Risks, risks everywhere and not a cut to ink.

The RBNZ deflated their forecasts, pushed out their hikes, and reiterated all the risks – up and down.

The RBNZ’s MPS raised a few key points

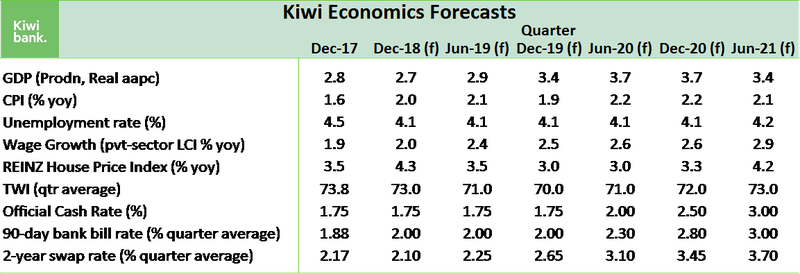

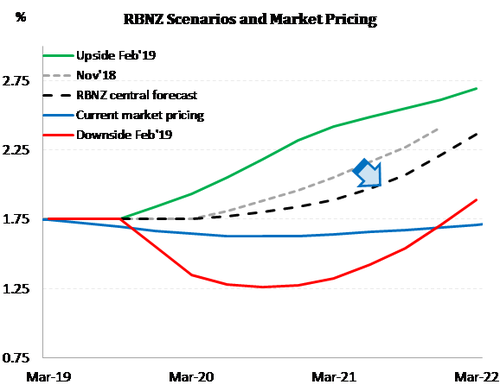

- The OCR is likely to remain at 1.75% for longer, with the RBNZ’s forecast rate hikes pushed out into 2021.

- There are both upside and downside risks.

- The message to households and businesses remains clear: don’t fear rising interest rates. The RBNZ will keep rates low, beyond the foreseeable future.

- We too have pushed out our forecast interest rate trajectory, well beyond the near-term. All going well, we should see a hike in 2021. All going not-so-well, well, we’ll see cuts (plural).

“We hold for a long period. The next move could be up or down”. Adrian Orr

Following other central banks around the globe, the RBNZ today postponed thoughts of rate hikes. The (in)action and all-too-similar language within the Monetary Policy Statement (MPS) failed to meet the dovish expectations in financial markets. The OCR remained at 1.75%, that wasn’t in any doubt, while the Bank pushed out the timing of future rate hikes to address a worsening outlook. The risks around the outlook were “symmetric”, up and down.

When asked: Has the chance of a rate cut increased? Orr said “No”. But the cash rate may stay at this level (1.75%) for longer.

The MPS included a Box (E) on the introduction of higher bank capital requirements. Orr noted that the impact on financial conditions should be “lost in the wash”. The RBNZ estimates a 20-40bp increase in bank margins to recover the high cost associated with higher capital. But the central bank assumes there will be “many offsetting forces” including a “safer” financial system and potentially healthier sovereign rating. Orr said he “seriously struggles” with the UBS study, that concluded there would be an 80-125bp increase in bank margins. Orr said: “We don’t at all buy in to that story… Well capitalised banks can lend more. The return on equity is incredibly strong, and above and beyond the risk they (banks) are taking… if the risks have declined, so too should the required return on equity”.

The comments were a firm (warning) guide to the lower end of bank expectations, seen between 40-120bps, with an expectation that impacts will be spread over 5-years. Of course, the Box did note: “If additional support to demand is required during the potential transition to higher levels of bank capital, monetary policy would be able to respond as needed. This will be assisted by the proposed long transition period.” Sensible…

The RBNZ stops short of the (more) dovish statements delivered elsewhere

Since the RBNZ’s November MPS, momentum in the global economy has slowed. For instance, economic growth in China is slowing faster than expected, and in the Eurozone the budding economic recovery of 2017 has all but petered out. In addition, we have seen a shift in positioning from a number of central banks in recent weeks. The US Federal Reserve (Fed), European Central Bank (ECB) and Reserve Bank of Australia (RBA) look to have taken on a wait and see approach, side-lining thoughts of monetary tightening.

But the RBNZ maintained a more neutral stance that was similar in tone to the November MPS. Of course, today’s statement was underscored by concerns around the global outlook. “Trading-partner growth is expected to further moderate in 2019 and global commodity prices have already softened, reducing the tailwind that New Zealand economic activity has benefited from… The risk of a sharper downturn in trading-partner growth has also heightened over recent months.” But this outlook hinges on unresolved decisions that could fall in any direction. These include ongoing US-Chinese trade discussions, an unresolved dispute in Washington DC over the US Federal budget, and an outright messy Brexit.

Capacity pressures continue to bubble just under the surface

The RBNZ remains on guard for possible price hikes. Because firms face significant capacity pressures and narrowing margins. Rising labour costs from large minimum wage hikes are just one example. And business sentiment surveys and labour market figures point to continued pressures. But for now, firms remain hesitant to pass these higher costs on in the face of fierce (explicit and implicit) competition. In addition, firms’ price setting behaviour has become more backward looking. As inflation gradually picks up, so too will pricing actions from firms, rather than firms responding to expected increases in costs.

A modest pass through of cost pressures are incorporated into the RBNZ’s inflation track. In the Bank’s view inflation is expected to reach the middle of the 1-3% target band by the end of 2020 – this is around six months later than their November forecast. The RBNZ uses an upside scenario to highlight the potential risk if firms pricing behaviour changes, and cost pressures are delivered more rapidly.

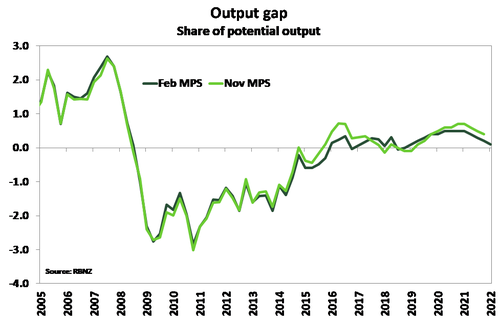

The economy has been running around its long-term sustainable level for a few years. As growth lifts this year, so too will inflation. The RBNZ lowered its GDP growth forecasts over the forecast period. However, the bank also lowered its forecast of potential growth, based on recent data. Lower potential growth means the economy needs a lower rate of growth to generate domestic inflation, and the output gap forecast is not much changed. GDP growth is expected to peak at a little over 3%yoy in the second half of the year.

Risks are tilted to the downside despite balanced scenarios

At the MPS press conference RBNZ Governor Orr assured markets that risks are symmetric, up or down. Once again, the upside scenario hinged on the risk of faster passthrough of cost pressures by firms. In the Bank’s view this would illicit 50bps of hikes over and above the central OCR track. The downside scenario was based on a deteriorating global outlook – it had to be really! Softer global growth would likely dent NZ export growth, hurting consumer and business confidence. The Bank signalled that under this scenario it would respond with 50bps of cuts below the central track.

Oh we love beautiful symmetry.

Market Reaction.

The risks the RBNZ delivered were “symmetric”. Market participants had positioned for a significant shift in the RBNZ’s bias. The probability of rate cuts had increased in interest rate markets, and the Kiwi dollar had eased into the announcement. Without the delivery of an explicit easing bias, the Kiwi dollar shot higher and Kiwi interest rates bounced. The Kiwi dollar lifted from 0.6730 to 68.50 (a big figure move). Kiwi swap rates lifted 6-8bps. On Kiwi interest rates, the 2.16% on 10-year Government bonds was deemed as “too low” by Governor Orr. And he said a 2% rate does not accurately reflect the likely growth and inflation outcome over the next 10 years.