank’s forecast. The NZ economy expanded 0.6% qoq at the end of 2017 compared to the Bank’s 0.8% qoq pick. Annual GDP growth lifted slightly to 2.9% yoy, but remains around trend for the NZ economy. The RBNZ has already somewhat dismissed the poorer GDP outturn in its March OCR review, stating that this was “…mainly due to weather effects on agricultural production”.

Surveys of business confidence suggest that economic growth will remain around trend in the near-term. More recently, business confidence has eased. ANZ’s Business Outlook survey showed firms’ own activity nudged lower in April.

GDP growth is expected to strengthen over 2018, in part due to increased government spending. A strong labour market has been a positive for households. NZ’s elevated terms of trade (ToT) is at record levels. The boost in incomes the stronger ToT provides is expected to support growth. At the start of 2018 the prices for NZ export commodities have strengthened further. The ANZ Commodity Price Index has lifted 5.7% since January in NZ dollar terms.

Global developments pose some downside risks: The global economy has shown ongoing robust growth, although recent data has pointed to an easing in activity over the coming months. Fears of the US Trump administrations’ protectionist trade policy came closer to fruition, with ultimatums laid down to China. These developments remain a risk to future global growth. The US Federal Reserve (Fed) remains on track to deliver at least two more rate hikes in 2018.

Another key global development has been an increase in bank funding costs. US Libor-OIS spreads widened sharply over the first quarter. Rising short-term funding costs have fed through to NZ banks, but less so than other markets such as Australia. There has been limited impact on NZ households to date. NZ banks are less exposed to movements of short-terms funding markets then they once were. Following the events of the GFC, regulators nudged banks toward sourcing more stable long-term funding. In addition, fixed-term mortgage rates have actually come under downward pressure in recent months as the mortgage market remains highly competitive in the face of a subdued housing market. But there is an exposure, and bank funding costs must be monitored for signs of a tightening in financial conditions. The RBNZ always takes into account actual lending rates across the economy, if they rise because funding costs rise, there is a reduced need to lift the OCR.

Statement wording and market reaction

The RBNZ one page statement delivered at the March OCR review still broadly stands today. There is likely to be a few tweaks to recognise the Bank’s employment mandate, the tightening of global financial conditions, and increased protectionist stance seen over the last six weeks. Once again we expect the RBNZ to retain the important final paragraph in the one page statement, specifically “Monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly”.

Market positioning

Markets are currently pricing in the first OCR hike by June 2019. There is unlikely to be much market reaction to the May MPS if the Bank maintains its OCR track. We expect a neutral statement. If the RBNZ decides to push out the timing of rate hikes, thereby signalling it expects to keep the current level of stimulus in place for longer, there may be a sharp market reaction. In this event we would expect to see downward movements in both the dollar and wholesale interest rates on the day of the MPS. We would assign a low, but not insignificant 20% probability to the RBNZ taking this direction.