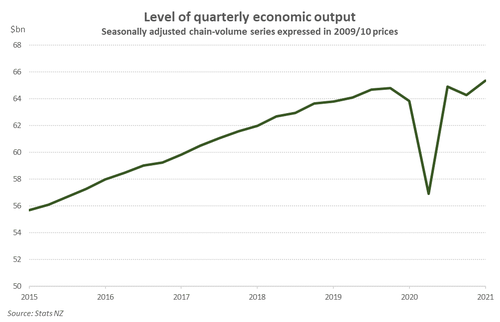

- The Kiwi economy recorded a remarkable 1.6% gain in the quarter. You’d be forgiven for thinking that was the annual rate. But the annual rate was 2.4% - compared to consensus expectations of 0.9%. The economy has confidently returned to pre-Covid levels.

- A solid rebound in construction activity and strong domestic spending have more than offset tourism related losses. And the rampant housing market should continue to fuel momentum in the construction sector. Confidence within the economy has clearly lifted.

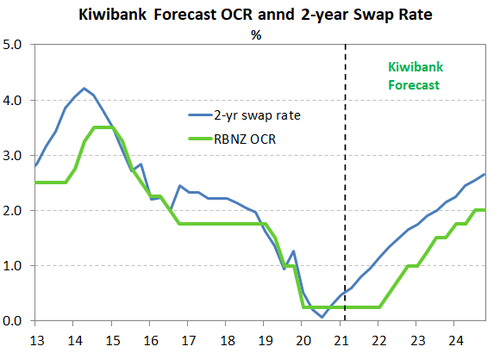

- The whopping 1.6% bounceback came in well in excess of the RBNZ’s forecast of another dip (-0.6%). As the markets digest today’s strong report, we should see expectations shift toward an earlier lift-off in the OCR than the Reserve Bank has schedule. Our forecast May ’22 start date for RBNZ rate hikes looks increasingly likely.

Following the sharp decline in the December quarter, the Kiwi economy rebounded 1.6%. We’ve more than dodged a double dip recession. We’ve outrun it. A solid rebound in construction activity and strong domestic spending have more than offset the loss of international tourism typical over the summer period.

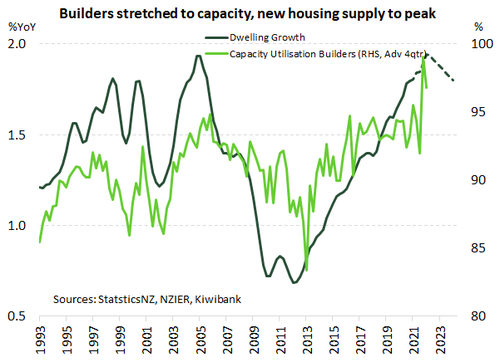

We are spending and building our way out of the hole that covid created. Household consumption was surprisingly strong. Household confidence has grown, and the inability to travel offshore has funnelled spending locally. The strength in consumption was reflect a healthy labour market, also. Construction was the largest contributor to growth in the quarter, adding 0.4%pts to overall growth. Much of the jump was driven by residential construction, as the building industry responds to our chronic housing shortage. Residential construction has also been fuelled by record low mortgage rates and rapid house price gains. Building consent data indicate that construction will continue to underpin growth this year – so long as we have the tradies to do the work. The best, positive, surprise was the lift in business investment. Confidence has returned to SME business.

Today’s report exceeded our best guesses, and showed the Kiwi economy survived the summer without tourists. So we begin the year on a much firmer footing. Looking ahead, the recovery in economic activity is expected to continue in the June quarter. Annual numbers will look particularly plump given the base effects in play, when the economy shrank a record (revised) 11% this time last year.

The closed border will continue to distort the picture. But the Aussie bubble is certainly helping. The rampant housing market should fuel momentum in the construction sector. However, it may be harder for industries already bumping up against capacity constraints - including construction and manufacturing - to eke out growth given the ongoing supply chain disruptions. The demand is there, but supply is harder to pin down in this covid world. Until the issues at the ports are resolved, shipping delays might see these industries post softer growth in the coming months.

In terms of the interest rate outlook, the 1.6% came in well in excess of the Reserve Bank’s forecast of another quarterly dip (-0.6%). As the markets digest today’s strong report, we may see expectations shift toward an earlier lift-off in the OCR than the Reserve Bank has scheduled. If data continues to paint a healthy picture of the economy, our May ’22 hike start date looks increasingly likely. One key downside is of course another covid community outbreak. Until herd immunity is achieved, the primary threat to the Kiwi economy will continue to be an outbreak of the virus, necessitating a tightening in alert levels.

From our viewpoint, all wholesale interest rates look too low. And the Kiwi currency looks very low. We expect to see a strong lift in both interest rate expectations and the Kiwi dollar from here.

We were eager to see this report. And it was well worth the wait!

Serving up a stonker!

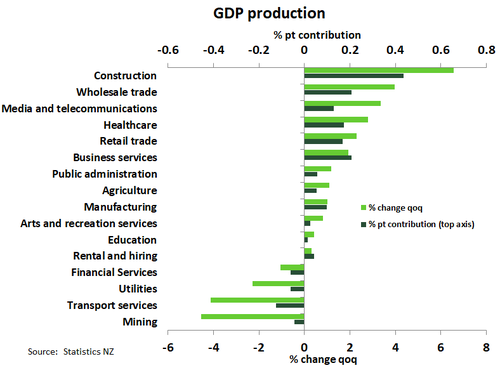

The Q1 snapshot of the Kiwi economy makes clear that the recovery is becoming more broad-based. All main industry groups rose in the 3 months to March. And services industries led the charge, with the 1.1% rise in the quarter, making up for majority (0.8%pt contribution) of overall growth. Service industries account for two-thirds of the economy and benefited from the solid demand for all “things”. For instance, wholesale trade was propelled 4% due to demand placed on machine and equipment wholesaling and vehicle wholesales. Global supply-chain disruption is likely to throw things around in wholesale trade in the coming quarters. Retail trade and accommodation also made a decent contribution to services. As discussed below households were out in force and spending over summer. Not all service industries reported such solid numbers. Transport services, which has faced the brunt of covid disruption fell 4.1% in the quarter and was still 24.2% below the level of activity in the March quarter last year as NZ was about to go into lockdown.

Overall, goods industries expanded 2.4% partly rebounding from the 3.1% fall the previous quarter. Massive domestic demand for housing meant construction activity jumped almost 7% and as expected was the largest single contributing industry to GDP growth (see chart above). And StatsNZ noted that the level of building activity is back near all-time highs. The surge in home building is helping to address NZ’s significant housing shortage. Also adding support to home building has been record low mortgage rates and a booming housing market. Building consent data indicate that construction will continue to underpin growth this year – so long as we have the tradies to do the work. Labour shortages are hindering some work in the construction sector and may mean the 1%+ rates of GDP growth expected in the coming quarters may be hindered. Supported by strong construction activity and the lift in plant and machinery investment also saw manufacturing post a 1% quarterly gain.

Overall, goods industries expanded 2.4% partly rebounding from the 3.1% fall the previous quarter. Massive domestic demand for housing meant construction activity jumped almost 7% and as expected was the largest single contributing industry to GDP growth (see chart above). And StatsNZ noted that the level of building activity is back near all-time highs. The surge in home building is helping to address NZ’s significant housing shortage. Also adding support to home building has been record low mortgage rates and a booming housing market. Building consent data indicate that construction will continue to underpin growth this year – so long as we have the tradies to do the work. Labour shortages are hindering some work in the construction sector and may mean the 1%+ rates of GDP growth expected in the coming quarters may be hindered. Supported by strong construction activity and the lift in plant and machinery investment also saw manufacturing post a 1% quarterly gain.

Primary industries recorded a solid 0.3%qoq rise. The bounceback in agriculture and forestry however were partially offset by falls in mining.

falls in mining.

Overall, we’re encouraged to see growth across all industry groups.

Kiwi were out in force and spending over summer

Just like production, the consumption measure of GDP also blew any predictions out of the water. The economy expanded 1.4% in the quarter and showed clearly the contribution made by a surge in domestic demand. Strong domestic spending has astoundingly offset the loss of activity typically gained from international tourism this time of year. Indeed, the inability of Kiwi to travel overseas may explain the strength in consumption since leaving the autumn lockdown. Swapping a trip to Europe for a brand-new lounge set. Expenditure GDP in the year to March was just 0.4% below the level seen the 12 months prior.

Last year’s fiscal support, record low interest rates, and improved confidence around job security was unleashed in a 5.5% jump in private consumption. Kiwi were more than happy to travel and explore Aotearoa over the summer. Spending on accommodation and eating out lifted 2.2% and is likely to have eased some of the pain on tourist operators from the absence of foreign tourists. Also, the built-up in savings over last year look to have been directed at upgrading the car and buying all sorts of new toys. Household spending on durables expanded almost 9% in the quarter and follows a slight breather in the Q4.

Mirroring the jump in wholesale trade and residential construction, investment activity skyrocketed at the start of 2021. Investment expenditure grew 6.4%. Encouragingly, a key driver was a massive jump in spending on plant and machinery and transport equipment. But the uncertainty of last year’s disruption from covid on firms’ investment decisions is still evident in the numbers. On an annual average basis gross fixed capital formation was still almost 5% down.

Disruption to the flow of trade and people across our border was the main drag on expenditure GDP growth in the quarter. Exports were hit by an 8% fall focussed on services exports. The starkest evidence of the damage done by the necessity of closing our border. From the June quarter we expect to see improvement in export services as the trans-Tasman bubble allows for the flow of people from our largest tourism market – Australia. Imports, to feed the insatiable domestic demand, jumped 7.1% in the March quarter, and were also a drag on GDP.

Closed border continues to distort the picture

Today’s report blew every forecaster’s best guesses straight out of the water - the Kiwi economy survived the summer without tourists. So we begin the year on a firmer footing. Looking ahead, the recovery in economic activity is expected to continue in the June quarter. Annual numbers will look particularly plump given the base effects in play, when the economy shrank a (revised) record 11% last year. However, the Q1 print may take some of the shine off the June quarter.

Near-term bumps are expected as the closed border continues to distort the picture. Continued absence of foreign visitors means industries reliant on our service exports – tourism and education – will continue to struggle. On the other hand, the rampant housing market should fuel momentum in the construction sector. However, it may be harder for industries already bumping up against capacity constraints - including construction and manufacturing - to eke out growth given the ongoing supply chain disruptions. The demand is there, but supply is harder to pin down in this covid world. Until the issues at the ports are resolved, shipping delays might see these industries post softer growth in the coming months.

Nonetheless, the Kiwi economy continues to outperform. The Q1 print came in well in excess of the Reserve Bank’s forecast of another quarterly dip. As the markets digest today’s strong report, we may see expectations shift toward an earlier lift-off in the OCR than the Reserve Bank has schedule. If data continues to paint a healthy picture of the economy, our May ’22 hike start date looks increasingly likely. One key downside is of course another covid community outbreak. Until herd immunity is achieved, the primary threat to the Kiwi economy will continue to be an outbreak of the virus, necessitating a tightening in alert levels.

Market Reaction

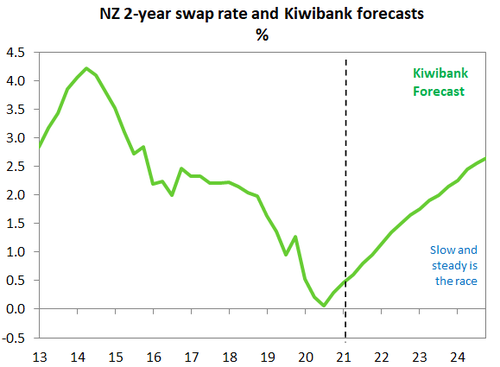

Wholesale interest rates were propelled higher, following the report. The pivotal 2-year swap rate jumped 7bps to 0.62%. But it was the belly of the Kiwi curve, the 5-year, that was catapulted 13bps to 1.32%. The 10-year also lifted 5bps to 1.95%. All of these wholesale interest rates look low to us. And we forecast a steep upward trajectory from here.

Although our rates look low, our currency looks even lower – based on our fundamentally driven forecast. The Kiwi dollar hardly reacted to today’s news. At 0.7065, the Kiwi is nearly a cent lower than yesterday’s close on a stronger USD. We see the Kiwi lifting to 0.73 near term, and we expect the Kiwi to hit 0.77 by year end.

Market traders have displayed great resistance to reflation trades in recent weeks. Despite an array of positive economic data prints, across the globe, interest rate markets are firmly bid. Until last night, the US 10-year had held under 1.5%. Interest rates, globally, do not adequately reflect the inflation risk that’s building, or the growth that we are seeing. And then there’s the lack of term premium. In our view, interest rates will push higher, much higher, into year end. And Kiwi rates are flying at a higher  altitude. Following the RBNZ’s hawkish tilt in the May MPS, we changed our forecast rate hike cycle to May 2022, with 3 full hikes forecast over 2022. Our forecast trajectory is the most assertive in the market, to our knowledge. Today’s report supports our view. If anything, there’s a growing risk of an earlier move from the RBNZ in February next year.

altitude. Following the RBNZ’s hawkish tilt in the May MPS, we changed our forecast rate hike cycle to May 2022, with 3 full hikes forecast over 2022. Our forecast trajectory is the most assertive in the market, to our knowledge. Today’s report supports our view. If anything, there’s a growing risk of an earlier move from the RBNZ in February next year.

Looking at international rates, the Kiwi market is too low, but much more sensible than the Aussie market. We struggle to see a world where the RBNZ is in the position to hike next year, and the RBA still refuses to hike until 2024. Positioning for higher rates in Kiwi markets makes sense. But shorting the Aussie market makes even more sense.