Key Points

- Despite a recovery in activity, firms remain pessimistic about the general economy.

- However, a net 15% of businesses experienced an increase in their domestic trading activity – consistent with GDP growth coming in around trend at the start of 2018.

- Firms still seem to be reluctant to pass on rising costs to customers, suggesting inflation is likely to remain subdued in the coming quarters.

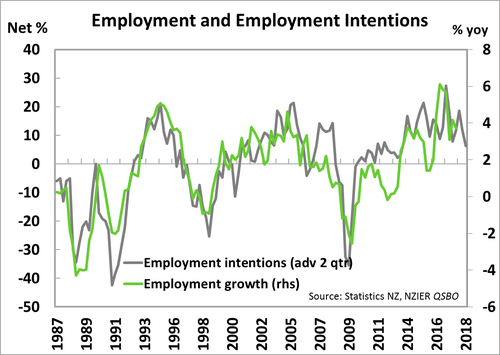

- Hiring intentions fell to a five-year low, with a net 6% of firms expecting to lift headcount over the June quarter.

- Today’s QSBO is likely to be viewed as supporting the RBNZ’s decision to keep the OCR unchanged for some time. We maintain our view the RBNZ will begin gradually hiking the OCR from May 2019.

Summary

Firms look to be stuck in a bit of a funk at present, despite demand recovering. NZIER’s Quarterly Survey of Business Opinion (QSBO) revealed a net 9% of firms were pessimistic about the general economy in the first quarter of the year, a slight improvement on the net 11% of pessimists in the December quarter. However, the downbeat view of the overall economy is perhaps more symptomatic of the bias shown in business confidence surveys against labour–led governments. When looking at firm’s domestic trading activity the QSBO presented a rosier picture. A net 15% of business experienced an improvement in trading activity at the start of 2018, versus a net 10% in December, and supports our view that GDP growth look likely to remain around trend of 2.5-3.0% yoy at the beginning of 2018. Once again the QSBO highlighted an ongoing puzzle: while a notable share of firms have experienced rising cost pressures, few are willing to pass these on by lifting prices. The net result of this ongoing conundrum looks to be a hit to firms’ profitability.

The caution illustrated by headline confidence may have fed through to business decisions. For instance, employment intentions fell to their lowest level in five years, with a net 6% of firms expecting to add to headcount in the next quarter. The result is still above the survey’s average level, but indicates that employment growth will cool over the coming quarters.

In terms of monetary policy, the RBNZ is likely to see today’s QSBO as supporting their view on inflation and justifying their current cautious approach. The fact that firms continue to look reluctant to hike prices in the face of rising costs is perhaps indicative of the structural changes that the RBNZ has highlighted as influencing price setting behaviour. These include globalisation, technological changes and increased competition amongst firms. With the RBNZ now also tasked with “…supporting maximum sustainable employment within the economy”, the fall in employment intentions may garner some attention. However, this would depend on the nature of the decline in hiring intentions. It currently looks as though firms’ may simply be unable to add to headcount because of the tight labour market.

Pessimism looks to be feeding through to business decisions

The downbeat mood of firms might have started to influence business decisions. There was a further fall in investment intentions in buildings with a net 1% of firms looking to divest in buildings – the first net decline since late 2012. In contrast, there was an increased share of firms looking to invest in plant and machinery. However, what stood out was a decline in hiring intentions. A net 6 % of firms are looking to increase headcount over the June quarter, which is the lowest level seen in five years (see chart below).

The declines in hiring intentions were most acute in the construction and services sectors. While firms’ cautiousness is likely to be influencing hiring decisions, an element of this result looks to be related to capacity constraints and difficulty in finding labour. Once again the main constraint to increased sales turnover among builders is labour. For the services sector, a net 4% of businesses expect to increase staffing, down from a net 13% in the previous quarter. Capacity constraints look to be building in the services sector, (capacity in the services sector is inextricably linked to people) which has for some time experienced solid growth.

Follow what I do and not what I say

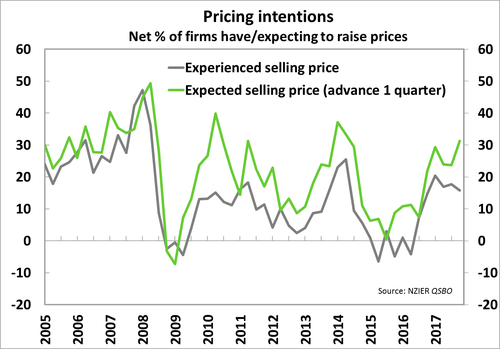

Today’s QSBO once again highlighted the puzzling situation, in which firms continue to point to rising cost pressures but are unable or unwilling to pass these costs onto customers. An increased share of firms (net 31%) experienced a lift in their average costs in the March quarter, the highest share since early 2013. In contrast, only a net 16% of firms actually increased prices over the quarter, and that was despite a net 31% in the December 2017 quarter indicating they were intending to hike prices at the start of 2018.

There is clearly something at play here, and for some time now firms have signalled bold intentions on pricing but not followed through. As the chart below shows, since the GFC there has been a distinct wedge between firms expected and experienced pricing decisions. This wedge supports some of the commentary coming out of the RBNZ around structural shifts in firms’ price setting behaviour. There are a number of factors proposed for this shift. For instance, the rise of the gig economy (including the likes of Airbnb and Uber) and large global online retailers have indirectly lowered inflation via increased competition in their respective industries. In addition, the emergence of globalisation as a driving force has streamlined global supply chains and driven down the cost of international trade. These issues may get coverage by RBNZ Governor Adrian Orr on Thursday April 12 in a speech entitled “Inflation targeting in New Zealand: an experience in evolution”. All told, the sluggishness seen in pricing behaviour supports the RBNZ’s current cautious approach to monetary policy and supports our view that the Bank will keep the OCR unchanged at 1.75% for some time, and begin gradually hiking from May 2019.

There was still enough in the March QSBO to suggest that inflation is set to rise over the year ahead. Capacity utilisation lifted almost a percentage point to 93.5%, driven by increased utilisation across both builders and manufacturers.

Builders and retailers are among the most pessimistic

A general sense of pessimism permeated through all the industries captured in the QSBO. Business confidence actually worsened in the construction sector with a net 7% of builders being downbeat around the outlook of the general economy, compared to a net 2% in the previous quarter. A drop in the share of builders that experienced a rise in new orders may be to blame. However, the QSBO still indicated that there remains a substantial pipeline of building work to get through in the NZ economy. For instance, a larger share of architect’s now expects an increased workload over the coming 12 months. Retailers remained in the doldrums, and NZIER noted that recent government policy changes that disproportionately hit the retail sector might be to blame. Policy changes include: the hike in the adult minimum wage to $16.50/hr, and the scrapping of the 90-day trial for new workers for firms with over 20 workers.