- The RBNZ’s latest FSR: NZ’s financial system is sound and “remains resilient to a broad range of economic risks”.

- As expected, there were no changes to current LVR restrictions. But the RBNZ is on watch to loosen them if conditions allow.

- An interesting theme of the FSR was the impact of climate change. The costs are very real.

- The RBNZ reiterated its desire to raise bank capital requirements to improve financial system resilience to a shock.

Today the RBNZ released its latest Financial Stability Report (FSR), and rest assured the NZ’s financial system is sound and “remains resilient to a broad range of economic risks”. The NZ financial system is vulnerable to high household and dairy farming indebtedness, and global risks to our main trading partners – these risks haven’t changed since the last FSR produced back in November. And then there’s climate change.

LVR restrictions unchanged

As expected, the RBNZ sat on Loan-to-Value (LVR) restriction settings. Vulnerabilities in the financial stability have not materially changed since the November FSR. And there have only been a handful of months since LVR’s were last loosened from 1st January. The RBNZ continues to review the data. There may be a case to loosen LVRs again later in the year, but this will be “…subject to continuing subdued growth in credit and house prices and banks maintaining prudent lending standards.”

Housing-related credit growth has been well behaved for some time now, because the housing market has cooled. Credit growth is hovering around 6%yoy, which is substantially down from the recent peak of 18%yoy back in 2015. However, the RBNZ notes credit growth continues to exceed household income growth. Moreover, the recent falls in mortgage rates, and the Government ruling out a comprehensive CGT could stoke higher credit growth. It’s a watching brief then.

The main, and immediate, risks are also unchanged

The RBNZ reiterated the vulnerabilities of the financial sector. Households and dairy farmers have significant levels of indebtedness, and risks to our trading partners remain elevated.

Global risks are a key concern. Since the last FSR in November, forecasts of global growth have been lowered. China, our largest trading partner, is embroiled in a trade dispute with the US. Across the ditch, the Australian housing market has faced a correction and the RBA is poised to cut the cash rate to 1% (or below), in our view. The RBNZ highlighted the concern that among developed nations there is less ammunition to throw at an economic crisis. Many major central banks are at or near lower interest rate bounds, and many Central Governments have elevated debt levels (not a New Zealand story).

Locally, the high level of household indebtedness continues to worry the RBNZ, particularly households with mortgages. The Debt-to-Income (DTI) ratio is at all-time highs and means highly indebted households are vulnerable to adverse shocks. But overall financial sector resilience to household debt has improved. Lending standards are tighter, and macro-prudential policy has meant that the quality of bank assets is higher. A silver lining in the recent falls seen in Auckland house prices is the reduced “…likelihood of a large and disorderly price fall”.

The farming sector, particularly dairy, is also a pressure point. The dairy sector remains highly indebted. However, this risk is concentrated in a small percentage of farmers. Lenders may need to reprice the risk posed by these farmers. Climate change is an added risk…

The RBNZ used the FSR to reiterate its desire to raise bank capital requirements. This work is ongoing, with recent submissions on proposed changes being reviewed. A final announcement on changes to capital requirements is expected at the end of the year. The outcome is likely to raise the cost of funds for banks. The debate remains by how much, and who will pay (shareholders or customers or both).

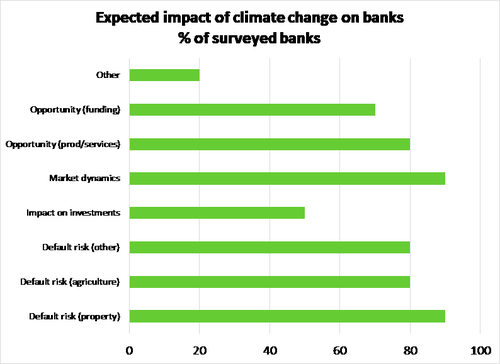

The costs of climate change are real

An interesting theme of the FSR was the longer-term risks to the financial sector that need to be considered – namely climate change. What is clear is that the future threat of climate change is having an impact on the financial system today, mainly via insurance. Consequently, we will all pay more to maintain a sound and efficient financial system in the future.

The RBNZ noted two main concerns. First, insurers have been moving to more risk-based pricing, customers highly exposed to natural disasters will or are pay higher premiums. Some customers may in fact find they can’t insure their property in future if they are particularly risky. Consequently, risks shift away from insurers and to households and those providing mortgages against these properties (i.e. banks). And as the RBNZ points out “…some risks may ultimately end up with other parties, such as central and local government.” Second, banks may not be accurately pricing the value of some assets today. For instance, some bank customers, such as farmers, are likely to be exposed to climate change policy responses. The Government has recently announced a greenhouse gas reduction targets.

The FSR included the results of a RBNZ financial sector survey on the impacts of climate change (Analytical Box B). This showed that it’s not only insurers that are concerned about the impacts of climate change on their business, so too are banks. Ultimately, the higher costs resulting from climate change has to be borne by someone, and that’s likely to be everyone.