- The RBNZ hiked the cash rate 50bps to 3%, for the fourth consecutive meeting. This was in line with our view and that of the markets’. The cash rate has been pushed well through neutral (2%) and into truly restrictive territory. The RBNZ reiterated its resolve to break inflation back down to 2%.

- The statement was suitably hawkish, and highlighted the need to maintain pressure on the economy to demand destruct inflation back to target. We now expect the RBNZ to hike to 4%, as we have suggested in recent commentary.

- Financial markets were muted in response. The Kiwi dollar lifted a little, but needs more encouragement. And interest rates lifted a little, as expected. We believe we have seen the peak in wholesale rates.

The RBNZ maintained a determined and resolute policy stance. Inflation needs to fall, and by quite a bit. The central bank’s hawkish commentary highlighted the upside surprises in domestically generated (non-tradables) inflation and the ensuing spike in wages. Although the RBNZ acknowledged the risks from offshore, and the slashing of global growth forecasts, the focus domestically is purely one of destructing demand to break the back of the inflation beast. More rate rises are required for mandates to be met. We have another 100bps of tightening to come.

“Committee members agreed that monetary conditions needed to continue to tighten until they are confident there is sufficient restraint on spending to bring inflation back within its 1-3 percent per annum target range.” (RBNZ August MPS)

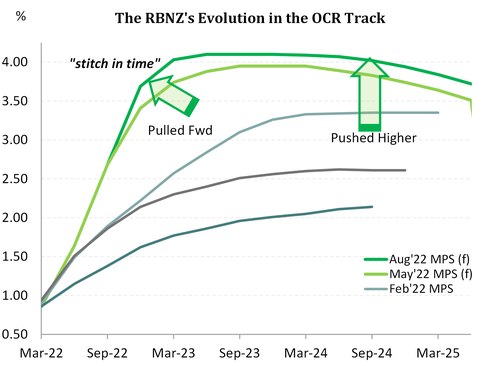

The all-important OCR track – see our first chart – showed a slight increase in the terminal rate from 3.95% to 4.1%. That simply means the central bank is more determined to get the cash rate to 4%, and there’s some risk (10/25) they’ll need to go another step higher. The path of least regrets involves doing more, rather than less, to tame inflation.

We had forecast a peak in this cycle of 3.5%. We believe the RBNZ is getting significant traction from its rate hikes to date. Both business and consumer confidence has been hit, hard, and the housing market is in full retreat. Nevertheless, our job is to forecast what the RBNZ is likely to do. Not want we think they should do. We now expect the RBNZ to hike to 4% in this cycle. We have highlighted this risk in our previews. And we’re becoming increasingly wary of the consequences such tightening will bring. The forward-looking indicators are already showing a significant slowdown is in train. And most outstanding mortgages roll onto much higher rates in coming months. There will be a profound impact on discretionary spending – by design.

We also put a larger weight on international forces. Half of the inflation seen over the last year was generated offshore. Slowing global growth will bring weaker commodity prices. And global shipping costs are falling and so too are waiting times. Tradables (imported) inflation is set to decline quite quickly into 2023.

“The outlook for global growth continues to weaken, reflecting the ongoing tightening in global monetary conditions.” (RBNZ August MPS)

Higher and higher

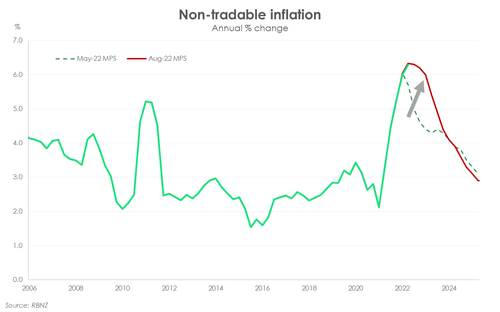

The RBNZ’s MPS came with a new set of forecasts. And inflation was in focus – specifically non-tradables (domestic) inflation. Domestic inflation pressures are strong. The Kiwi economy remains acutely capacity-constrained which continues to  generate inflationary pressure. The RBNZ’s new non-tradables forecasts have been materially upwardly revised, given the higher starting point. The forecast track has also been pushed out, signalling an uncomfortable sense of persistence in today’s rapidly rising consumer prices. Inflation may have peaked at 7.3%. But the RBNZ expects a slow descent from here. Inflation is set to remain above the 1-3% target band until the middle of 2024 – that’s three quarters longer than previously forecast.

generate inflationary pressure. The RBNZ’s new non-tradables forecasts have been materially upwardly revised, given the higher starting point. The forecast track has also been pushed out, signalling an uncomfortable sense of persistence in today’s rapidly rising consumer prices. Inflation may have peaked at 7.3%. But the RBNZ expects a slow descent from here. Inflation is set to remain above the 1-3% target band until the middle of 2024 – that’s three quarters longer than previously forecast.

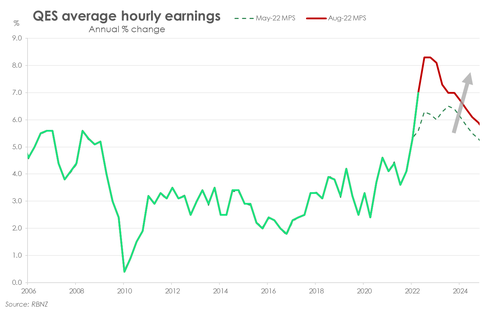

The RBNZ’s expectations for wage growth was also of keen interest. Despite the marginal rise in the unemployment rate, the labour market remains incredibly tight. And that tightness is now translating to rapidly rising wage growth. The private sector Labour Cost Index (LCI) took a step change higher. And large wage hikes appear generally widespread, with over two-thirds of jobs experiencing a pay rise. Rising interest rates and rising living costs will push up wage expectations. The RBNZ made big upward revisions to their  wage growth forecasts. The LCI has further to rise, peaking at 5% by the middle of next year. The RBNZ’s forecast on average hourly earnings – which is a better account of the increases in firms’ salary and wage bills – were also materially upgraded. It is the acceleration in wages that would worry the RBNZ about second round effects of inflation.

wage growth forecasts. The LCI has further to rise, peaking at 5% by the middle of next year. The RBNZ’s forecast on average hourly earnings – which is a better account of the increases in firms’ salary and wage bills – were also materially upgraded. It is the acceleration in wages that would worry the RBNZ about second round effects of inflation.

The lift in domestic inflation and wage growth forecasts support the RBNZ’s hiking campaign. Inflation expectations may have fallen, recently, but they remain too high. The RBNZ would want to see actual inflation clearly and firmly heading south before they consider slowing the pace of tightening.

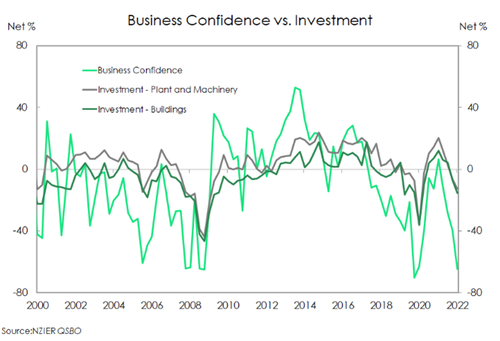

The more the RBNZ tightens monetary conditions, however, the dimmer the economic outlook. Consumer confidence has fallen to recessionary levels. Households are operating in an increasingly expensive environment. High interest rates and high living costs are eating into discretionary spend. And a weaker wealth effect from falling house prices will also weigh on  household consumption in the coming months. Businesses too are feeling downbeat. The ongoing supply-side issues continue to plague the outlook on domestic trading activity, with the labour shortage a major constraint. Rising costs for labour and materials are also sapping profitability. But most concerning is the deterioration in investment intentions. That businesses are unwilling to invest in their future is a worrying sign for future economic activity.

household consumption in the coming months. Businesses too are feeling downbeat. The ongoing supply-side issues continue to plague the outlook on domestic trading activity, with the labour shortage a major constraint. Rising costs for labour and materials are also sapping profitability. But most concerning is the deterioration in investment intentions. That businesses are unwilling to invest in their future is a worrying sign for future economic activity.

The downgrade to the RBNZ’s GDP growth forecasts was acknowledgment of the growing downside risk to the economy. We are wary of the growing risks of a recession, both locally and globally. However, the tightness in the labour market may (hopefully) see the Kiwi economy avert a recession, for now.

Across the Terrace, Treasury are likely to see the impacts of inflation. Stronger-than-expected inflation is likely to be giving the Minister of Finance a bit of a headache too. Like most things, the cost of providing public services is rising rapidly. Public sector salary costs being a major component of the provision of public services. That means the Government may have to spend more in nominal terms, than projected back in the May Budget, just to deliver the same real level of spending. And, as the RBNZ pointed out in the MPS “Any government expenditure above this [May Budget] is likely to require higher interest rates in response, to enable the domestic economy to rebalance and reach a more sustainable pace of growth.”

The market’s reaction was mixed

The reaction in financial markets was muted. The Kiwi dollar lifted, a little, on the announcement, only to reverse later on. The Kiwi dollar looks to be well supported in the mid 63s. We expect the Kiwi to find some legs, as the USD is likely to lose some steam (and flight to safety bid). The same could be said for wholesale interest rates. Wholesale interest rates lifted, a little, on the announcement, but settled without much of a move. Kiwi swap rates have adequately priced the likely path for the RBNZ’s OCR trajectory. And we’d go as far as to say, the market is perfectly priced given the information we have.