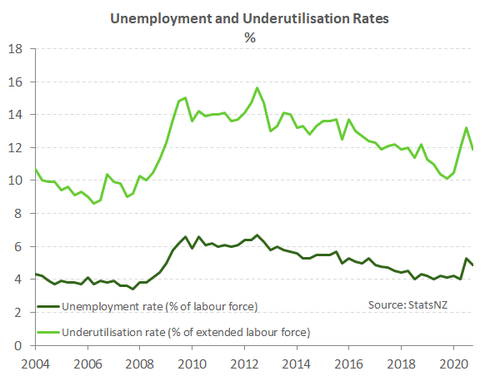

- The unemployment rate ended 2020 at just 4.9%, compared to KB’s estimate of 5.4%, and consensus of 5.6%. And the outlook for 2021 is much better.

- A shallower peak in unemployment means we will have less economic scarring. And the sharp bounceback in hours worked means we will see higher than expected consumption across the economy.

- The construction industry employed an extra +13,200 people in the quarter. This is precisely what we want to see. This is a fantastic read.

- When considered against the rampant housing market, the RBNZ has little choice but to keep the cash rate unchanged, and do more to restrain the exuberance in the housing market.

The labour market IMPROVED in the December quarter, against expectations of a slight deterioration. The unemployment rate dropped to 4.9%. Although we still expect the unemployment rate to peak a little higher in the first half of 2021. REDUCED slack in the market was also seen in the fall of the underutilisation rate to below 12%. We’ve seen a sharp FALL in the number of people out of work, or wanting more hours to work.

Today’s report was truly remarkable.

Annual wage growth slowed a little, however. Broad-based measures of inflation are mixed. And wage growth has cooled in a highly uncertain Covid world. Companies are battling supply disruptions, surges in costs, and a dearth in foreign visitor demand. That said, we’ve found ourselves in a much better place. There’s nowhere else you’d rather be in the world right now. And the labour market data reflects the resilience of the Kiwi economy. Since bouncing out of lockdown, our economy has outperformed most developed economies around the world.

It could have been much worse, and it’s unlikely to get much worse. A 4.9% unemployment rate is a remarkable result, considering the earlier estimations of a move towards 10%. Provided we make our way through 2021 without any major lockdowns, or economic disruptions, we’re firmly fixated on the light at the end of the Covid tunnel. Statistics on Covid cases will (hopefully) be overwhelmed by statistics on Covid vaccinations. And, all going well, the Kiwi economy should record a solid 3-4% growth rate this year.

It could have been much worse, and it’s unlikely to get much worse. A 4.9% unemployment rate is a remarkable result, considering the earlier estimations of a move towards 10%. Provided we make our way through 2021 without any major lockdowns, or economic disruptions, we’re firmly fixated on the light at the end of the Covid tunnel. Statistics on Covid cases will (hopefully) be overwhelmed by statistics on Covid vaccinations. And, all going well, the Kiwi economy should record a solid 3-4% growth rate this year.

The diminishing downside risks to the labour market, have diminished the downside risks to the housing market. So, the national exuberance in housing will continue. Reinstated LVR restrictions will do some of the work in slowing the rampant run rate. But more creative solutions will be required to truly tame the beast. On the demand side, we’ve highlighted the need to better price the risk of different home loans – see here. But it’s not a demand problem, in our view. The true problems are firmly on the supply side. And any slack we see developing in the labour market should be enticed into housing development…

A recovery built on construction

The number of people employed rebounded 0.6% in the December quarter, following back-to-back declines due to covid. Employment was 0.7% up on December 2019. StatsNZ pointed out that at an industry level, the impact of covid was felt by the tourism and media industry last year. However, these soft spots were offset by increased jobs in a construction sector fuelled by a new infrastructure spending, a housing shortage, a rampant housing market and record low mortgage rates. There were around 20K more people employed in the construction sector at the end of 2020 compared to a year earlier. In comparison, retail and accommodation and information media industries lost about the same number between them.

The number of people employed rebounded 0.6% in the December quarter, following back-to-back declines due to covid. Employment was 0.7% up on December 2019. StatsNZ pointed out that at an industry level, the impact of covid was felt by the tourism and media industry last year. However, these soft spots were offset by increased jobs in a construction sector fuelled by a new infrastructure spending, a housing shortage, a rampant housing market and record low mortgage rates. There were around 20K more people employed in the construction sector at the end of 2020 compared to a year earlier. In comparison, retail and accommodation and information media industries lost about the same number between them.

Without any extensive lockdown anywhere around the country in the December quarter, actual hours worked jumped 4.5% in the quarter to be almost 4% higher than the same quarter last year. The Quarterly Employment Survey (QES) of firms revealed that total weekly paid hours also lifted 1.3%qoq. Paid hours were far less affected by covid over 2020 due to the Government’s wage subsidy keeping many in paid employment. But importantly, the rise in paid hours is a positive sign for Q4 GDP growth figures when they are released next month.

The strong rebound in activity over the second half of last year looked to have enabled people to up their hours of work too. The number of people underemployed – those that work part-time but would like to up their hours – dropped 18k.

From tour guide to tradie

Since the initial nationwide lockdown in March last year, NZ women have lost jobs and hours at a greater rate than men. The June quarter revealed the disproportionate blow of shutting down the country on women. Women accounted for 90% of the quarterly drop in employment. Six months on, and it appears that things are getting better. The unemployment rate fell for both men and women (4.5% and 5.4%, respectively), with about 5,000 fewer men and women unemployed. The underutilisation rates fell also. And quarterly employment growth was a touch stronger for women, with 10,000 more women employed (7,000 more men).

So on a quarterly basis, men and women appear to be recovering from the lockdown on an equal footing. But when we compare today’s labour market with that of a year ago, the asymmetry is clear. There are 25,000 more people unemployed than in the December 2019 quarter. And of that, 60% are women.

The ongoing border restrictions continue to take a toll on female employment, in particular. Annually, 5,700 fewer women were employed in the travel agency services, and 11,400 fewer in administrative and support services industry.

In contrast, the emphasis on construction as our post-covid recovery strategy has seen increases in related jobs. But these construction opportunities are dominated by job opportunities for men. The survey showed an annual increase of 21,000 people whose main job was in the construction. And of this increase, 15,200 were men and 5,800 were women.

The details of the report are even dicier when we dive into the demographics. The latest figures show that the groups hit hardest by covid - young, Maori and Pasifika - are no better off. The annual unemployment rate rose from 7.2% to 9.0% among Pasifika, and remains unchanged among Maori. They’ve been displaced, and are yet to be picked up elsewhere.

Those that have become unemployed may look to be re-deployed into other industries seeking workers, notably in infrastructure. But it’s not as easy for a tour guide to drop the speaker phone and pick up a shovel. More is needed toward the re-training needs of our most vulnerable. Govt support is needed to limit the number of those dropping out of the labour force. Our Tasman neighbour seems to have the formula right. The Australian Govt Government introduced the “JobMaker Hiring Credit” – a programme designed to provide businesses with an incentive to take on employees aged between 16-35 years. There’s no reason we can’t introduce the same here. It would provide our most vulnerable a way back into the labour market.

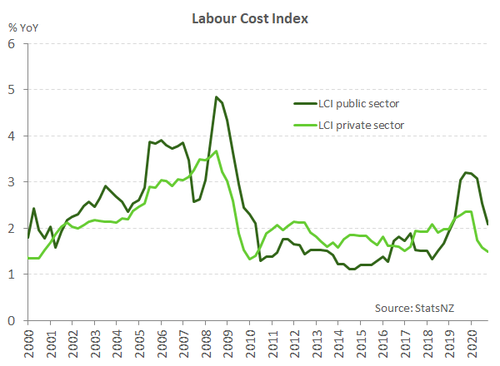

Wage growth eases a little further

Wage growth, as measured by the private sector Labour Cost Index (LCI), lifted 0.5% in the quarter leading annual wage inflation to ease 0.1%pts to 1.5%. Annual wage growth peaked at 2.4% a year ago and has pulled back as a result of the coronavirus hit.

The remaining slack in the labour market will likely keep a lid on underlying wage growth over 2021 – even with a minimum wage heading to $20/hr in April. The unemployment rate is still not indicative of full employment across NZ’s labour market. And the underutilisation rate, despite falling in the quarter, remains around 1½%pts above pre-covid levels. However, the faster-than-expected recovery is likely to see labour market slack be absorbed much sooner, leading to rising wage inflation on the horizon.

While today’s report is welcome, we are yet to believe that the unemployment rate has peaked in the current cycle. Assuming NZ doesn’t experience another major covid lockdown situation, we expect the unemployment rate will peak closer to 6% over the first half of 2021. Pain from an absence of visitor arrivals is still being felt. Nevertheless, a 6% unemployment rate peak would be a remarkable outcome.

Market Reaction

The reaction to the remarkable report was reliably well reasoned. The Kiwi currency was catapulted higher. The Kiwi jumped from 0.7160 to 0.7192 against the big (US) dollar, and leaped from 0.9420 to 0.9460 against the Aussie dollar. We continue to forecast a stronger Kiwi currency over the year ahead. We’re picking 0.75c against the USD by year-end.

Wholesale interest rates are higher across a far steeper curve. Risk of rate cuts have been replaced by risks of rate hikes! And as soon as next year. The Kiwi rates market has gone from pricing in a negative cash rate, just a few months ago, to rate hikes beginning in the middle of next year. It all comes down to the RBNZ’s communication on 24th February. The RBNZ should remove their ‘optionality’ around negative rate policy, but cap market expectations of rate hikes. A return of the OCR track will do the trick. We’d expect the RBNZ to signal an unchanged OCR well into 2022 (possibly 2023) at this stage, to restrain the rise in wholesale interest rates. The RBA signalled an unchanged cash rate, into 2024! It’s about time we took out the downside risks. But it’s not yet the time to talk up the upside risks. That’s a game plan for next year (we hope).